Payroll Gain is Amongst Largest Downside Miss Ever

Payrolls rose $266,000 from a month ago, according to a Labor Department report Friday, May, 7th 2021 that represented one of the most significant downsides miss on record. Economists in a Bloomberg survey projected a $1 million hiring surge in April 2021.

Catching the media’s eye, there is some concern from a miss standpoint. This would be the biggest miss ever at more than three standard deviations out from the mean, so in other words, it shouldn’t have happened.

McDonald’s Struggle with Unemployment Benefits

The National Owners Association (NOA) is an organization “to unify Owners to “Lead Together Again” and save our culture while assuring the owners have net cash flow growth, financial viability and are immune from intimidation and retribution.” McDonald’s is a part of this organization. They’re having trouble hiring employees due to unemployment benefits and say an ‘inflationary time bomb’ will force them to hike Big Mac prices up.

Here are a few key quotes from the NOA letter to its members:

“What’s going on here? When people can make more staying at home than going to work, they will stay at home,” the letter read, which was obtained by Insider. “It’s that simple. We don’t blame them. We fault the system.”

“Natural human behavior is to choose to receive more money while staying at home than working for a highly demanding job — especially with the amount of stress that is being put on employees right now.”

Welfare Wall- Economy

In the below chart from Gary Alexander, Secretary of Public Welfare, Commonwealth of Pennsylvania, explained, “a single mom is better off earnings gross income of $29,000 with $57,327 in net income with benefits than to earn gross income of $69,000 with net income and benefits of $57,045.” They came up with this ten years ago. So $69,000 is a good salary now, but an excellent salary then. The skillset that is needed to bridge that gap would be pretty difficult to cover.

But what was more shocking is the chart below that Steven Rattner, New York Investment Asset Manager, tweeted. The chart showed tens of millions of US workers, in jobs ranging from the dishwasher, to the hotel clerk, to preschool teacher, to anyone on minimum wage, can now earn more from unemployment than from their regular job.

If you look at the unemployment bar, people get an equivalent of $11.23 to $7.25 per hour for minimum wage. Also, the median salary of $20.08 is compared to $17.78. As you can see, unemployment benefits have affected different parts of the labor market differently.

So, what is the other argument outside of just unemployment benefits taking up additional employees?

If you look at who is going back to work, there are many more men represented than women. It may not be disincentives, but rather the burden of children still at home from school falling on women, not allowing them to go back to work. Another problem with this is the question of the labor market having to compete with the government to get these people to come back to work.

We are not seeing the polls that you would expect if they were competing with the government. You would expect the low-wage employment to be rising as they’re trying to offer higher benefits to attract the person coming in.

The next issue is regarding the miss and not showing up in other datasets. If we look at the chart below from ADP Research Insitute regarding data leisure, hospitality, trade, and transportation, these areas pick up the most jobs and have the most job openings.

The data shows $742,000 of payroll gain compared to $266,000 from the Bureaus of Labor Statistics. At the moment, GWS believes a lot is going on here, and probably a significant part is sampling. The Bureau of Labor Statistics is trying to control things such as working part-time, contracting, going full-time, how many companies have been created, and how many companies are lost, ultimately showing a sample error.

Effects on the Stock Market

What has been driving the stock market is stimulus, whether it’s a federal stimulus or not. The federal reserve still sees these unemployment numbers, and they have a dual mandate to maintain the purchasing value of the currency and keep unemployment low. They think inflation’s transitory, moving to a 36 month rolling 2% average. When we look at the data, we have some low numbers going back 36 months.

They think inflation isn’t a thing, but they are working out of a paradigm, a trade-off between inflation and unemployment. Whatever the reasoning behind the actions is, the Feds are going to continue to be accommodated. Next, we have unemployment data that says the recovery isn’t happening as quickly as we like. CPI is on an annualized basis at 0.8, that’s 9.6%. You can see in the chart below if inflation did cause interest rates to move up, then the 30 years could be down 20% and the ten years down 8-9%.

—-

Keep up to date on Gatewood Wealth Solutions through our daily 3x3s and our weekly market insights on our YouTube, LinkedIn, and Facebook accounts.

Disclosures:

Economic forecasts set forth may not develop as predicted, and there can be no guarantee that strategies promoted will be successful.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested directly.

Securities and advisory services are offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

The Roaring Twenties

We continually compare what we’ve gone through over the last decade to the roaring twenties. If we go back and look at the stock market, especially the crash as we went into the thirties, a lot was going on more than just the stock market.

GWS compares what is happening currently to the twenties because of how the money supply was used: coming out of the progressive era with World War I just ending. Much of the government spending was curtailed because the war had ended, and we had an advanced period of central banking. However, there was also a legacy component of cutting government spending and taxes to stimulate the economy. But what wasn’t happening in the 1920s was the rampant laws and unfair capitalism.

Money Supply in the 1920s

In the twenties, we had a currency that was outstanding with not much change. It was timed deposits, what we call Certificate of Deposit (CD) now, and demand deposits increasing behind the scenes. So, the central bank started to grow because there was a gold-backed system. We can see it can affect the money supply in Column 8 (below), rising about 70% over the decade.

Gatewood Wealth Solutions believes that the amount of money being created will make it into capital markets or capital assets first and cause an appreciation in those assets. Between 1920-21, we went through a recession with a lot of the government spending is for World War l with deflation in the system. Therefore, the federal reserve saw it in the index and began to expand the money supply.

Also, when World War I ended, Europe was very much devastated, and they needed foreign loans—allowing these foreign loans to be made by the U.S. to Europe. In turn, the loans were used mainly to buy exports from the U.S., specifically agriculture. The overall point is when we see the money supply expand, the market expands right along with it.

The graph above is looking at the annual percentage of change in the money supply. The yearly change is quite variable: 4% up to 10% of basically 0% right before the crash. However, it does not state when the money supply got near zero in terms of new and additional money into the system.

We can see (above) the money supply takes off with a lag coming out of the first recession. Then, there’s a more stable money supply as growth begins to slow. Next, we get into the 24-25 period when England is trying to go to the gold standard. The Fed lowers interest rates again, and we see lag, but it corresponds to an increase in capital markets. The money supply begins to stabilize for a short amount of time with a little bit of flatness in the market. Lastly, going into 1928-29, we start to see the Fed slow, getting down to a 0.7% growth rate. Then, the crash occurs.

However, the point is, the money supply was increasing dramatically along with the capital markets. Though the money supply expanded in the right direction, we didn’t see inflation growing somewhat rapidly. The Fed was expanding the money supply based on a stable basket price and allowing them to continue to raise the money supply and see the capital market.

In the Inflation Basket graph above, we can see a 68% increase in the total money supply over time, but we do not see inflation above 4% whenever we measure it as a basket of goods. Coming out of World War l, command and control components were put on the economy to provide war goods. As those were ending, a lot of the government spending was ending too. Therefore, as the economy restructured, prices were falling in the goods in the basket without stabilization. The Fed used an inflation basket to gauge how much money they should create to get to a stable price.

The economy in the 1920s

Most places that people lived were getting electricity, and with that comes new labor-saving appliances such as a vacuum, washing machine, and toaster. Also, instant communication is occurring through mass media, such as the radio. You were able to pick up a phone and connect with people across the world. The new invention of a vehicle came about to go further away to find better economic opportunities. Like today, we have a lot of new technology coming in, causing an increase in productivity.

This is all one big cycle as farms were starting to be mechanized. The tractor was becoming something that farmers were using to increase agricultural output dramatically. People were leaving the urban environment because farms could produce food. Therefore, the higher-cost producers had to go, but there was plenty of jobs at the factory. The demand for labor kept prices up, causing the production capacity of the economy to grow faster than the money supply.

However, it was causing an imbalance because food prices started to decrease. Money was being borrowed for the farm implements. Therefore, there were a lot of bankruptcies, especially whenever there was inflation. The Fed eventually slowed the money supply causing the crash.

“If we’re living in something like the 1920s, will we have the same outcome?”

GWS does not think the next phase will look like the 1930s. We believe the Fed will be swift to continue to expand the money supply because they’re not concerned about a rise in inflation. They would welcome inflation to offset some of the deflationary pressures.

Averaging out the average 2% will allow prices to increase. If we can’t maintain this productivity gain that we’ve had over the last couple of decades, our experience will be more like the 1970s, where you have inflation as the outcome and not deflation.

—-

Keep up to date on Gatewood Wealth Solutions through our daily 3x3s and our weekly market insights on our YouTube, LinkedIn, and Facebook accounts.

Disclosures:

Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested directly.

Securities and advisory services are offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

As some of you may know, this Sunday is a special day for me; it will be my first Mother’s Day. My husband, Kyle, and I were blessed with two beautiful baby girls last year, and they are the lights of our lives! Nothing gives me more joy than to watch them continue to grow and develop their personalities.

What you may not know is that I am also celebrating another milestone this year: being cancer-free. Just after I had my twins last summer, I learned I had cancer and immediately began treatments. It was a whirlwind undergoing chemo, learning to be a first-time mother to twins, and figuring out what the future looked like for our family. While I am happy now in remission, that time last summer is etched into my memory — the barrage of emotions, the weighty decisions, the vast life adjustments.

During this time, I also gained tremendous clarity on what it means to have a purposeful life. And it got me thinking about how we help our clients find purpose in their lives, too. Our Chief Development Officer, Daniel Goeddel, issued a challenge to our firm last summer to develop our individual “elevator pitches” for the firm. The one-sentence lines we would use to tell people about the heart and soul of our firm and what makes us different.

As I lay in my hospital bed for a week, having come down with an infection due to my chemo-compromised immune system, Dan’s challenge came to mind. It was the first time I was away from the twins after they were born for more than just one night,and I couldn’t have any visitors because of Covid-19. As I lay there, pondering, a phrase suddenly came to me:

“We give purpose to your money so that you can be present in your life.”

Let me tell you what I mean by this.

When you hold your newborn baby for the first time, and they wrapped their finger around yours, were you thinking, “Do I need to increase my investment exposure in the technology and financial sector due to current market conditions?” No.

When you are watching that same child walk across the stage at their graduation as they lift their diploma in excitement, will you ask yourself, “What is the tax implication of withdrawing the left-over funds in their 529 accounts?” No.

When that child yells “Happy Retirement” as you walk into a room filled with your closest family, friends, and co-workers celebrating the end of a 40-year career, will it cross your mind? “Did I save enough money to last the next 40 years and continue to live the lifestyle that I have become accustomed to?” Of course not.

And when that child stands beside your grave after peacefully passing away in your sleep after a long 90-year life, they won’t have to be thinking, “Did Dad complete his estate planning documents and have insurance in place to plan for our family?” That will be the last thing on their mind.

Why? Because you are our client. Here at Gatewood Wealth Solutions, we give purpose to your money so you can give meaning to and be present in your life. With your goals as our objective, we look at all aspects of your financial situation, from income and estate tax planning to risk and investment management. We provide solutions to life’s most challenging questions through a customized service commitment based on your family’s complexity, leaving you free to enjoy life’s best moments.

Life’s best moments might be different for everyone. But for me, these are the moments I spend with my growing family — for whom I am incredibly thankful this Mother’s Day.

—-

Disclosures:

Securities and advisory services are offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

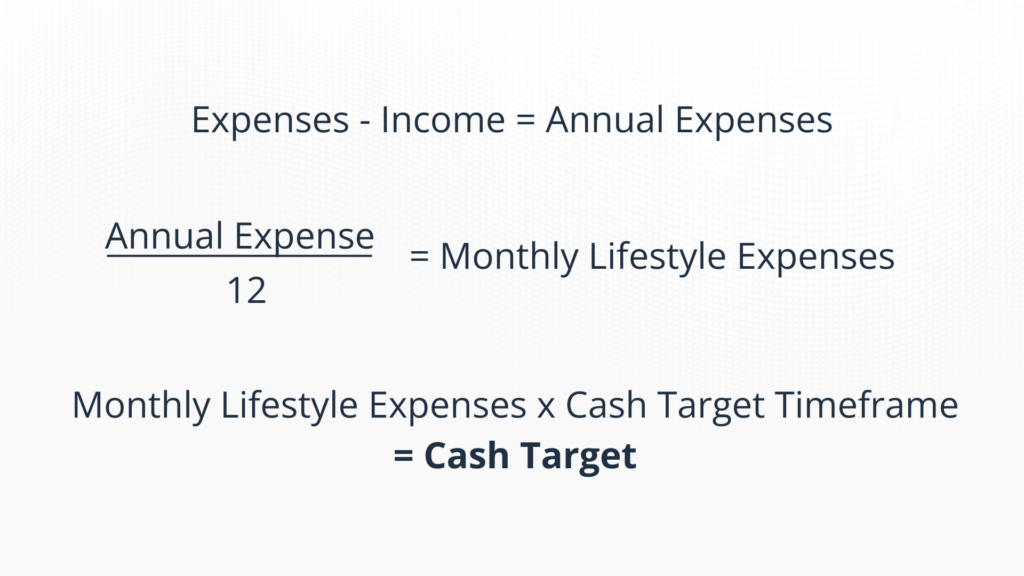

At Gatewood Wealth Solutions, we pride ourselves on keeping our clients “Bear Market Ready, but Bull Market Positioned.” By this, we mean that we help clients calculate an emergency fund — what we call their “Cash Target” — seeks to protect them during down markets. Then, the rest goes into the market, where it can seek growth.

Our firm has worked hard to develop an approach that allows us to pinpoint exactly where that “sweet spot” is, based on clients’ expenses, life stages, and our investment committee’s outlook on the market. Our financial planning and investment management teams work closely together to ensure no stone goes unturned in making this assessment.

How do we come to this number, which we call a client’s Cash Target? We’re glad you asked.

Step 1: Determine the client’s total annual expenses.

We start by totaling the client’s annual expenses. These include lifestyle expenses, taxes (including federal, state, and property), insurance, liabilities, charitable giving, insurance payments, and other costs. Then, we assess if there are expense changes during the “Cash Target Timeframe.” If so, we include this in the Cash Target formula by finding the cash target each year, as you will see in Step 4.

Step 2: Evaluate the client’s income.

Once we determine a number for annual income, we again review any year-to-year changes by identifying specific Cash Targets for each year if the income fluctuates.

Step 3: Incorporate the Investment Committee’s current Cash Target Timeframe.

Our Investment Committee regularly evaluates market conditions to make recommendations for ideal Cash Targets. For example, pre-pandemic, the general Cash Target was 24 months. By January 2021, our investment committee increased the target to 33 months. As you can see, the “Cash Target” — the amount we recommend clients keep on hand in cash — expanded as the market became more uncertain. And it will likely shrink back again as the market gains stability.

Step 4: Calculate the Cash Target

Next, we move on to the actual calculation. We know life (more precisely– income and expenses) is not the same year after year. Therefore, we developed a formula to consider those income or expense changes:

If no expense or income changes:

Expenses – income = Annual Expense /12 = Monthly Lifestyle Expense X Cash Target Timeframe = Cash Target

If an expense or income changes:

Year 1: Expenses – income = Annual Expense /12 = Monthly Lifestyle Expense X 12 = Year 1 Cash Target

+ Year 2: Expenses – income = Annual Expense /12 = Monthly Lifestyle Expense X 12 = Year 2 Cash Target

= Cash Hub Target

Note: If more than 24-month Cash Target, we would continue the process (+ Year 3 Expenses – income = Annual Expense /12 = Monthly Lifestyle Expense X 12 = Year 2 Cash Target).

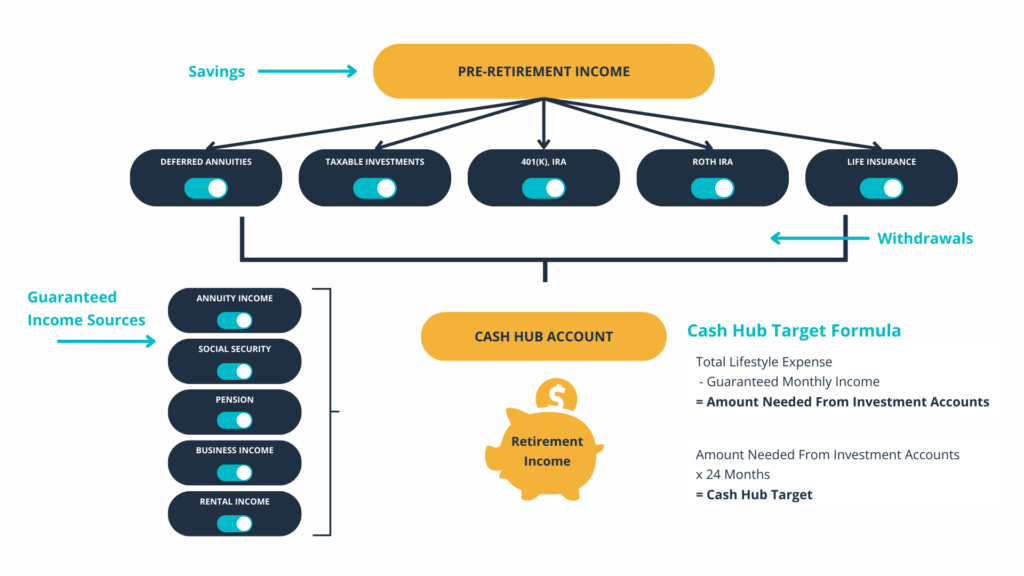

Step 5: Fund the Cash Hub Account

Once we have the Cash Target amount, we calculate and fund the Cash Hub Account. For example, if your cash target is $240,000 and you have $100,000 in your checking/savings account, we would fund the Cash Hub Account at our firm with $140,000. However, the big questions are – which accounts do you pull from and when? To answer this, we consider tax qualification and tax brackets, liquidity concerns, and legacy goals.

The cash hub account is just one small part of our overall distribution planning approach, which you can see below. Our planning team constantly turns these funnels on and off based on our clients’ specific financial situations and life goals. We can make sure we correctly put our clients’ money to work for them while maximizing their tax-saving strategies.

Important Disclosures:

All investing involves risk, including the possible loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested directly.

Securities and advisory services are offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

When our GWS team meets with prospective clients, one of the first questions we ask is, “What brought you in today?”

Most of the time, these prospective clients have undergone a significant life event — such as receiving an inheritance, going through a divorce, nearing retirement, or experiencing a liquidity event — that made them decide to seek professional guidance for their financial futures.

It may not come as a surprise that the most common reason clients walk in our door is, “I’m retiring.” Retirement is something most of us work toward for decades, but it can be overwhelming as it approaches. We’re here to help simplify the process for clients by sharing our experience with you to help you become and remain financially self-reliant.

Here are the top eight steps your GWS team will help you complete when you decide to retire.

1. Calculate your Cash Target

At GWS, we recommend identifying your Cash Target two years before you retire. However, if you are new to retirement planning with our firm, there is still time. Your Cash Target is essentially your emergency fund. This is important, so you never have to liquidate your investments when the market is down. Selling your investments during a market correction could have a significant impact on your success in retirement.

Below is the formula used to calculate your Cash Target – the first step is calculating your expenses. It might sound daunting to figure what your costs will be in retirement, but your GWS advisors will help you do the rest of the work if you have that number.

The “Cash Target Timeframe” above comes from the GWS Investment Committee, based on the underlying market and economy, and gets revisited quarterly. Our Cash Target Timeframe ranges from 24-36 months.

2. Calculate & Fill your Cash Hub Account Target

The next step is to calculate and fund your “Cash Hub Account Target” – in other words, the amount you need from your investments held in an account at our firm that we refill or spend down every quarter.

Depending on the tax qualification of your assets and the timeline of your income and expenses, funding and monitoring the Cash Hub Account can be complicated. Our team is here to help take the guesswork out of the process.

3. Contribute Tax Efficiently in the Year of Retirement

Whether your retirement is your highest tax bracket year or one of your lower tax bracket years, working with our team to determine how to maximize your tax-efficient contributions is vital. For one client, the best scenario could be maximizing pretax options in their 401(k) or contributing to a Donor Advised Fund for a tax deduction. While for another client, the best scenario would be to contribute to a Roth 401(k) and do a Roth Conversion in the year of retirement. Having the ability to leverage flexible tax treatment in years of higher (or lower) income is essential in this step.

4. Review Retiree Benefits Package

Your GWS team can help provide you a summary of everything you can expect from your benefits, including:

Options with Regards to your Employers Sponsored Retirement Plans

Pension Benefit Amount & Election Options

Deferred Compensation Plan Payout

Employer-Sponsored Health Insurance

Some of these benefits can get complicated because they vary based on time of service, years of compensation, age you want to take your benefits, and how the income stream is set up going forward. Also, you must decide which pension or deferred compensation elections make the most sense for you. If given the option, should you take it all at once? Spread out payments via an annuity?

Understanding how your benefits package affects your other assets and financial planning is essential. The more plans you have, the more complicated it gets because different structures are available to you. Your advisor will help you walk through all your options and determine what makes the most sense for your financial situation.

5. Access Health Insurance Options

If you are younger than 65 and do not have employer-sponsored health insurance, you will have to supply your health care coverage through vehicles such as COBRA, or if your employer doesn’t offer a COBRA plan, you can try the Affordable Care Act (Obamacare).

Employing this option and depending on your income, you may even qualify for a subsidy. But open enrollment periods are limited, and you must plan your retirement accordingly. Other insurance options include less robust coverage choices with short-term plans. These plans are usually viable for generally healthy people who have no pre-existing conditions.

6. Elect Social Security

Social Security can be confusing — let alone understanding how to maximize it. Your advisor can help walk you through all the pros and cons of when you and your partner should elect to take it.

At GWS, we have our own Social Security Maximization Process to help you determine how to get the most Social Security benefits for you and your family. We can help you visualize the financial implications of electing your benefit early, at full retirement age, or later in life. That way, you can know what to expect from each possible scenario, allowing you to make informed decisions.

7. Set up a Monthly Withdrawal Structure and Bank Account

Our team will help you create a “paycheck” in retirement! If your company sent you your paycheck twice a month, you might set up your distributions from your Cash Hub Account to mimic that frequency. Having a set schedule like this will make your life easier and help you keep a good understanding of when your money is coming in.

By considering what your exact cash needs will be in retirement, you can make sure that you have the correct distribution funnels in place and money coming out of the bank.

8. Distribution Planning

How do you determine which accounts to pull from and when? This can be overwhelming, but working with our team to create a tax-efficient strategy can save you tens or even hundreds of thousands of dollars over the long run.

It all goes back to the concept of distribution planning, which you can see depicted in our infographic above. Your advisor will help you turn on and off different levers, depending on your tax bracket, to help you take a strategic approach to tax savings.

The hallmark of our culture is our commitment not simply to answer questions but to find clear solutions that lead to better outcomes for our clients. A lot goes into the retirement planning puzzle, but your advisor can help give you confidence that you’ve covered all your bases.

Our highly credentialed team is here to help you and answer your questions. Feel free to reach out to us using the scheduling tool below or give us a call at (314) 924-5100. We would love to hear from you!

—-

Disclosures:

All investing involves risk, including the possible loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested directly.

Securities and advisory services are offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

Government Total Expenditures

The amount of government spending recently has been very high. We have two bills, infrastructure, and stimulus, being massive ticket items. During the 2008 crisis, everyone was agitated about the $1 trillion spent for the bailout. However, today we’re doing two $2 trillion bills. The government spending is undoubtedly high, and we’re starting to see that show up in the reports for companies.

Inflation Concerns

The graph below is looking at inflation concerns regarding earnings reports of companies and the correlation to inflation. When companies are giving their updates on goods, services, materials, labor, and the rest of their spending, it correlates with Consumer Price Index (CPI). We can see that it’s up 12%, which is enormous.

However, we see an uptick in the concerns by companies, and we can see the CPI correlates with consumer products. We’ve been as high as this before, and we did not go negative in the previous recession from lockdowns. So, we’re going off a higher base, and we’re already above-target inflation of 2%.

Who is Seeing Inflation First?

Producers see the inflation in the pricing first. Here is just a snippet of several reports from different companies that are talking about significant price increases as they produce the product:

FAST (Industrials): “We are experiencing significant material cost inflation, particularly for steel, fuel, and transportation costs.”

GIS (Staples): “Looking ahead, as we experienced a higher inflationary environment, our first line of defense will continue to be our strong holistic margin management cost-savings program. In addition, we are taking actions now and in the coming months […] to drive net

price realization that will benefit our FY2022. “

CAG (Staples): “we see input cost inflation accelerate in many of our categories and across the industry.”

LW (Staples): “while the pandemic-related effects on our supply chain were the primary drivers of our cost increases, we also realized higher costs due to input cost inflation in the low single-digits. We expect that rate will begin to tick up in the coming quarters as edible oil and transportation costs continue to increase.”

STZ (Staples): “similar to previous years, we’re expecting substantial inflation headwinds in the low to mid-single-digit increase range, largely related to glass and other packaging materials, raw materials, transportation, and labor costs in Mexico. “

PPG (Materials): “We experienced a significant acceleration of raw material and logistics cost inflation during the quarter. Coming into the year, we were expecting an inflationary environment and had prioritized selling price increases across all of our businesses. This has helped us achieve solid price increases year-to-date. With a higher inflation backdrop, we have already secured further selling price increases and are in the process of executing additional ones during the second quarter. “

DOV (Industrials): “What we are going to fight against between now and the end of the year […] is inflationary input costs between raw materials, labor, and price/cost. […] the way it’s looking, we may have to intervene on price again in certain of the businesses over the balance of the year.”

TEL (Tech): “I would expect our margins to modestly improve as we work our way forward here into the third and fourth quarter based on some of the actions that are underway and our ability to combat some of the inflationary pressures out there. […] Certainly, we’re feeling the biggest inflation right now is on the freight side. The freight inflation has been significant. And as we battled through there and there’s a variety of reasons for that, including higher air freight and so forth in terms of that. And that’s not unique to TE. Certainly, I think that’s been as well-publicized across the overall supply chain. […] labor cost is not a major issue on the inflation side, but labor availability in certain places that COVID is more impacting continues to drive some inefficiencies.”

These companies are discussing significant price increases as they produce their product due to supply and demand. If you look at the import price in the graph below, you can see a much higher spike than the CPI. The CPI is a blue line, and it is going parabolic. We also see it in the producer price index (PPI). As the companies push those out, then stock prices will continue to move up, which is a good thing.

Transitory – Short Term Components of Current Issues

What’s causing the current issues are transitory (short-term component) at the moment. If we look at just how many ships are trying to get into ports due to the back-order on goods, you will see how incredibly expensive a shopping container goes for. It comes down to the supply and demand component because many people have done without specific goods, and they’re trying to restock.

Although unemployment is high, we see a labor shortage in the lower wages across the board looking at the supply chain because it was disrupted due to the pandemic. Do we see this fixing itself over time? Yes, this is what we call transitory as supply-demand will come to a balance. However, we also have a monetary policy that is not transitory, which will be seen in food prices as they go up substantially.

There is also a discretionary component for the low and middle income, where if prices are going up on things they’re demanding, and they have to use more of their paycheck to purchase these items. Then, they will have less of their salary to pay for other things. Therefore, everyone’s inflation basket and experience are different. We can start to look at different groups on how inflation affects them differently. If we look at the bottom 10% (the median earner), we could see inflation is much higher than if we’re looking at the top 10% of earners.

Suppose it’s not a significant percentage, and everyone else has had to cut back elsewhere. In that case, the higher income will be able to spend money and go further because inflation is moving prices.

Biden’s Tax Plan

Political unrest will support calls for higher taxes on higher-income earners. This is not a phenomenon that just happened in 2020. It has been going on for quite some time. We’ve made the argument that it’s the federal reserve and their monetary policy that has benefited people with assets over those that make income.

The 1% and big divide between the different economic levels is something that’s been prolonged. Therefore, it is easier to propose higher tax increases. The current tax plan wants to raise the corporate tax rate from 21% to 28%, restore top individual rates from 37% to 39.6%, subject wages above $400,000 to social security payroll tax, and taxes on capital gains as ordinary income.

We’ve been able to “print” money, and there has not been the inflationary effect, so why raise the taxes? If Biden’s tax plan were to pass, this would not solve all the problems because it may not impact the number of government receipts coming in, and people change their behavior.

Also, there is a proposal to have the IRS donate $88 billion over the next ten years to make sure people are not gaming the tax system. Suppose you have to pay people to prevent any additional gaming of the system. In that case, that’s money that you’re not going to spend on the other government items, and it proves the point that when people are going to do a lot of things to prevent the tax from actually hitting right.

Although this is a higher than average tax increase, if we look at both of them together, it’s not the highest. Supporters and critics of President Biden’s tax plan have made various claims about the size of the tax proposals, ranging from “not big enough” to the “biggest tax increase in history,” however it can be both.

By comparison to these past tax increases, in the first year, Biden’s tax plan would increase federal revenue by 0.68% GDP, making it the tenth-largest tax increase since the 1940s. In the second year of Biden’s plan, when the temporary expansion of the Child Tax Credit expires, the plan would increase federal revenue by 1.52% GDP, tying for the fourth-largest tax increase as a share of GDP since the 1940s.

In addition, Biden’s proposal would raise significant revenue. The plan would also have a negative long-run effect on the American economy, lowering long-run output and after-tax incomes.

If we look at the tax foundation table above, they assume GDP will drop 1.62% on our future growth. Our capital stock will decrease, and it’s the capital that allows for wage increases long-term. The more efficient your tools are that make you more productive; the more you can sell, and the higher wages you can pay.

Then, we would see a wage rate drop because of the tax increase. It’s not just the wealthy that are going to feel this. The rich create businesses and spend a lot of the money to affect the people they hire if they have less of that. Then, it would cause an estimated half-million lost jobs due to tax increases.

Tax Revenue

Now, let’s talk about tax revenue as a way to close the gap. We can change the way taxes are received, but that’s not the problem. The problem is the amount of government spending. The graph to the left shows you the volatility and the growth rate compared to revenue. Revenue is relatively steady, and it continues to move up.

The graph on the right shows the revenue and stability (the green line) versus the spending. The spending is growing, and at the bottom, you can see the deficit. Therefore, it’s the government spending that is causing a lot of the problems. So, if we want to make a significant impact on the deficit, the bigger thing to focus on at the moment is government spends.

—-

Keep up to date on Gatewood Wealth Solutions through our daily 3x3s and our weekly market insights on our YouTube, LinkedIn, and Facebook accounts.

Disclosures:

Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

This information is not intended to be a substitute for specific indivudalized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

All investing involves risk, including the possible loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested directly.

Securities and advisory services are offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

Demographics and Destiny

Demographics is destiny, not density. This map shows how many more people live in other countries compared to our own. We can see China and India are the densest and most populated countries.

To understand how this affects the economy, we need to go back to the Keynesian model. It shows Gross Domestic Product (GDP) equals consumption plus investment plus government spending, and exports and imports will have some effect. The two things that matter the most are consumption and investment choices. Everyone is constantly consuming things, but some have different ratios on consumption versus investment.

If you look at the senior population, frequently industrialized and developed nations have significant savings from the previous production. When we think about them as only consumers, it’s a lowercase c. Why? Because many people call them “annoyingly wise” with their consumption. In other words, they have to be much wiser on how they consume. We would consider this lifestyle bucket to have many savings if it’s an industrialized country, but there are low consumers in the GDP model.

Producer Population

Now, if we look at the producer population, they will be consumers while being significant producers. Goods that are coming into the economy will be produced by the age group of 18-65. Their choices between consuming versus investing will be highly related to how many people are dependent upon them.

Suppose you look back to the senior population, and they don’t have savings to live off of. In that case, they’re going to put a drag on the producer population because their consumption versus investment choices are different. Meaning they may have a parent to be supported. This leads to less money for investment causing GDP to grow more dramatically. Therefore, the lower the senior population dependency on the producer population, the faster the GDP can grow.

Borrowing Population

Then there’s the borrowing population. This population is no longer in childhood, and they are getting educations, starting families, or starting their first job. They are not big producers yet, but they have a lot of demand for borrowing because they’re investing in future production. They have a symbiotic relationship with the senior population because they can loan to this group as they develop their skills.

Child Population

The child population is a significant factor in the producer population regarding consumption. If you don’t have many kids, you tend to have more investment in other things in your life. Therefore, children will be a big part of the producer’s consumption versus investment choices. Just because children are mainly only consumed does not mean that’s a drawback because they’re detrimental to long-term growth. Remember, they’re the future producers as well.

Expanding Population

The population pyramid above is an expanding population often relating to an expanding economy with the age bands on the left. Then, you have it divided by how many people are male or female. For productivity of making more children, the ratio of women is far more critical than the number of men. It’s the norm of the population, when the more women you have, the higher the fertility rate. The ratio of men to women will have different economic impacts, like China has fewer women than men because of their prior one-child policy.

If you look at the pyramid, we can see that the segment comprises mainly young people. The further we go up the less impact that has. This is met with good capital structure and technology and could be a booming economy in the next 20 to 30 years.

Stationary Population

Here is a stationary population. We see the children and the producing population are pretty steady. However, there is a little bit of a decrease here, but you can easily make that up with immigration. We can see that this will be just a stationary economy with no significant liability for demographics in the future.

Population Dividend

Next, we have the population dividend. If you get an example where the fertility rate is low in a country with not many children or elderly for the producer population to support, then the choices on consumption versus investment change. All the excess money is going into the growing the economy faster, which is a massive boon for the economy. The population dividend turns into a population liability.

Population Liability

As individuals retire, there’s a decreasing amount of people that are producing within the economy. If there were plenty of savings that the senior population has to live off during production, then there will be more imports coming in to support them as they decrease spending.

Demographic Comparisons

What are the four countries we have been talking about? The first one expanding is Mexico, with a very young population that is multiplying. The next one, the United States, is right next door to Mexico, where the immigration is coming from the Southern border. The current population dividend is China, and they do not have a lot of savings for their senior and the current producer population. They are becoming wealthier, but not fast. Lastly, we have Japan for population liability. Japan in the eighties-nineties was taking over the world because they were in a population dividend.

Japan and China Comparison

China has a 20-year lag to Japan. Japan was in the expanding phase through the sixties to seventies. Then, they started to move into the producer population. By the eighties to the nineties, they were reaching the population dividend. Then, 2000 happened, and things began to turn, and the economy not growing much since.

Production Function: Growth Rate of GDP Overtime

Y(t)= A(t)K(t)aL(t)1-a

(Current Capital Stock, Technology Development, and Labor Population)

The growth rate of GDP over time has a couple of more factors with a fairly complex equation, but we can keep it simple as:

Do you have a current capital structure?

Do you have factories and tools that are already there in the economy?

Are they good at developing that capital structure further?

These three components are the primary factors on how fast an economy is going to grow over time.

—-

Keep up to date on Gatewood Wealth Solutions through our daily 3x3s and our weekly market insights on our YouTube, LinkedIn, and Facebook accounts.

Disclosures:

All investing involves risk, including the possible loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Securities and advisory services are offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

Market Bubble?

When we’re thinking about the market, one thing that is on our minds is the market in a bubble? You turn on your TV and, you often get an oversimplified definition: priced earnings P/Es are high, sell your stocks. This is on people’s minds because they see previous valuations in 2000 and 2008. So, it is a fair statement to say valuations are stretched.

Price to Earnings Ratio

The price of the S&P 500 divided by its trailing earnings gives you the price-to-earnings ratio. You can use all sorts of measures for price-earnings, such as trailing or forward. Specifically, we’re using a high standard here.

The graph looks at the last 12 months of earnings and shows how much you pay per dollar of earnings. This is how you can value stock, and you don’t have to worry about inflation. When earnings increase, the value of stocks should, too. Therefore, a relative valutation of price to earnings is a great way to compare stocks prices over time.

What is the Alternative?

The alternative in the year 2000 and 2008 were bonds. If you would have sold in the 2000 timeframe, the ten-year was paying over 5.5%, and inflation was reasonably low, especially during the recession. However, today we don’t have higher yields in the bond market. We’re at 1.74%, and inflation expectations are running at 3.3%. Not only is the interest rate low, but inflation is above what that interest rate is paying.

We wanted to put numbers to the story, so here is a more straightforward way of looking at it.

We are showing 33, as the highest P/E- S&P 500, looking at the past 12 months where we know there were some rough patches. The average for stocks is about 2x higher and 3x higher on the average of bonds. Therefore, bonds could be more overvalued than stocks based on historical standards. The only way to improve the P/E ratio on a bond is to have the price decrease. For stocks, the P/E ratios can improve via a drop in stock price, our fear or by earnings moving up, our hope. Earnings moving up is what we expect for stocks currently.

Earnings Season

As we enter earnings season, the expectations for earnings are high. We’re likely to see “record-breaking” numbers because we’re looking back 12 months ago. There were low to no earnings coming in due to the global pandemic.

Just as we compared bonds to stocks using a P/E multiple, we can easily compare stocks to bonds via a normal valuation for bonds by converting both to a yield. The Fed model above compares the earnings yield of stocks to the earnings yield of a bond. Whenever one is over the other, that’s the undervalued asset class, and you should invest. If we go back to the sixties, you should have been buying stocks, not bonds, based on the earnings yield. Then, to the eighties, we can see both lines matched up together. As interest rates decreased on bonds, stocks looked more attractive and were also bid up at the same rate. We can see the red line (stocks) is over the blue line (bonds) right now. Once again, not just looking at the P/E, but looking at the earnings yield, we can see stocks are more attractive versus bonds looking at the overall investment opportunity set.

Fixed Income Market Dynamics

The interest rate is the downside risk of bonds. At 1.74% on the 10-year, we’re having one of the worst starts over the last 40 years for bonds. Just another 1%, and we would see further decreases of 7-9% in the ten-year treasury. So there’s undoubtedly some downside risk in bonds.

Government spending can cause interest rates to increase because there’s only so much money that can be invested. The way that the U.S. has been offsetting a significant steep increase is by printing money, but that can cause inflation expectations, which can also cause interest rates to move up.

Ultimately, I think the risk for fixed-income is the long-term risk of inflation. Especially at low-interest rates, because if interest rates increase and you see the drop in your treasury, over time, it’s just going to appreciate at the higher interest rate and give you back all the cash you expect.

There’s never going to be any more upside to the bond from when you bought it. So if we had a $1000 bond and it pays us 1% while holding it for 20 years, you will get about $1,200 at the end. $1,200 is more than $1000, but what about that purchasing price in $1,200?

In the cost of basket goods, assume the basket today costs $100. We’re going to inflate it by 2%, 4%, and 6%.

The bond appreciated 20% at a 2% inflation, so the $100 basket of goods cost you $150. Now at 4%, it’s more than double at over $200 in 20 years. It is unusual to see 6% inflation over 20 years, but if you did, it would be over $300. Another way to think about this is to compare the bonds to the cost of goods. In other words, what is the effect of my purchasing power on that basket of goods, assuming that I’ve invested and I’m earning 1% and I’m losing 2%, 4%, or 6%.

In the 2%, you’re losing 1% to inflation each year. At 4%, you’re losing 3%, which has historically been the expected norm for inflation. Then, at 6%, you’re losing over half to inflation each year.

The income that you’re going to get on the bonds will be taxed. Typically you buy bonds where there is some cost or investment management fees. It’s not beyond the realm of possibility to be somewhere between 3-5%, especially since 3% has been the historical norm on the loss of purchasing power. We have a mission to help clients become financially self-reliant, and bonds will not fill that role. Gatewood Wealth Solutions doesn’t see bonds playing a role in preserving purchasing power and wealth at the current low interst rates.

—-

Keep up to date on Gatewood Wealth Solutions through our daily 3x3s and our weekly market insights on our YouTube, LinkedIn, and Facebook accounts.

Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

All indices are unmanaged and may not be invested directly. The economic forecasts outlined in this material may not develop as predicted, and there can be no guarantee that the strategies promoted will be successful.

All investing involves risk, including the possible loss of principal. No strategy assures success or protects against loss.

Securities and advisory services are offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise, and bonds are subject to availability and change in price.

COVID-19

The global pandemic was a central theme this quarter; going back to the beginning of the year, we can see that there’s been a significant drop in the number of cases, which has helped in the reopening. There’s also the optimism of the COVID vaccine, whether it’s Pfizer, Moderna, or Johnson & Johnson.

As the susceptible population drops, the severity of the outbreaks decline. There is a possible third wave in early Spring, but not as severe as more medical intervention options become available.

Change in Leadership

One theme that also dominated market trends in the first quarter – just as it did in Washington D.C. was a change in leadership leading to government spending and tax changes. President Joe Biden was announced as the 46th President of the United States on January 20, 2021.

President Biden called for returning the top marginal rate to 39.6%, the same rate when President George W. Bush, a Republican, was in office. The 2017 tax cut reduced that rate to 37%. Under Biden’s campaign tax proposal, those annually earning more than $1 million would have to pay higher taxes on capital gains, which typically make up the largest share of income for the wealthy. He would require estates to pay taxes on the unrealized gains on these assets.

As part of his campaign platform, Biden wanted to subject wages of more than $400,000 to Social Security payroll tax, currently capped at $142,800 for 2021. Ultimately he would rewind the estate tax policy to 2009 when the federal exemption was $3.5 million per person, and the rate was 45%. Biden would also reverse part of the 2017 tax cuts to the corporate income tax rate. He would increase it to 28%, up from the current 21%, but not as high as the 35% top rate before the Republican tax breaks.

As tax proposals change, government spending does as well. Biden proposed a $2 trillion bill on infrastructure and jobs. The plan includes everything from road repairs and electric vehicle stations to public school upgrades and training for the clean-energy workforce.

U.S. Deficit Spending is Accelerating the National Debt

Because the infrastructure bill is so high, it will impact the national debt vs. Gross Domestic Product (GDP). All of the Government spendings are starting to show up in statistics and is a concern. The blue line is the national debt. It has continued to increase over the last year. If you look at GDP, the red line, you can see that the debt is outpacing GDP by far. These numbers and the relationship between one another are essential to pay attention to due to inflation.

Inflation Fears

We know the inflation fears exist because people are no longer saying that we won’t have inflation, and we already see the signs of inflation in the graphs below.

The left graph represents the first quarter of 2021 and looks at several U.S. stock market indexes vs. several commodity indexes. Commodities for the quarter have significantly outpaced the stock market indexes. We can also see a similar trend where everything is based on the Dow Jones Industrial Average. The NASDAQ was up more than 9% above the Dow. However, it was nothing compared to the energy index, which was up 20% over the Dow.

Crowding Out Effect

The Government is pulling resources by spending and increasing prices by bidding up, known as Cost Pull. They then decide what investments to make and taxing corporations that reduce their ability to invest in growth (reducing long-term private-sector production). It is not just in the price of things; we see it in the bond market as well.

Inflation Expectations

We see inflation expectations in rising yields between 3-3.2%. Inflation is not something that the government isn’t aware of. It’s something that they are pursuing as a policy, another theme we see in the 1st quarter.

Bond Indexes

For bonds, the first quarter of 2021 was at its worst in over 40 years. The bond sell-off hit treasuries the hardest, followed by safer core and corporate bonds. Only high-yield bonds managed to end the quarter in positive territory.

Equity

Perhaps the most notable change was strength in value stocks, which have been lagging significantly in recent years. Still, the longer-term performance gaps are in favor of growth stock. Long duration is not just a concept in fixed income; it’s a concept in stocks. Stocks that are long duration tend to be growth or technology.

In the Image above we can see the long duration effect on returns. Changes in the discount rate will have a larger impact on Growth than Value and Large cap compared to small cap. There are always other factors to consider, but this showed up for the first quarter. US Large Cap Growth was negative .73%, while Large Value was a strong 10.13%. Small Value was 21.41% while, Small Growth was negative .42%. For the first quarter, the further down market cap and to the value side, the better the performance. This is not the case over the 1 and 3 year time periods. Over the last year, you wanted to be Small with a Growth tilt and over 3 years Large with a Growth tilt. Is this the start of a new rotation away from Growth stocks? This has yet to be determined.

Sector Indexes

The broadening of recovery and rising interest rates boosted cyclical stock sectors during the quarter. Energy stocks gained 31%, and financial services and basic material companies led all other sectors. Defensive sectors suffered, and technology stocks gained the least of any sector for the first time since 2016.

—-

Keep up to date on Gatewood Wealth Solutions through our daily 3x3s and our weekly market insights on our YouTube, LinkedIn, and Facebook accounts.

Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

All indices are unmanaged and may not be invested directly. The economic forecasts outlined in this material may not develop as predicted, and there can be no guarantee that the strategies promoted will be successful.

All investing involves risk, including the possible loss of principal. No strategy assures success or protects against loss.

Securities and advisory services are offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

COVID-19

In New Jersey, the COVID-19 case count is beginning to increase again. However, if you look at Texas, you don’t see anything. If news stations or individuals discuss science, they should have a working theory on how science happens.

If you were to compare New Jersey and Texas, New Jersey is right on the dot. Remember the Sun Belt states? It was predicted cases would increase based on season changes by the end of March and April 2021. This is where people go into air-conditioned environments, making it a better environment for the Corona Virus to spread. Texas will likely have a bump in June. With that being said, we only need about 60 to 70% immunity, and as more people get the vaccine, the closer to exemption we become.

What is Inflation?

From our vantage point, inflation is when we see goods increasing in price, or another way to say it is the dollar is decreasing in value. Remember, it’s not the goods that are changing. It’s the currency. Therefore, we’re inflating the money supply, which is historically the definition for inflation. Rising costs are symptoms of inflation. I think people have pushed back on the idea of inflating the money supply because there are times whenever you don’t see goods go up if you measure it by price. From our experience, there has been a significant increase in the money supply over the last decade.

Inflation Equations

Here is an equation by Milton Friedman, who said inflation is always and everywhere a monetary phenomenon.

Money (M) is the water, velocity (V) is the pipes or how everything rotates, everything in the whole (Y) is the production of tangible goods, and the pressure (P) is the gauges in the pipes or the price of items.

There is a central pipe, the banking system, including the federal reserve and the treasury on how money gets into the system. The way that it gets through the economy is not just through one single pipe. You have lumber, home building, food, car manufacturing, semi-conductors, and many other ways to get through the economy.

When you increase the money supply, everyone has their different rank order goods, and they’re competing with each other. The areas that they have are where the highest demand is going to be. The areas that tend to get the flow are usually capital markets because most of your money is already going through things you need. Then, when you get a substantial increase, the majority goes into investing. So, once you have all your food, shelter, and clothing, additional money starts to flow in a capital market, and that’s why home prices and investments have gone up.

Moore’s Law

One thing that continues to keep prices down is this notion of Moore’s law: the amount of transistors you can put on a microchip has increased every 18 months. But the way that you understand that diminishing returns has to happen as you take the absurdity is you flip it.

Another way of understanding that would be that you’re making the transistor smaller and smaller. The smallest transistor would be a size of an atom, and the chip would be about Venice’s size. At some point, you’re going to run into problems. The diminishing returns of putting more transistors on that chip interest will slow down, which means those deflationary forces through technology start to let price inflation come back into this system.

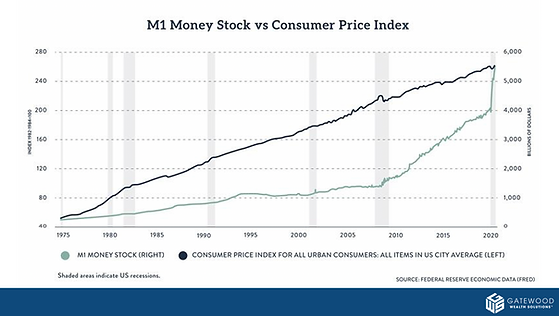

M1 Money Stock vs. Consumer Price Index (CPI)

Going back to 1975, the CPI has been climbing at the same slope. Money supply, all the way through 2008, was growing at a slower rate than inflation. The amount of money that was being created wasn’t causing the prices to go up less, but rather to go up faster. In 2008 we saw a rapid expansion in the money supply, but CPI stayed the same. Now the money supply is exceeding it, so it isn’t a one-for-one.

Asset Prices or Debt

One of the places that the rapid expansion has been going is asset prices or debt. In 1960, we had 53% of our Debt to Gross Domestic Product (GDP). We were holding 53% of our economy, our national income as debt. It went down in the 1980s to 34% because the government was inflating through the sixties and seventies. Then, by 2000 we were at 58%, moving up to 130% now. Our debt is growing at a lot faster rate than our economy, and it is our economy that pays it back.

Inflationary Outcomes

What are the ultimate outcomes whenever you inflate the money supply?

Stop Monetary Inflation

Interest rates increase above a point that velocity slows—market crash due to restructuring the economy towards consumer goods and away from capital goods.

Servicing the debt becomes impossible, and the liquidation of debt through default and restructuring—market crash does a sharp drop in money supply

Continue to Monetize the Debt with Eventual Price Inflation

A loss in the faith of the currency–hyperinflation

Weimar Republic, Venezuela, Zimbabwe, Continental

Greyback versus Green Back

Inflation Expectations

Interest rates are beginning to rise with inflation expectations, but equities are doing better than bonds for the year. The inflation expectations are now over 3% in the bond market.

It is undoubtedly true that if we look at how bonds have started the year out, this is one of the worst starts in some time for bonds. You have to remember that even though interest rates are going up, if you get a brand new bond, that might be good, but it’s the current bonds you hold that the price will go.

—-

Keep up to date on Gatewood Wealth Solutions through our daily 3x3s and our weekly market insights on our YouTube, LinkedIn, and Facebook accounts.

Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

All indices are unmanaged and may not be invested directly. The economic forecasts outlined in this material may not develop as predicted, and there can be no guarantee that the strategies promoted will be successful.

All investing involves risk, including the possible loss of principal. No strategy assures success or protects against loss.

Securities and advisory services are offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

Future Education

You’re going to start seeing costs come down, meaning spending $40,000 a year for a degree may not be the way to go. One example would be the Massachusetts Institute of Technology (MIT). They have an open source where you can look at any of the lectures online and earn a degree. Surprisingly, this is not a new innovation. Google Career Certificates is a new innovation, entering this space where they can give you employment skills that are beneficial without going through a four-year college degree. Google Certificates prepares its audiences for jobs, while MIT structures itself around an institution’s idea.

As we move forward in our progressive society, we will have more diversity with education types that could be better geared towards the individual child’s needs. Working from anywhere is where we can see more innovation, and if you can educate from anywhere, you are no longer bound to your house.

Recreational Vehicles

A recreational vehicle isn’t automation or innovation, but it is still a considerable topic regarding creation. The ability to work and educate from anywhere will likely include more significant travel. Tesla has an application called Starlink for high-speed internet in your car. Vehicles like this and services like Uber or Lyft have become the internet of things, allowing for driverless cars in the future. Imagine if your RV is moving to your destination with little or no input. You can work, sleep, eat, learn and stay connected.

It is also crucial to automate artificial intelligence (AI) driving. It’s all about the time, speed, and data we are dealing with, showing how dependent we have become on the ability for everything to be connected anywhere at fast speeds. As our world is getting into AI, people realize how important it is to have a body, allowing you to have a relationship with things around you.

Warehouses & Package Delivery

Toyota released a video imagining a team of robots allowing warehouses to use fewer people for a specific task. They see automation as a growing field in society.

This video shows the idea that all of these robots can work as one. They’re able to work in a unified manner, with the task being loading and offloading products from vehicles continuously. High-speed internet is crucial because people need to know where the robots are and what schedule they are on.

Another company that is working on this is Ford. In the video below, they show self-driving vehicles that deliver packages. However, if you don’t have a driver, you still have the last 50 feet to cover. Ford introduced Digit, a robot that does the last 50 feet for you. Digit is the solution because it’s easier as it is not easy for vehicles to go around obstacles. This robot looks more like us and most likely can take a quick screen grab once it sets that package on your front door, just like our Amazon delivery people.

Groceries

Since work from anywhere has started, you have begun to see the app Shipt and Instacart become popular, where you can order your groceries to your doorstep. Kroger is trying to automate this and make it easier for us to shop, especially since fewer people are worried about going into the building.

The whole idea is that the grocery store would become a warehouse with automation. There is a warehouse being built in Butler County, Ohio, and several more in the works. It would take an employee about 40 minutes to collect 50 items for a person; however, it would take just five minutes with robots.

Clothes, Construction, and Lumber

Folding our clothes is another topic of automation. This massive machine in the video below is probably not arriving in our houses in any time soon until it’s smaller. However, it perfectly folds your clothes for you.

What about the construction? Especially since we’re going to need different buildings to be built with highly skilled labor techniques. Here you have two examples of some masonry work.

This automation will require people to have less skill to know how to operate this machine versus the time it takes them to do it. You may see a drop in the cost of buildings being built and a need for new buildings to be more efficient for these robots to be used. This is going to put a demand on commodities because now it’s cheaper to build them. You can create more of them, which means you need more material—leading to another topic of automation, lumber.

Lumber is an example of something that can be more environmentally friendly because it is not as hard on the terrain. Now, if we have all of these machines working, what’s something that we would need more of?

Energy

Energy is very crucial in the automation process. Solar power looks very promising long-term, where the price of gathering solar energy continues to drop. We can see it plummeting on this logarithmic scale.

However, there are negatives to solar power as the actual panels use many materials, much of which is not very good for the environment. The more significant part is the storing of energy, the battery life. You have to collect the power when the sun is shining because if you need to increase your capacity, you can’t just turn a knob and have the sunshine a little bit brighter.

Short Term Concerns with Automation

There are lots of concerns with automation as our world does not like change. The Government is trying to figure out how to provide for people because they believe that this would increase unemployment. There would undoubtedly be more minor jobs for delivery, fewer jobs for construction but new jobs in other sectors.

One of the reasons this is going to be a problem is monetary and Government policy. We’re tilting the field in favor of capital procurement, creating this technology maybe a little bit early before we need it because we’ve kept interest rates so low. There is this back and forth between labor and capital, and if we tilt the field in favor of capital, it could be labor that’s moving out.

Ultimately these don’t have to be at odds with each other. If you were allowing interest rates to increase, it would become more costly to add new capital. As that capital makes it cheaper to work, and you need lower skills that bring down the cost of labor, which may sound bad at first—but considering everything else going down at a faster pace, it doesn’t necessarily hurt. Then, you would just hire people instead of capital. Therefore, the market forces can bring these together and balance them while solely making this progression.

Long Term Concerns with Automation

The long-term problem is Maslow’s hierarchy of needs. We could have everything provided for us in this situation. The shelter is cheaper than robotics and automation. The ability to have your food is more reasonable, especially if you like the idea of synthetically printing it. All those basic needs are there, but then we have safety needs. You could have robots as your security, right? There’s a lot of protection from new technology.

We start to move up in love and belonging. You can see tighter family units and smaller social groups that spend a lot more time together because we’re no longer structuring our world around a location. Then, this moves into self-esteem and self-actualization as a hierarchy.

—-

Keep up to date on Gatewood Wealth Solutions through our daily 3x3s and our weekly market insights on our YouTube,Facebook, and LinkedIn accounts.

Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

All indices are unmanaged and may not be invested directly. The economic forecasts outlined in this material may not develop as predicted, and there can be no guarantee that the strategies promoted will be successful.

All investing involves risk, including the possible loss of principal. No strategy assures success or protects against loss.

Securities and advisory services are offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

A popular reason clients come to us is that they have a large amount of cash — and want to make sure they’re investing it at a good time. Maybe they had a significant liquidity event, sold their company, exercised their stock options, were paid a large bonus, or even received an inheritance. The first question on clients’ minds is nearly always, “When and how should I invest the cash into the market?”

When people find themselves with excess cash on their hands, it can be challenging to know whether to invest now or hold the cash for a more suitable time. Part of that dilemma is psychological. It’s hard to let go of a massive amount of money and simply trust the market with it. And while it’s generally a good idea to invest all excess cash outside of someone’s cash target, there are still options for clients who aren’t comfortable doing so right away.

It comes down to whether someone is an emotional or rational investor. Neither approach is “right” or “wrong,” and we offer paths for both preferences.

What do I mean by that? Watch the video below to hear our CIO Aaron Tuttle, CFA, CFP®, CLU®, ChFC® and I explain the difference between emotional and rational investing, as well as how we can work with either preference to get your cash invested properly.

—-

Keep up to date on Gatewood Wealth Solutions through our daily 3x3s and our weekly market insights on our YouTube,Facebook, and LinkedIn accounts.

Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

All indices are unmanaged and may not be invested directly. The economic forecasts outlined in this material may not develop as predicted, and there can be no guarantee that the strategies promoted will be successful.

All investing involves risk, including the possible loss of principal. No strategy assures success or protects against loss.

Securities and advisory services are offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

No strategy assures success or protects against loss. Investing involves risks including possible loss of principal.

Air Travel Hitting an All-Time High in the Past Year

The United States has air travel picking back up, hitting the highest level in a year amid eased restrictions. An increase in air travel is very much good news, but it’s going back to that reopening theme and some inflation fears that a lot of people have as we come out of the lockdowns and recession.

Stimulus

For those receiving checks, check your account. If you have not done so already, it should be there. As most of you already know, we had the new stimulus bill (STEMI) passed last week and signed into law by president Biden. However, it has its detractor, and the most vocal regarding the STEMI is Senator Rand Paul. He followed in his father’s footsteps in the Austrian business cycle theory (the philosophy of how economies work). The detractors are about the business cycle caused by monetary policy through central banks. Usually, this does not end well if you continue to grow the economy by just throwing money into the system.

In the quote above, Senator Rand Paul was quoting the non-partisan CBO. He mentions the increase in risk for the financial or fiscal crisis, and in this situation, it could lower confidence in the U.S.’s ability to pay down debt. What he said should cause all the politicians to have some sort of pause.

Diving deeper into that CBO report, they said the reserve status of the U.S. currency is undoubtedly at risk with the amount of spending. By 2050 the amount of revenue that the government is giving, 50% of it needs to go to just pay the interest.

Infrastructure Bill

President Biden is not the first president to say we need to do infrastructure spending. President Trump campaigned on an infrastructure bill. President Obama campaigned on an infrastructure bill. However, we continue not to spend money there. The Government is talking about a $2-4 trillion stimulus bill for infrastructure after the U.S. has already spent $6 trillion in stimulus over the last year.

The administration has also stated that this infrastructure bill should have higher interest rates. So, Treasury Secretary Janet Yellen talks about the need to do this infrastructure and points out the need to fund the higher tax infrastructure bill.

The Biggest Federal Tax Hike Since 1993?

The administration is embarking on what could be the most significant federal tax hike since 1993 to finance an infrastructure plan, Biden’s climate-change initiatives, health care, and economic inequality. Bloomberg has a list of reportedly under consideration proposals, though they all likely won’t make it into the final bill. Notably, the first two bullets would effectively unwind the two most significant Trump tax cuts components.

Raising the corporate tax rate to 28% from 21%.

Paring back tax preferences for so-called pass-through businesses, such as limited liability companies or partnerships.

Raising the income tax rate on individuals earning more than $400,000.