When Working Hard Stops Paying Off

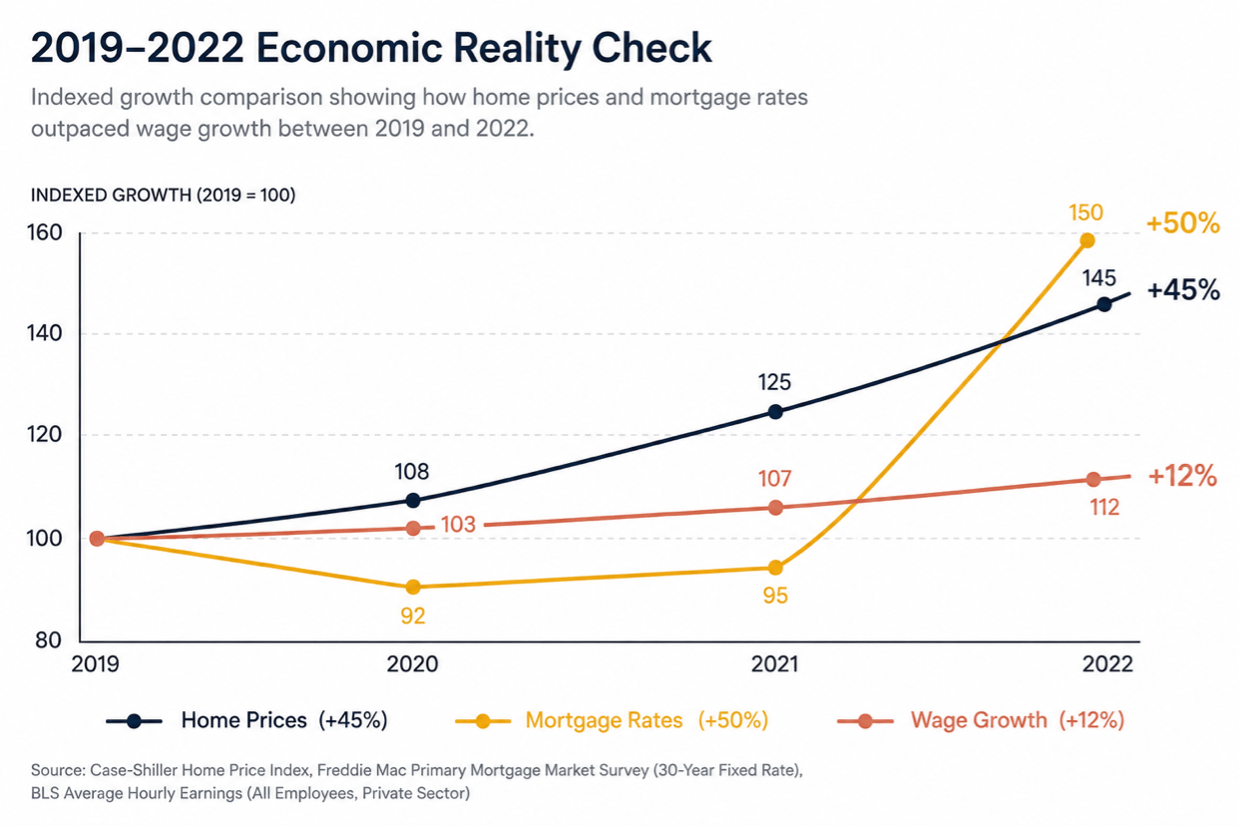

If you bought a home in 2019 and tried buying that same home today, chances are you would not be able to afford it. The same house, but a near 80% increase in monthly principal and interest payments. That is not a rounding error. That is a different life. Now imagine you are a renter trying to cross that gap, a gap that widened dramatically, and seemingly overnight.

“If this one parlay hits,” or “if these options finally print,” then maybe everything gets back on track. Prediction markets, zero-day-to-expiration options, sports betting, all symptoms of the same underlying problem. It is not laziness or entitlement, and it is less about greed than about desperation after watching traditional milestones become seemingly less attainable.

The system no longer appeared to reward the values it had always promised to reward: work hard, invest early, and you will be taken care of. When it feels like the goalpost is continually moved out of reach, taking excessive risk to bridge the gap seems a lot less speculative and more like a desperate grasp at the life you felt was promised.

Financial nihilism did not emerge from nowhere. For many people, it began during the COVID era, when both stock markets and housing prices rose at a pace that seemed to defy gravity, while wages largely stood still.

What Happens When an Entire Generation Stops Believing the Path Works

Imagine feeling like one day you are ready to buy your first home, and the next you feel like you’ll be renting forever. Or maybe you have finally saved up that three-month emergency fund, only for the next emergency to find you and deplete it. You do everything right. You work hard, you save, you plan, and yet the life you were told those habits would deliver feels further away than ever.

Housing costs are climbing. Everyday expenses feel heavier than they did just a few years ago. And your social media feed is flooded with stories of overnight wins: crypto moonshots, sports betting paydays, meme stock fortunes. In that environment, it is easy to understand why a single high-risk bet not only looks more appealing than another decade of savings, but can even start to feel rational.

This mindset has a name: financial nihilism. It is the growing belief that traditional investing and long-term saving may no longer feel sufficient or realistic, and that, in turn, makes larger financial risks feel more justified. And in many ways, that reaction reflects genuine economic frustration that millions of hardworking people across generations are experiencing right now.

This article is not about criticizing risk-taking or dismissing those frustrations, and it certainly is not aimed at calling those who are working tirelessly to make ends meet lazy or unresourceful. These issues are real, and they deserve to be taken seriously. It is about recognizing the difference between speculation and strategy, and about the path from one to the other.

At Gatewood, we believe long-term financial confidence is more often built through consistency, diversification, and informed decision-making than through chasing a single breakthrough moment. Even modest habits, paired with a disciplined plan, can create meaningful progress over time, without relying on unreliable attempts at market timing or taking on extraordinary risk.

Some numbers that put this frustration in sharper focus:

42% of Americans, including 42% of Gen Z, report living paycheck to paycheck, with nearly half citing the high cost of living as a top barrier to financial success.

When you are already stretched thin, it becomes easier to rationalize a high-upside gamble as a legitimate path forward.

A 2025 paper titled “Giving Up” by Lee and Yoo explores this dynamic directly. As households’ perceived probability of attaining homeownership falls, they systematically shift their behavior, consuming more relative to their wealth, reducing work effort, and taking on riskier investments. When a modest $100 bet could pay off 100x, the logic of making small, calculated gambles starts to feel less irrational. The problem is that those bets accumulate.

Nearly 32% of Gen Z and 24% of Millennials say they are currently invested in or considering prediction markets or sports betting, compared with just 17% of all U.S. adults, per Northwestern Mutual’s 2026 Planning & Progress Study.

The disproportionate share of young adults turning to highly speculative tools has both short- and long-term consequences.

In the short term, it means money lost that could have been saved. In the long term, the cost compounds: $1,000 a year spent on multi-leg parlays or binary options is $1,000 that never had the chance to grow in a diversified IRA. We believe that thoughtfully diversified investing is one of the more reliable long-term defenses against the silent wealth erosion of inflation. Many people view investing as risky because account values can fall, and that is true. But the equally real risk is that standing still means your purchasing power quietly declines year after year.

Of the more than 2 million Polymarket traders analyzed in a Wall Street Journal investigation, roughly 70% lose money and just 0.1% of accounts have captured 67% of all profits on the platform. Among the small group of profitable traders, the overwhelming majority have earned less than $1,000 in total.

The financial impact is only a piece of what needs to be addressed in this statistic. The time cost of repeatedly checking bets, worrying about results, and feeling the pull of “I really need this one to work out” takes a toll on emotional well-being in addition to financial well-being.

When Speculation Starts to Feel Rational

Financial nihilism does not emerge in a vacuum. It is the byproduct of a broader cultural shift in how people engage with money, risk, and the future. Over the last decade, the rapid evolution of speculative trading platforms has transformed investing from a disciplined, long-horizon practice into a highly gamified retail experience.

Options trading, once largely concentrated among professional market participants, is now accessible through mobile-first platforms designed to maximize engagement and transaction frequency. According to researchers at the Johns Hopkins Carey Business School, the volume of zero-day-to-expiration (0DTE) options on S&P 500 stocks more than doubled between 2021 and 2024, accounting for more than 43% of total daily options volume on those stocks. The result is an environment where investing increasingly resembles entertainment, and where the psychological distance between a speculative trade and its real-world impact on long-term financial well-being becomes dangerously blurred.

It is worth acknowledging that this is not the first time in history that excessive risk-taking has become normalized among certain groups. Options and other speculative instruments have existed for hundreds of years. What is genuinely new is how easy it has become to access them, and how deliberately the experience has been designed to feel like play.

Research in behavioral finance has long shown that people do not evaluate gains and losses rationally. Richard Thaler and Eric Johnson’s foundational work on the “house money effect” and “trying to break even” illustrates how prior gains can increase a person’s willingness to take risk, while prior losses often push them toward even more aggressive behavior in an attempt to recover. The result is a dangerous feedback loop: after experiencing losses, many investors become more speculative, not more cautious. Discipline gives way to the emotional impulse to get back to even. A telltale way of acknowledging this shift is the move from “it would be great if this bet paid off” to “I don’t know what I’ll do if this doesn’t work out.”

Gamification, Designed to Disconnect You from Consequence

Modern trading platforms amplify these tendencies through deliberate design. Instant deposits. Push notifications. Frictionless options approval. Celebratory animations when a trade closes. These are not accidents. They are features built to encourage both activity over intentionality and engagement over education.

In this environment, risk is abstracted from consequence. Repeated exposure to this cycle can deepen financial nihilism: the belief that traditional financial discipline no longer matters, that long-term planning is a fantasy, or that speculation is the only realistic path to getting ahead.

The broader challenge is cultural as much as financial. A generation raised during economic uncertainty, surrounded by social media-driven speculation, and handed instant access to leveraged products often lacks the institutional guidance that once reinforced prudent financial habits. No one taught them how to think about risk. And the platforms profiting from their activity have little incentive to.

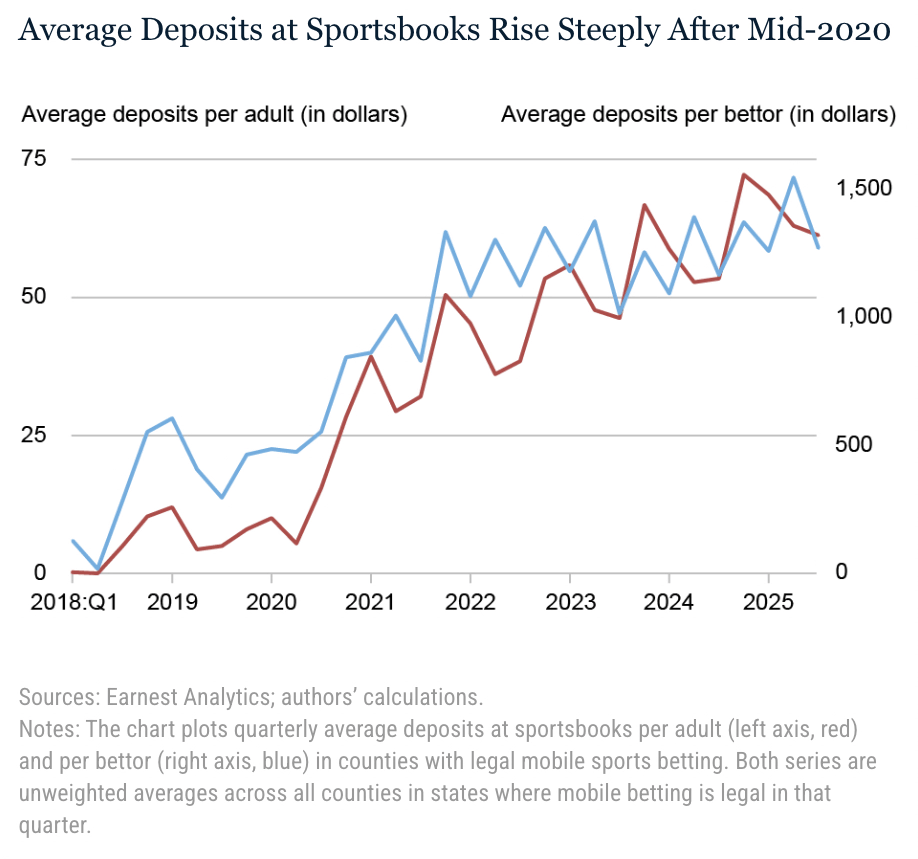

The line between informed investing based on company fundamentals and outright gambling has become increasingly blurred. Sports betting alone, since the repeal of the Professional and Amateur Sports Protection Act in 2018, generated $16.96 billion in gross revenue in 2025, up from approximately $430 million in 2018, a roughly 40-fold increase in seven years. And recent research from the Federal Reserve Bank of New York found that legalized sports betting has led to measurable increases in credit delinquencies, particularly among bettors under 40.

Moving Forward With Intention

At Gatewood, we believe the antidote to financial nihilism is not simply caution, it is education grounded in perspective, process, and personal accountability, paired with a portfolio structure that makes room for aspirational risk without derailing long-term progress.

Financial literacy must extend beyond understanding products and markets to include genuine awareness of the behavioral biases that shape financial decisions. Investors who recognize how psychology drives risk-taking are far better equipped to avoid reactive choices in moments of market volatility or personal financial stress.

Our Firm-to-Family® commitment reflects this. Financial guidance should not stop at the client, it should extend to their children and families. Personal finance is rarely taught well in K–12 classrooms, and depending on the path students take afterward, it may not be taught later either. These are foundational skills that matter regardless of career path or zip code.

Corrective action begins with restoring intentionality to the investment process by reframing wealth-building as a long-term discipline rather than a short-term outcome, emphasizing diversification and risk management, and helping people develop confidence through knowledge rather than speculation.

When investors understand how markets function, how compounding works over time, and how behavioral pitfalls erode returns, they are far more likely to make decisions aligned with their long-term goals rather than short-term emotions. Building financial stability does not require extraordinary income, perfect market timing, or unrealistic optimism, it requires a plan. Consistent contributions to diversified, long-term investments have historically created growth that speculation rarely delivers sustainably, while products like parlays, short-dated options trades, and prediction markets are designed to create excitement, not lasting wealth for the average participant.

Acknowledging these risks doesn’t require dismissing the frustrations younger Americans feel today. Those concerns are legitimate, and they deserve better than platitudes. More specifically, they deserve better access to clear, practical financial education, and plans built on realistic assumptions, not just being told to be more patient.

Start early. Stay consistent. Diversify broadly. Understand the behavioral traps. Give time the opportunity to work in your favor.

Giving Speculation a Home: The Three-Bucket Strategy

Believe it or not, there is a place in a portfolio for aspirational risk, which is a more refined way of describing speculation in financial circles.

The goal of financial planning is understanding where and when to take risks, and where to exercise restraint. When you embrace aspirational risk as part of a broader strategy, you acknowledge that not every investment needs to fit neatly into a long-term financial plan.

The Three-Bucket Strategy is integral to our planning practices and is discussed at length in this blog post. A brief explanation of each bucket is below:

- Bucket 1 — Safety: Liquid, low-risk reserves that cover near-term needs and keep you from having to touch your long-term investments in a crisis.

- Bucket 2 — Growth: Your core, diversified, long-term wealth-building engine, built on consistency and compounding over time.

- Bucket 3 — Aspirational: A deliberately small, pre-defined allocation for high-risk, high-reward bets that gives you skin in the game without jeopardizing the rest of your plan.

The aspirational bucket takes the impulse to speculate seriously rather than dismissing it. By giving speculation a defined home in your portfolio, it transforms a potentially destructive behavior into a controlled one. You are not told to ignore the frustration or simply “be more patient.” Instead, you are given a structured outlet for it.

The critical distinction is between desperation-driven speculation, where you need the bet to work out, and strategy-driven speculation, where a loss stings but does not derail your retirement, your child’s college fund, or your emergency cushion. Bucket 3 only works when Buckets 1 and 2 are intact first. That intentional sequencing is what separates a calculated swing from a desperate one.

From Discouraged and Aimless to Confident

People recognize gambling as speculative and risky, yet they overlook two quieter costs: the long-term financial harm of repeated small losses, and the compounding growth that money could have generated if it had been invested instead. That may be towards retirement, a child’s education, a family vacation, or other purposes that contribute to lasting financial confidence and personal fulfillment.

You don’t need a finance degree, a large portfolio, or perfect economic conditions to begin building toward long-term goals. What matters most is understanding the tradeoffs, creating a strategy aligned with your priorities, and giving time the opportunity to do its work.

Ultimately, combating financial nihilism is about rebuilding trust in process, in disciplined planning, and in the reality that long-term financial progress remains within reach even when it doesn’t feel that way.

Teach your children about personal finance early and often. Whether through sharing resources, having honest conversations about money, or working with an advisor who’s enthusiastic about educating both you and your family, anything is better than nothing. If you’re not sure where to start, that’s exactly what Gatewood is here for.

Build a strategy. Not a lucky break.

Go Deeper on the Three Buckets

The Three-Bucket framework is the backbone of how we approach long-term wealth-building at Gatewood and there’s a lot more to it than this post could cover. Our free e-book walks through each bucket in depth: what belongs in it, how it works alongside the others, and how to put the whole framework to work in your own financial life.

Sources & References

- Lee, Seung Hyeong, and Younggeun Yoo. “‘Giving Up’: The Impact of Decreasing Housing Affordability on Consumption, Work Effort, and Investment.” SSRN Working Paper, November 19, 2025. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5770722

- Thaler, Richard H., and Eric J. Johnson. “Gambling with the House Money and Trying to Break Even: The Effects of Prior Outcomes on Risky Choice.” Management Science, vol. 36, no. 6 (1990): 643–660.

- Bank of America. “BofA Study Finds Fewer Gen Z Rely on Family for Financial Assistance, Even With 42% Living Paycheck to Paycheck.” Better Money Habits Report, May 2026. https://newsroom.bankofamerica.com/content/newsroom/press-releases/2026/05/bofa-study-finds-fewer-gen-z-rely-on-family-for-financial-assist.html

- Northwestern Mutual. “2026 Planning & Progress Study.” March 2026. https://news.northwesternmutual.com/planning-and-progress-study-2026

- Ostroff, Caitlin, Katherine Long, and Neil Mehta. “The Tiny Group of Polymarket Traders Taking Home Most of the Profits.” The Wall Street Journal, May 2026. (Analysis of 1.6 million Polymarket accounts since November 2022.) Johns Hopkins Carey Business School. “Risk and Reward: New Insights on 0DTE Option Trading.” 2024.

- American Gaming Association. “Commercial Gaming Revenue Hits $78.7 Billion in 2025.” February 26, 2026. https://www.americangaming.org/resources/commercial-gaming-revenue-tracker/

- American Gaming Association. “State of the States 2019” (for the 2018 baseline sports betting revenue figure).

- Goss, Jacob, and Daniel Mangrum. “Sports Betting Is Everywhere, Especially on Credit Reports.” Federal Reserve Bank of New York Liberty Street Economics, March 25, 2026. https://doi.org/10.59576/lse.20260325

Important Disclosures:

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. Gatewood Wealth Solutions and LPL Financial do not provide legal or tax advice or services.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.