When Mike started his consulting business, he did what many new entrepreneurs do—he operated as a sole proprietor. It was simple, required no formal setup, and allowed him to focus on building his client base.

But two years in, with business booming and $200,000 in net income on the books, Mike’s CPA asked a pivotal question:

“Have you thought about electing to be taxed as an S-corporation?”

Mike had heard the term before but didn’t quite understand how it worked—or why it mattered. What followed was an analysis that changed the way Mike ran his business and saved him thousands of dollars every year.

The Tax Breakdown: Sole Proprietor vs. S-Corp

As a sole proprietor, Mike was paying self-employment tax on every dollar of his $200,000 net income. That meant:

- Sole Proprietor Self-Employment Tax:

$200,000 × 15.3% (Social Security + Medicare) = $30,600

Ouch.

But under an S-Corp structure, things look different. Mike would pay himself a reasonable salary (let’s say $96,000) and take the rest of the profit ($104,000) as a distribution, which isn’t subject to self-employment taxes.

Here’s how the S-Corp scenario plays out:

- S-Corp Employment Tax on Salary:

$96,000 × 15.3% = $14,688 - Remaining $104,000 in profit is not subject to employment tax.

- Tax Savings:

$30,600 (Sole Proprietor) – $14,688 (S-Corp) = $15,912 saved

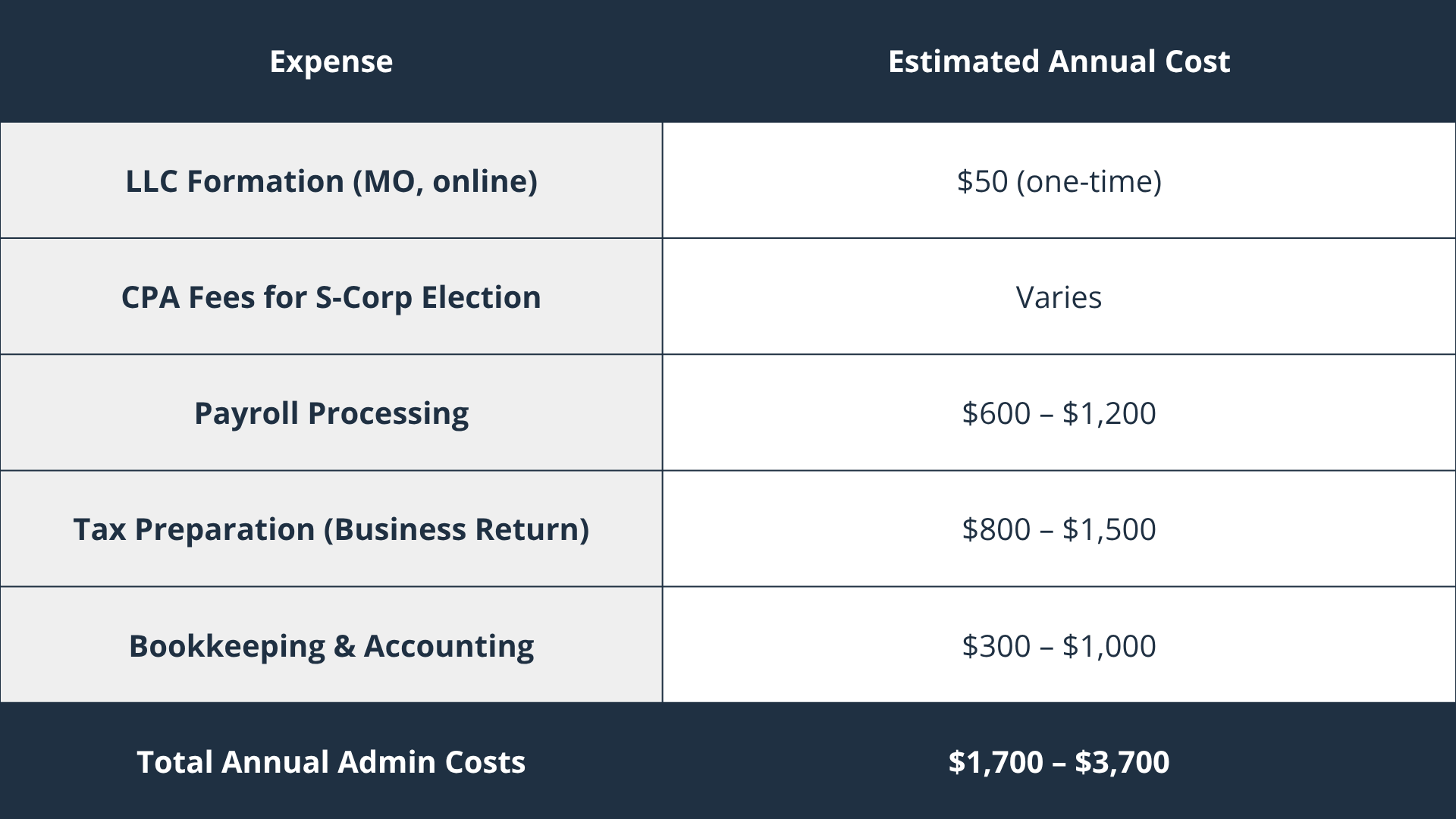

The Cost of Making the Switch

Of course, S-corporation status comes with a few additional administrative requirements:

Even after subtracting these estimated costs, Mike stood to save between $12,212 and $14,212 per year.

Bonus Tax Benefit: State Income Tax Deduction

But that’s not all. Because S-corps are pass-through entities, Mike also became eligible for Missouri’s pass-through entity tax election, allowing state taxes to be paid at the business level—rather than being limited to the $10,000 SALT deduction cap on his personal return.

This strategy gave Mike additional federal tax savings, since he could now fully deduct state taxes paid by the S-corp.

Other Advantages of Being an S-Corporation

Beyond tax savings, Mike discovered several practical and strategic benefits:

- Professionalism: Operating as an S-Corp signaled to clients and vendors that his business was established and credible.

- Liability Protection: As an LLC electing S-Corp status, he gained legal separation between personal and business assets.

- Retirement Contributions: With W-2 wages, Mike could contribute more to certain retirement plans (like a solo 401(k)).

- Ownership Flexibility: He could bring on other shareholders or investors without reworking the business structure.

- Improved Bookkeeping Discipline: Payroll, regular compensation, and distributions helped him create clearer financial records—critical for future growth or financing.

Additional Considerations When Converting to an S-Corporation

Fringe Benefits May Be Less Favorable

S-corporation owners who hold more than 2% of the company are treated differently than sole proprietors or C-corporation owners when it comes to fringe benefits.

- For example, health insurance premiums must be included in the shareholder’s W-2 wages and deducted on their individual return—not the business return.

- This approach does not reduce FICA taxes and can limit the overall tax benefit.

- The same applies to HSA contributions and certain other fringe benefits, which may not be deductible at the entity level.

Reasonable Compensation Is Required

The IRS requires that S-Corp shareholder-employees pay themselves a reasonable wage before taking distributions. This is a common IRS audit focus.

Tip: A reasonable salary should be based on industry standards, the services performed, and the time spent working in the business. In our earlier example, $96,000 appears reasonable—but this figure should be justified and documented.

State Tax Workaround – SALT Cap (PTE Election)

Some states, including Missouri, allow Pass-Through Entity (PTE) tax elections, which can help bypass the federal $10,000 cap on state and local tax (SALT) deductions.

However, this strategy comes with caveats:

- The election must be made annually and on time.

- It isn’t always beneficial, depending on whether you itemize deductions and your income level.

- Not all states allow this workaround, so consult your tax advisor to see if it applies.

Tracking Basis and Distribution Rules

S-Corp shareholders must carefully track their basis (i.e., their investment in the company).

- Distributions in excess of basis are taxable.

- Losses may be disallowed if the shareholder doesn’t have enough basis to absorb them. This becomes more complex if the business has significant debt, inventory, or variable income.

Timeline for Electing S-Corp Status

To be effective for the current tax year, you must file Form 2553 by March 15.

- If you miss the deadline, you may still qualify for late election relief, but you’ll need to follow IRS procedures.

Exit Strategy and Flexibility

S-Corp status is relatively easy to revoke if your situation changes. However, once revoked, you generally cannot re-elect S-Corp status for five years without IRS approval.

Bottom Line: Is It Time to Make the Switch?

For Mike, the math was simple: Save over $12,000 a year, protect personal assets, and run a more structured, scalable business.

If you’re earning over $50,000–$60,000 in annual net income, talk to your CPA or financial advisor about whether electing S-Corp status could be right for you. With the right structure and planning, you may save thousands each year in taxes—while building a more scalable and protected business. For many small business owners, this single decision can meaningfully boost profitability and financial efficiency—without changing the work you do.

Want to explore whether switching to an S-Corp could save you thousands too? Let’s talk.

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

This information is not intended to be a substitute for individualized tax advice. We suggest that you discuss your specific tax situation with a qualified tax advisor.

This is a hypothetical example and is not representative of any specific situation. Your results will vary.