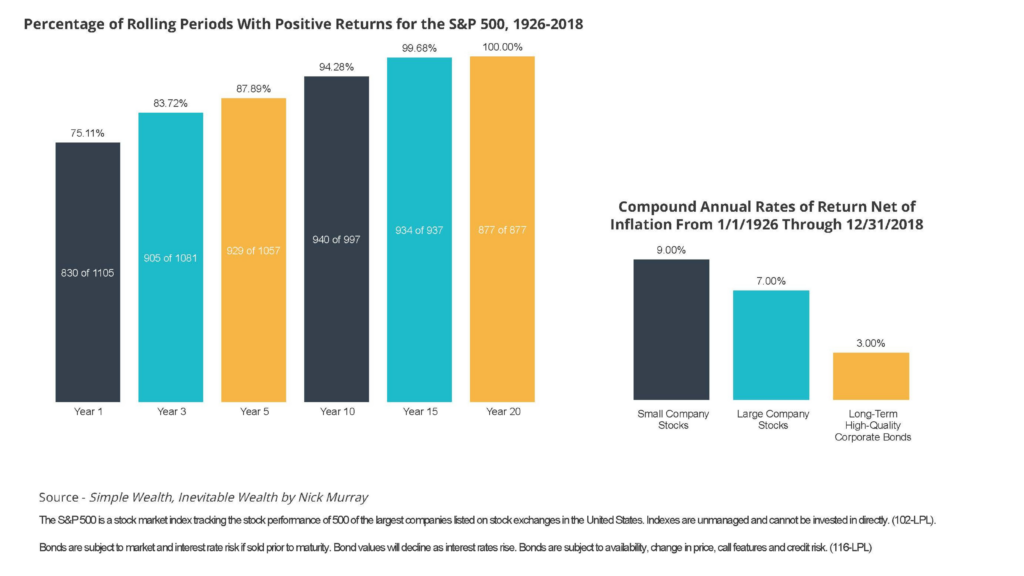

Simple Wealth, Inevitable Wealth: Nick Murray’s Timeless Principles of Portfolio Construction

When it comes to investing, simplicity and discipline often outperform complexity and constant tinkering. Few voices in financial planning have championed this notion more effectively than Nick Murray, one of the most respected minds in wealth management. His philosophy centers on long-term equity investing, behavioral discipline, and the idea that financial advisors are coaches, not market forecasters.

At Gatewood, we embrace many of these foundational principles while adding our own personalized approach to support our clients’ goals in building enduring wealth aligned with their values and purpose.

Nick Murray’s Core Principles of the “Ideal Portfolio”

Equities Are the Best Path to Long-Term Wealth

Murray firmly believes that stocks are the only reliable way to outpace inflation and generate real wealth over time. While cash and bonds may offer short-term stability, their purchasing power erodes in the long run. A well-constructed equity portfolio, in contrast, provides access to the enduring growth of businesses and economies across the globe.

Diversification Reduces Risk

Although equities are central to a strong portfolio, diversification across industries, geographies, and asset classes helps buffer against sudden market shocks. The goal? Avoid letting any single event or sector derail your long-term plan.

Bonds Have a Role—But a Limited One

According to Murray, a traditional 60/40 “balanced” portfolio is not optimal for long-term investors. Bonds, he argues, primarily serve as a psychological cushion. For those with a lengthy time horizon, over-allocating to bonds can actually increase the risk of running out of money in retirement. The risk of a loss of purchasing power is often much greater than the risk of short-term market volatility.

Investor Behavior Matters More Than Portfolio Construction

Even the best-designed portfolio can fail if an investor succumbs to panic. Murray emphasizes that market volatility is not the true enemy—emotional decisions are. Remaining invested through bear markets is the key to compounding wealth.

No Market Timing—Ever

Attempting to forecast short-term market movements is a fool’s errand, says Murray. Rather than chasing trends or reacting to market noise, investors should rely on a disciplined, repeatable process that keeps them invested for the long haul.

Retirees Need a High Allocation to Equities

One of Murray’s more controversial stances is that retirees should still hold significant equity exposure. Why? Because the greatest threat in retirement is inflation. If a retiree’s portfolio does not grow over time, their purchasing power diminishes—often severely—in the later stages of retirement.

How Gatewood Builds On Murray’s Principles

Purpose-Driven Investing

Wealth is personal. Every portfolio we construct at Gatewood aligns with our clients’ values, goals, and long-term vision. Rather than defaulting to cookie-cutter strategies, we develop personalized allocations for business owners, high-net-worth families, and individuals navigating complex financial scenarios. Your portfolio aligns with your overall financial plan and your personal preferences.

A Systematic, Process-Driven Approach

We take the behavioral aspect of investing seriously. While discipline is crucial, relying on willpower alone is risky. Instead, we employ a structured, repeatable process that helps clients avoid emotional pitfalls—particularly during turbulent markets.

Enhancing Diversification With Alternative Strategies

Equities remain the core of our portfolios, but we also incorporate alternative investments and tax-optimized strategies to help mitigate risk and enhance long-term returns. This added layer of diversification complements Murray’s model while adapting it to today’s investment landscape.

Planning for the Transition to Retirement

Rather than defaulting to a blanket recommendation for high equity exposure, we craft personalized withdrawal strategies that consider your income needs, tax exposure, and continued growth potential. A well-constructed equity portfolio provides access to the enduring growth of businesses and economies across the globe.

Data-Driven Risk Management

Discipline matters, but data does too. We use real-time financial modeling and stress testing to keep our clients prepared for the unexpected. This helps keep both your portfolio—and your peace of mind—intact, even in worst-case scenarios.

The Bottom Line: Principles + Process = Success

Nick Murray’s philosophy offers a timeless foundation for building long-term wealth. However, execution matters as much as the theoretical framework. At Gatewood, we pair Murray’s principles with our own strategic process—one designed to guide you through market ups and downs with confidence.

Long-term investing is simple, but that doesn’t mean it’s easy. If you’re looking for a financial partner who blends the discipline of a seasoned advisor with the personalization that real families and businesses need, we’d love to help. Let’s develop a plan that aligns with your purpose, your goals, and your future.

Ready to Take the Next Step?

If you’re ready to explore how these principles can translate into real-life wealth strategies for you or your business, schedule a conversation with Gatewood today. We’re here to help you build, protect, and maximize your wealth—so you can focus on living the life you’ve envisioned.

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Government bonds and Treasury bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value

Bonds are subject to credit, market, and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor’s portfolio. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Why Gatewood? Our True Differentiators

At Gatewood, we’ve spent decades crafting an experience so personal and comprehensive that it can’t be easily copied. We believe in a Firm-to-Family model where relationships span generations, backed by in-house investment management, industry-leading technology, and a genuine commitment to excellence and independence. Below, I’ll break down exactly how we stand apart—and why so many families value our insight into their long-term financial well-being.

Competitor Comparison – What Sets Us Apart

Feature

Gatewood

Typical Advisory Services Firm

Client Ownership

Firm-to-Family Model (Clients belong to the firm)

Advisor-Owned (Each advisor runs their own book)

Investment Management

In-House

Mostly Outsourced

Cash Management

Real-Time Dynamic Planning

Static One-Time Planning

Technology Spend

Industry-Leading

Minimal Investment

Advisor Age & Continuity

Multigenerational Team

Advisors Nearing Retirement

Market Risk Management

Cash Buffers, Profit-Taking

“Stay the Course” Approach

Product Sales

No Proprietary Products

Often Push Own Products

Firm Independence

No Private Equity

Many Firms Sell to PE

1. One Firm, One Family – Firm-to-Family vs. Advisor-to-Client

“Most firms operate under an advisor-to-client model, where your financial success hinges on one individual. If that person retires or leaves, you’re often left starting over. We do it differently.” – John Gatewood, CFP®, CLU®, Founder & Director of Advisor Development

True Client Ownership by the Firm

Unlike many firms, we don’t function as a set of individual advisors, each claiming their own “book of business.” Every Gatewood client is a client of the entire firm, ensuring smoother transitions and consistent care.

Dedicated Client Care Team

Instead of chasing a single busy advisor, each Gatewood family works with a specialized Client Care Team, including:

A Wealth Advisor as your relationship manager

A CFP® Wealth Planner to integrate every aspect of your financial life and provide excellent advice

A Wealth Coordinator to manage administrative details and daily service requests

Consistent Policies & Seamless Transition

This firm-wide approach standardizes the client experience. If one of your advisors steps away, the rest of the team knows you and your family intimately, ensuring continuity and confidence.

Why competitors struggle to replicate this:

They often operate under big umbrella brands, with disparate advisors who follow different strategies. Shifting to a uniform Firm-to-Family model requires a massive cultural overhaul—no easy feat.

2. In-House Investment Management – No Outsourcing, No Middlemen, No Conflicts

“We don’t outsource your portfolio to an external manager. Our Investment Committee makes decisions internally—so you can talk directly to the people managing your money.” – Christopher Arends, CFA®, CMT®, CAIA® , Chief Investment Officer

Proprietary Strategies

At Gatewood, all investment strategies are managed in-house, backed by a blend of technical analysis, quantitative trends, and daily research. We can trim profits when markets peak, maintain strategic cash reserves, and adapt quickly to shifts—all with your goals in mind.

Direct Access to Decision-Makers

Many firms separate the client from the people who actually pick stocks or structure portfolios. Not here. You have direct access to our Investment Committee to better understand the rationale behind each investment decision. This is your money, not ours. You deserve to deeply understand how we are acting on your behalf.

Why competitors can’t do this:

Either they outsource to third-party managers, or they lean on a centralized, far-off department. Both limit flexibility and create barriers to true personalization. Oftentimes, this comes with conflicts of interest and entangling relationships with fund companies. We believe keeping everything in house is essential to acting as a true fiduciary for the families and businesses we serve.

3. The Cash Hub Account & Dynamic Financial Planning – Smarter Retirement Income

“One of the biggest financial mistakes people make is selling in a downturn. Our Cash Hub approach helps you avoid that trap.” – Christina Shockley, JD, CFP®, Partner & Chief Planning Officer

Strategic Cash Reserves

We generally recommend holding 6 to 30 months’ worth of expenses—depending on one’s life stage and market conditions—to avoid forced selling during downturns. This “Cash Hub” strategy is the backbone of our planning process. Our Investment Committee sets policy for our entire firm quarterly to ensure we are consistently preparing for market downturns.

Dynamic Adjustments

We don’t set it and forget it. Life changes constantly, so our team adjusts your cash reserves in real time. Whether you’re buying a home, funding college tuition, or facing unforeseen events, we integrate new information into your plan continuously.

Why competitors can’t do this:

Some advisors push clients to invest every spare dollar (that’s how they earn fees) and rely on lines of credit for liquidity. Others do static, one-time plans that never get updated. Without ongoing, interactive planning, maintaining an optimal cash buffer is nearly impossible leaving many families unprotected for the next bear market.

4. Industry-Leading Technology Investment – A Major Barrier to Entry

“Our tech stack synchronizes planning, trading, and operations in real-time. That means no detail falls through the cracks.” – Clayton Feldman, CFA®. Director of Operations

Accountability & Transparency

Our clients can see their investment performance (net of fees), benchmarks, and fees in the Gatewood app. This should be the industry standard, but most advisors hide from this basic accountability. We believe transparency builds trust and our clients deserve to have this critical information at their fingertips.

Advanced Client Portal & Tech Stack

We offer full transparency, including after-fee performance reporting, trading activity, and tax impacts. Because our system integrates with your financial plan continuously, you see real-time progress rather than an annual snapshot.

Real-Time Adjustments

You can explore life changes—like buying a second home or altering retirement timelines—and instantly see how each decision affects your broader plan, thanks to our integrated technology.

Why competitors can’t do this:

High-level tech requires substantial investment in software, training, talent, and maintenance. Many firms see technology as a cost to cut, rather than an engine for delivering dynamic planning. We ensure our advisors and clients have robust tools, especially relating to AI capabilities.

5. Multigenerational Team – Long-Term Advisor Continuity

“With advisors ranging from seasoned specialists to new talent, we’re building a legacy of leadership that can serve you and your children for decades.” –Aaron Tuttle, CFA®, CFP®, CLU®, ChFC®, Chief Executive Officer & Partner

Future-Proofing Your Relationship

The average advisor in the U.S. is close to retirement age¹. At Gatewood, we actively recruit and develop younger advisors to ensure someone will always be here for your family’s long-term needs.

Mentorship & Development

From day one, our new advisors learn the ins and outs of our Firm-to-Family philosophy. By the time they’re leading relationships, they already know your family’s preferences and history.

Why competitors can’t do this:

Many haven’t invested in a robust talent and training pipeline. They rely on quick hires instead of cultivating advisors who fully understand their firm’s vision—or your family’s story. Our Advisor Career Path is both thorough and forward-thinking, allowing us to recruit and retain the best in the industry to serve our clientele.

6. Behavioral Economics & Bear Market Readiness – More Than Just “Stay the Course”

“It’s human nature to want to sell when things look grim. We’ve built structural guardrails—like cash buffers—to help clients stay disciplined.” –Brian McGeehon, MAcc, CFA®, CLU®. Partner & Chief Financial Officer

Equity-Focused, Cash-Backed Philosophy

We draw on insights from top financial minds and real-world experience, emphasizing equities for long-term growth potential while strategically using cash to avoid panic selling when markets dip.

Proactive vs. Reactive

Saying “ride it out” is easy, but many firms stop there. We don’t just talk about discipline; we support it with a systematic rebalancing process, profit-trimming, and well-maintained cash reserves.

Why competitors can’t do this:

They often default to cookie-cutter allocations (like 60/40 portfolios) that can lag in both bear and bull markets. Some may mention ‘behavioral coaching,’ but without tangible processes in place, it’s often an empty promise and certainly not a practice.

7. Process-Driven, Not Product-Driven – A True Fiduciary Model

“We don’t sell proprietary funds or push insurance products. We’re consultants, not product distributors.” – Jared Freese, CFP®, CLU®, CEPA, ChFC®, Wealth Advisor Manager

No Conflicts of Interest

Our compensation is straightforward advisory fees—nothing else. We’re not incentivized to push certain funds or policies. Every decision aims to benefit you, not boost a hidden commission. We publicly share our fee schedule.

Goals-Based Planning

We use a goals-based planning framework (more commonly known by our clients as the “Three Buckets”) to categorize assets by personal risk, market risk, and aspirational risk. That way, every dollar works toward a purpose aligned with your unique goals and comfort zone.

Why competitors can’t do this:

Even some “fiduciary” firms still earn commissions from certain products, like annuities. Embracing a purely process-driven model means giving up those additional revenue streams, which many traditional firms find hard to do. Our industry is full of firms claiming a fiduciary status, yet the main goal is pushing product. Doing the right thing is an easy differentiator, which we wish was not the case.

8. Commitment to Long-Term Independence – No Private Equity Sellout

“We’re structured to last for generations. Our focus on independence means client interests always come first.” –John Gatewood, CFP®, CLU®, Founder & Director of Advisor Development

Designed for Decades

We have no plans to sell Gatewood to private equity—now or in the future. Our ownership framework ensures consistent leadership and philosophy, so the values you trust today remain in place for the long haul. Our firm is owned privately by the following people:

Aaron Tuttle, Partner & CEO

Brian McGeehon, Partner & CFO

Christina Shockley, Partner & CPO

Dan Goeddel, Partner, & COO

Client Interests First

Without external investors pushing for higher margins, we can concentrate on what truly matters—your confidence, your growth, and your legacy. As private equity invades the wealth management space, we will maintain our independence.

Why competitors can’t do this?

Private equity buyouts are common in wealth management as most retiring advisors have not built a team and succession plan internally. After an acquisition, decisions often become bottom-line-driven rather than client-centric. Once independence is sold, it’s nearly impossible to get it back.

The Gatewood Difference

Our structural, philosophical, and process-driven edge permeates every facet of Gatewood—from the first conversation we have to the way we nurture relationships with your children and grandchildren. It’s not just a marketing pitch; it’s a profoundly ingrained mode of operation designed with the goal to safeguard and grow your wealth.

Ready to Experience a Different Kind of Wealth Management?

At Gatewood, we manage more than money—we build relationships that stand the test of market cycles and generational shifts. If you want consistent, sophisticated guidance free from hidden agendas, we’re here to help.

Let’s talk about your goals and how our Firm-to-Family model can help you pursue them—today and for decades to come.

Rebalancing a portfolio may cause investors to incur tax liabilities and/or transaction costs and does not assure a profit or protect against a loss. (28-LPL)

Asset allocation does not ensure a profit or protect against a loss. (34-LPL)

“This Too Shall Pass.” The Five-Year Anniversary of the Covid Crash.

“This Time it’s Different.”

The markets have given us a lot to digest lately. From shifting tariffs under the Trump administration to Elon Musk’s influence on the rise (and rollercoaster) of DOGE, plus rapid changes in federal policies—uncertainty has been the dominant theme. And if there’s one thing markets hate, it’s uncertainty. But while the headlines may suggest that “this time is different,” we’re reminded again that history often tells a reassuringly familiar story: this too shall pass.

The Uncertainty Factor

We’re seeing how quickly investors react to potential trade wars, personnel shifts, and talks of cutting wasteful or fraudulent spending. When so many unknowns hit at once, markets struggle to price it all in. Yet history reminds us that markets have weathered many storms before.

When COVID-19 first struck, markets plummeted before recovering in record time. That tells us something about how investor psychology works: once the most severe unknowns become known—even if they’re negative—markets tend to re-price and move on.

A Look at Recent Volatility

In order to put the current volatility in context, consider the COVID-19 crash.

Worst days since 2020:

March 16, 2020: -11.98%

March 12, 2020: -9.51%

March 9, 2020: -7.60%

Best days since 2020:

March 24, 2020: +9.38%

March 13, 2020: +9.29%

March 26, 2020: +6.24%

In just 33 days, from February 19 to March 23, 2020, the S&P 500 fell 33.9%—a truly historic plunge. Yet, by August 18, 2020, barely six months later, the index had fully rebounded, even though the world was far from normal.

What changed? By March 23, the uncertainty about global shutdowns was, to some degree, factored in. The market had enough information to price the situation and begin its climb.

Perspective Through History

Since 1980, the S&P 500 has had an average intra-year drop of 14%. That means, in any given year, you can expect some sharp swings. Despite these drawdowns, the index still finished positive in 34 of the last 45 years.

Yes, tariffs can rattle short-term confidence. Yes, DOGE hype can come and go. Yes, federal cuts can spark anxiety. But these are just the latest in a long history of events that cause market volatility. Historically, markets have proved resilient in the face of everything from recessions to pandemics and they tend to reward disciplined investors over time.

The Power of Diversification

The current landscape also underscores why diversification is critical.

International holdings are significantly outperforming U.S. stocks this year.

Value stocks have been outpacing growth stocks.

Fixed income offers yields comfortably in the 4% range, providing stability amid the market’s daily fluctuations.

If you’re only invested in a narrow slice of the market, you feel every bump. A well-diversified portfolio, on the other hand, can help cushion the ride when uncertainty hits.

Staying Disciplined in Uncertain Times

As the news cycle churns, it’s easy to think, “This time is different.” But if recent history has taught us anything, it’s that overreacting to short-term market swings can often do more harm than good.

Volatility is part of the investing journey.

Uncertainty is inevitable.

Long-term perspective usually wins the day.

Whether the market is panicking over tariffs, new technologies, or dramatic fiscal changes, remember that reacting out of fear can lock in losses and undermine the very reason we invest: to grow our wealth over time.

The Bottom Line

Market uncertainty is never comfortable, but it’s not new. We’ve seen swift downturns before, and we’ll see them again. Historically, markets reward those who stay focused on their goals rather than getting caught up in the headlines.

When uncertainty is high, it helps to revisit your investment plan, lean on diversification, and keep a steady hand on the wheel. While the players and policies may change from one administration to the next, what remains is the market’s ability to adapt and recover, often more quickly than we expect.

In other words: this too shall pass.

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA & SIPC.

Tax Planning Checklist for Filing by April 15, 2025

The Tax Season Rush: A Stressful Time for Busy Professionals

As the April 15 tax filing deadline approaches, many professionals, executives, and business owners find themselves overwhelmed. Between managing high-stakes projects, running businesses, traveling for work, and making time for family and social commitments, tax preparation often takes a backseat.

For many, tax season is a scramble—hunting for W-2s, 1099s, business expense records, and charitable donation receipts, all while trying to juggle their already packed schedules. Instead of being proactive about tax strategies, they often find themselves reacting to their tax bill after the fact, missing valuable opportunities to reduce their tax burden.

The reality is that taxes are one of the biggest expenses professionals and business owners face—and just like any other expense, they should be strategically managed. The good news? There’s still time to make impactful tax moves before the filing deadline.

Last-Minute Tax Moves to Reduce Your 2024 Tax Bill

While most tax-saving strategies had to be completed by December 31, 2024, there are still important actions you can take to reduce your tax liability before filing.

1. Contribute to Retirement Accounts (If Eligible)

✔ Traditional IRA Contributions(Deadline: April 15, 2025)

Contribute up to $7,000 (or $8,000 if age 50+) to a Traditional IRA and potentially deduct it from taxable income.

✔ SEP IRA Contributions (For Self-Employed Individuals)(Deadline: Tax Filing, Including Extensions)

If self-employed, you can contribute up to 25% of net earnings, with a max of $69,000 for 2024.

These contributions are fully deductible and can significantly lower taxable income.

✔ HSA Contributions (If Enrolled in a High-Deductible Health Plan)(Deadline: April 15, 2025)

Contribute up to $4,150 (individual) or $8,300 (family) and deduct contributions from taxable income.

If age 55 or older, you can contribute an additional $1,000 as a catch-up contribution.

2. Maximize Tax Deductions & Credits

✔ Review Charitable Contributions

If you made charitable donations in 2024 but did not document them, gather receipts to claim deductions.

If age 70½ or older, confirm whether you made Qualified Charitable Distributions (QCDs) from an IRA.

✔ Determine if You Qualify for the Child Tax Credit

Up to $2,000 per child, subject to income phase-outs.

✔ Claim Education-Related Tax Credits

American Opportunity Credit (for undergraduate students, up to $2,500)

Lifetime Learning Credit (for continuing education, up to $2,000)

✔ Check for Home Energy Efficiency Credits

If you installed solar panels, upgraded insulation, or replaced HVAC systems in 2024, you may qualify for tax credits.

✔ Deduct Student Loan Interest

Up to $2,500 in student loan interest may be deductible.

3. Optimize Capital Gains & Losses

✔ Use Prior-Year Capital Loss Carry-forwards

If you harvested losses in 2023, they can offset any 2024 capital gains.

You can also deduct up to $3,000 in losses against ordinary income.

✔ Confirm Tax Treatment of Any 2024 Investment Sales

If you sold investments, determine whether they qualify for lower long-term capital gains rates (0%, 15%, or 20%).

✔ Review Estimated Tax Payments (If Self-Employed or Have Large Investments)

If you underpaid estimated taxes in 2024, confirm whether penalties may apply.

The IRS waives some penalties if 90% of taxes were paid through withholdings or estimated tax payments.

4. Ensure Business Owners Take Advantage of Last-Minute Deductions

✔ Fund a SEP IRA (Deadline: April 15 or Tax Filing with Extensions)

Contribute up to $69,000 (2024 limit) to reduce taxable income.

✔ Confirm Deductible Business Expenses

Ensure home office, business mileage, travel, and client entertainment expenses are documented for deduction.

✔ Take Advantage of QBI Deduction (If Eligible)

If you own a pass-through business (LLC, S-Corp, or Sole Proprietorship), you may be able to deduct up to 20% of qualified business income (QBI).

✔ Finalize Payroll and Employee Benefit Contributions

Ensure any employee bonuses, retirement contributions, or profit-sharing payments are properly accounted for.

What to Gather for Your Tax Preparer or Financial Advisor

Pulling together the right tax documents ensures an accurate and efficient tax filing. Use this checklist to organize your records before meeting with your CPA, tax preparer, or financial advisor.

Personal Information

✔ Full Legal Names & Social Security Numbers for all dependents

✔ Filing Status: Single, Married, Head of Household

✔ Bank Information: For direct deposit refunds

Income-Related Documents

✔ W-2s from all employers

✔ 1099s (for self-employed, contract work, rental income, dividends, or investment income)

✔ K-1 Forms (for income from partnerships, S-corps, or trusts)

✔ Rental Property Income (if applicable)

✔ 1099-INT/1099-DIV (for interest and dividend income)

✔ 1099-B (for stock sales or investment transactions)

✔ Alimony Received (if applicable)

Deductions & Credits

✔ IRA Contributions (Traditional, Roth, SEP, SIMPLE IRA)

✔ HSA Contributions & Distributions

✔ Medical Expenses (if itemizing deductions)

✔ Mortgage Interest & Property Tax Statements (1098)

✔ Charitable Contribution Receipts

✔ Student Loan Interest (Form 1098-E)

✔ Education Expenses (Form 1098-T for tuition credits)

✔ Childcare Expenses (Name, Address, and EIN of Provider)

✔ Moving Expenses (if Military)

Business Owners & Self-Employed Tax Documents

✔ Profit & Loss Statement for 2024

✔ Business Expense Receipts (home office, vehicle mileage, travel, meals, equipment)

✔ Payroll & Employee Benefits Records

✔ Retirement Plan Contributions (Solo 401(k), SEP IRA, SIMPLE IRA)

✔ Estimated Tax Payments Made in 2024

Investment & Real Estate Tax Documents

✔ 1099-R for Retirement Distributions

✔ 1099-Q for 529 Plan Distributions

✔ 1099-S (if you sold a home or rental property)

✔ Schedule K-1 (if you’re a partner in a business or receive trust income)

✔ Cost Basis & Sale Proceeds for Any Investments Sold

✔ Rental Property Income & Expenses

Final Steps Before Filing

✔ Confirm Your Estimated or Final Tax Payment (If Owed)

✔ Check for Any Carry-forward Losses or Unused Deductions

✔ Consider Filing an Extension (If Needed)

Use Form 4868 to extend the filing deadline to October 15, 2025.

Note: You must still pay any owed taxes by April 15 to avoid penalties.

Don’t Wait—Plan Now to Reduce Your Tax Bill!

The weeks leading up to April 15, 2025 are crucial for filing accurately, claiming deductions, and minimizing taxes owed. The earlier you gather documents and meet with your advisor, the better positioned you are to reduce your tax burden and avoid last-minute surprises.

Need help navigating tax strategies or making final contributions before filing? Contact Gatewood Wealth Solutions today for a customized tax planning review!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA.

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC

Trump’s Proposed Tariffs: Economic Weapon or Unintended Consequences?

Introduction

Tariffs have long been a powerful but controversial tool in economic policy, influencing trade balances, industry growth, and global relations. While tariffs are often used to protect domestic industries and jobs, they can also increase costs, disrupt supply chains, and provoke retaliatory trade measures.

With President Donald Trump proposing new tariffs in his second term, it is critical to examine the potential economic benefits and consequences of these policies.

How Tariffs Work & Why Politicians Use Them

A tariff is a tax imposed on imported goods, making them more expensive and giving domestic industries a competitive edge. Governments justify tariffs for several reasons:

✔ Protecting Domestic Industries – Shields local businesses from cheaper foreign competitors.

✔ Reducing Trade Deficits – Encourages domestic consumption over imports.

✔ Leverage in Trade Negotiations – Used as a bargaining tool in international trade deals.

✔ Revenue Generation – Provides direct tax revenue to the government.

President Trump previously implemented tariffs as part of his “America First” trade policy. In his second term, he has proposed tariffs on imports from Canada, Mexico, and China, as well as reciprocal tariffs to match the duties imposed on U.S. goods by other countries.

While these measures aim to strengthen U.S. industry, they also carry potential risks, including higher consumer prices and trade retaliation from global partners.

The Pros & Cons of Tariffs: Who Wins and Who Loses?

✔ Potential Benefits of Tariffs

Job Protection & Domestic Growth – Industries like steel, textiles, and technology benefit from reduced foreign competition.

Stronger Local Manufacturing – Encourages companies to reinvest in U.S. production rather than outsourcing.

Negotiation Leverage – Tariffs pressure foreign nations to renegotiate trade agreements that benefit American businesses.

Short-Term Gains for Farmers & Key Sectors – Temporary relief from low-price competition abroad.

Example: U.S. steel tariffs helped boost domestic production but raised costs for automakers and construction firms.

❌ The Negative Effects of Tariffs

Higher Costs for Consumers – Businesses pass tariff costs onto consumers, raising prices for food, electronics, and automobiles.

Inflationary Pressures – Tariffs increase overall inflation, leading to higher interest rates and slowing economic growth.

Retaliatory Tariffs Hurt U.S. Exports – Countries like China and the EU respond by targeting American industries (e.g., soybeans, whiskey).

Disruptions to Global Supply Chains – Industries reliant on imported raw materials (e.g., automotive, tech, and manufacturing) face higher costs and production delays.

Example: The U.S.-China Trade War (2018-2020) led to higher prices on imported goods, costing the average American household $1,277 per year.

Impact on Inflation & Global Trade

One of the biggest risks of tariffs is inflation. As tariffs increase the cost of imported goods, companies pass these expenses to consumers, raising prices across the economy.

❌ Long-Term Effects: Persistent inflation pressures force the Federal Reserve to raise interest rates, slowing investment and job growth.

Globally, tariffs disrupt trade flows as companies shift production to countries with lower trade barriers. Nations impacted by U.S. tariffs may form alternative trade agreements, reducing American influence in global markets.

Example: After U.S. tariffs, China increased soybean imports from Brazil, permanently reducing U.S. market share.

Are Tariffs a Sustainable Economic Strategy?

✔ When Used Selectively: Tariffs can protect key industries and pressure foreign nations into fairer trade deals.

❌ Overuse Leads to Economic Slowdowns: Broad tariff policies raise costs, fuel inflation, and trigger global trade conflicts.

With President Trump’s proposed second-term tariffs, policymakers must carefully weigh short-term benefits against long-term risks. If implemented without strategic adjustments, tariffs could exacerbate inflation and slow economic recovery.

Conclusion: Finding a Balanced Trade Approach

Rather than relying solely on tariffs, the U.S. could consider:

✔ Trade Agreements that Promote Fair Competition (e.g., stronger deals with allies).

✔ Tax Incentives for Domestic Manufacturing (instead of penalizing imports).

✔ Investments in Workforce Development & Technology (to make U.S. industries more competitive globally).

Ultimately, tariffs should be used as a precise tool, not a broad economic policy. While they can shield domestic industries, their long-term costs—higher prices, inflation, and trade retaliation—must be carefully managed.

What’s Next?

As the Trump administration considers new tariffs, businesses and consumers should prepare for potential price increases, supply chain adjustments, and shifts in global trade dynamics. The key to long-term economic success lies in balancing protectionist policies with sustainable growth strategies.

Tariff Impacts: Positives and Negatives.

The table below outlines the potential positive and negative impacts of tariffs across various industries and countries. While tariffs can provide benefits such as protecting domestic industries and increasing government revenue, they also introduce challenges such as higher consumer prices, trade disruptions, and economic slowdowns.

Industry/Country

Positive Impact

Negative Impact

U.S. Steel & Aluminum

Higher domestic production, protection from foreign competition

Higher material costs for automakers, increased consumer prices

U.S. Agriculture

Temporary price relief for farmers, government subsidies

Retaliatory tariffs reduced exports, financial losses for farmers

U.S. Manufacturing

Encourages local production, protects jobs, less foreign competition for domestic manufacturers

Higher costs for raw materials, reduced global competitiveness

Technology Sector

Incentive to develop domestic semiconductor chip production

Increased prices for electronics, supply chain disruptions

Retail & Consumer Goods

Potential growth and support for U.S. textile industry

Higher prices for consumers, inflation risk

China

Encourages domestic consumption, reduced reliance on U.S. imports

Export losses, reduced access to U.S. markets

European Union

Increased protection for local businesses due to reduced U.S. imports

Tariffs on U.S. goods led to retaliatory measures, trade disruptions

Mexico & Canada

Possible renegotiation of trade agreements

Reduced trade volumes with U.S., higher import costs

Vietnam & Southeast Asia

New manufacturing investments, as companies seek tariff-free production

Gains at the expense of traditional U.S. trade partners

U.S. Government Revenue

Increased tax revenue for the government from tariffs

Economic slowdown from reduced trade

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Love Your Financial Future: A Valentine’s Day Guide to Aligning Your Goals

Align Your Goals, Strengthen Your Bond, Love Your Financial Future.

Valentine’s Day isn’t just about flowers, chocolates, and dinner reservations—it’s about celebrating love and partnership. This year, why not take the opportunity to strengthen your bond by aligning your financial goals as a couple? Financial planning may not sound romantic, but building a shared vision for the future is one of the most meaningful ways to show your love and commitment.

At Gatewood Wealth Solutions, we believe that love and money go hand in hand. Whether you’re navigating financial discussions or preparing for life’s biggest milestones, aligning your goals is essential to loving your financial future.

Aligning Your Goals: The Foundation of a Strong Bond

Why Financial Alignment Matters

Just like trust and communication, financial alignment is key to a healthy relationship. When couples work together to establish shared goals—whether it’s saving for a dream vacation, paying off debt, or planning for retirement—they create a foundation of understanding and partnership that strengthens their bond.

How to Get on the Same Page

Plan a Money Date Night: Use Valentine’s Day as an excuse to schedule a money date. Over dinner or a glass of wine, discuss your financial dreams and challenges.

Set Shared Goals: Identify your top priorities as a couple. Do you want to buy a home, save for retirement, or travel more?

Create a Vision Board: Visualizing your shared goals can make them feel more tangible and exciting.

Navigating Financial Discussions with Love

Overcoming Money Differences

Every couple brings unique financial habits and experiences to the relationship. While one partner might be a saver, the other could be more of a spender. Instead of letting these differences create tension, use them as opportunities to grow together.

Practice Empathy: Take the time to understand your partner’s money mindset and what shaped their habits.

Set Nonjudgmental Boundaries: Agree on spending limits or savings goals without criticizing each other’s choices.

Communicate Regularly: Make financial discussions a regular part of your relationship, not just a one-time event.

Handling Tough Conversations

Focus on shared solutions rather than pointing fingers.

Be honest about your fears and financial stressors.

Enlist a qualified advisor to provide a professional perspective when needed.

Preparing for Life’s Key Milestones Together

Every stage of life brings unique opportunities and challenges, and planning for these milestones together can bring you closer as a couple.

Buying a Home

Discuss what “home” means to each of you—location, size, and budget.

Save for a down payment together, targeting 20% to avoid private mortgage insurance.

Plan for additional costs like maintenance and taxes.

Starting a Family

Budget for medical expenses, childcare, and education savings.

Ensure you both have adequate life and disability insurance to protect your growing family.

Revisit your estate plan to include guardianship for children.

Planning for Retirement

Talk about what retirement looks like for each of you—early retirement, travel, or starting a new venture.

Maximize your retirement savings through 401(k)s, IRAs, and Roth accounts.

Explore rolling over old 401(k)s for streamlined management and increased investment flexibility.

Confidence in Wealth Activation and Enjoyment

Valentine’s Day is a time to celebrate love, but it’s also an opportunity to reflect on the future you’re building together. Transitioning from wealth accumulation to wealth activation, confidently spending down your investments during retirement, requires careful planning. That’s where Gatewood Wealth Solutions can help.

Our Team Is Your Team

Wealth Advisor: Guides you through key financial decisions.

Wealth Planner: Creates a roadmap tailored to your shared goals.

Portfolio Strategist: Aligns your investments with your risk tolerance and future aspirations.

Wealth Coordinator: Ensures every detail is executed seamlessly.

Enjoying the Life You Build Together

With a clear financial plan, you can embrace life’s key moments confidently. Whether it’s traveling the world, celebrating milestones, or simply enjoying everyday moments, your wealth plan ensures you can live with purpose and intention.

This Valentine’s Day, Commit to Your Financial Future

Love is about building a life together, and your financial future is a big part of that. This Valentine’s Day, make a pledge to align your goals, strengthen your bond, and love your financial future. Whether it’s discussing your dreams, tackling tough money conversations, or preparing for life’s milestones, each step brings you closer to the life you envision together.

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC

Unlocking the Power of 401(k)s: How Better Benefits Drive Employee Success

As we approach the first week of February, it’s an opportune time for every business leader to reevaluate and recognize the critical role that robust employer-sponsored retirement plans play in their organizations.

The Value of Employer-Sponsored Plans:

Attracting and Retaining Top Talent: In today’s competitive job landscape, a comprehensive benefits package is crucial in attracting and retaining the best talent. A well-designed 401(k) plan can set your company apart, making it a preferred employer in your industry. Employers who offer generous matching contributions see higher retention rates and more engaged employees. For example, tech companies that enhance their 401(k) offerings often report a substantial boost in employee loyalty and job satisfaction.

Boosting Employee Engagement and Productivity: Financial wellness is directly linked to employee productivity. Employers that integrate financial wellness programs and robust retirement plans often witness a reduction in financial stress among their staff, leading to enhanced productivity and overall job satisfaction. This is evident in organizations where employees are provided with tools and education to manage their finances effectively, leading to a more focused and motivated workforce.

Gatewood’s Role in Retirement Planning for Organizations:

A Commitment to Fiduciary Excellence: By offering 3(38) investment fiduciary services, a professional third party takes on the responsibility of managing your retirement plan’s investment decisions. This enables your team to delegate the complex duties of daily plan operations to help make sure that your plan adheres to the highest standards of regulatory compliance and performance. Our proactive consultations includes regular reviews and updates to keep the plan aligned with both market conditions and legislative changes.

Strategic Partnerships for Optimal Outcomes: We collaborate with leading recordkeepers such as CUNA, Fidelity, and Empower to deliver quality administrative services and sophisticated investment strategies. This helps ensure that our clients enjoy streamlined plan administration, comprehensive investment choices, and robust technology for effective plan management.

Enhancing Employee Financial Confidence:

Tailored Retirement Solutions: Understanding that one size does not fit all, we customize retirement plans to match the unique demographic and financial profiles of your workforce. Our strategies are designed not just to better secure financial futures but to also empower your employees to make informed investment decisions, enhancing their confidence in their financial planning.

Identifying Common Plan Shortcomings: Employers often face challenges that may indicate their current 401(k) plan is not meeting its potential, such as low participation rates, limited investment options, high fees, or inadequate employee engagement. Addressing these issues is crucial in maintaining a plan that truly benefits both the employer and the employees.

Key Questions Employers Should Ask: To ensure your 401(k) plan is as effective as possible, consider these essential questions:

Are the plan’s fees reasonable?

Is the plan compliant with current regulations?

Does the plan offer a diverse range of investment options?

How effective is the plan’s communication and education strategy?

What is the participation rate?

Are regular reviews and feedback mechanisms in place?

How responsive is the financial broker and how proactive in keeping the plan up-to date?

This National Employer Benefits Day, take the opportunity to reflect on how your retirement plan is shaping your business’s future. Are you fully leveraging your 401(k) plan to attract top talent and retain valuable employees? At Gatewood Wealth Solutions, we are dedicated to empowering businesses like yours with strategic, customized retirement planning solutions that foster long-term growth and stability.

Important Disclosures

This information was developed as a general guide to educate plan sponsors but is not intended as authoritative guidance or tax or legal advice.

Each plan has unique requirements, and you should consult your attorney or tax advisor for guidance on your specific situation. In no way does advisor assure that, by using the information provided, plan sponsor will be in compliance with ERISA regulations.

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC.

9 Rules of Thumb for ‘High Earners, Not Rich Yet’

Meet Lauren and Matt, a young couple in their early 30s. Lauren is a rising marketing executive, while Matt is a software engineer rapidly climbing the corporate ladder. Together, they’re doing well financially, earning a combined six-figure income. But like many H.E.N.R.Y.s (High Earners, Not Rich Yet), they find themselves juggling a mountain of financial priorities.

Between student loans, high rent, saving for a future home, and planning for kids down the road, they’re overwhelmed. They want to enjoy life now—dining out with friends, traveling occasionally, and upgrading their lifestyle—but they also know they need to secure their financial future. The challenge? They’re busy, their to-do list feels endless, and they’re not quite sure where to start.

For Lauren and Matt, the solution is simple: focus on a few key financial rules of thumb. These guidelines can serve as a framework for managing money and building wealth, even with a packed schedule.

1. Pay Yourself First

Rule of Thumb: Save at least 20% of your income before spending a dime.

Lauren and Matt realized that waiting until the end of the month to save wasn’t working. Instead, they automated savings, directing a portion of their income into retirement accounts, a house fund, and emergency reserves. By saving first, they could spend guilt-free, knowing their future was secure.

2. Protect Your Income

Rule of Thumb: Have disability insurance that covers at least 60–80% of your income.

Many young professionals overlook disability insurance, assuming nothing will disrupt their careers. But Lauren and Matt learned that their employer’s group plan capped coverage at a modest monthly maximum, far less than what they’d need. They opted to supplement it with individual disability insurance, ensuring their income—and lifestyle—would be protected in the event of an illness or accident.

3. Life Insurance: More Than You Think You Need

Rule of Thumb: If you have dependents or plan to, get 10–15 times your annual income in term life insurance.

While Lauren and Matt didn’t yet have kids, they knew it was part of their future plan. They secured affordable term life insurance policies, providing peace of mind that their future family would be cared for in the event of the unexpected.

4. Max Out Tax-Advantaged Accounts

Rule of Thumb: Take full advantage of 401(k) plans, IRAs, and Roth IRAs to build wealth tax-efficiently.

Lauren and Matt made it a priority to contribute the maximum allowable amount to their 401(k)s, leveraging employer matches where available. They also funded Roth IRAs to diversify their tax strategies, giving them flexibility in retirement.

5. Tackle Debt Strategically

Rule of Thumb: Pay down high-interest debt first while keeping student loans manageable.

Lauren and Matt made a plan to aggressively pay off their credit card balances while sticking to a manageable payment schedule for their student loans. By prioritizing high-interest debt, they freed up cash to save and invest.

6. Build Cash Reserves

Rule of Thumb: Save 3–6 months of expenses for emergencies and additional cash for specific goals like a home down payment.

The couple set aside enough money to cover emergencies, giving them confidence in their financial future. They also opened a separate savings account dedicated to their future home’s down payment, contributing to it monthly.

7. Plan for Housing Affordability

Rule of Thumb: Keep your total monthly housing expenses—mortgage, taxes, and insurance—under 30% of your gross income.

Lauren and Matt began researching homes in neighborhoods they loved, but they stayed realistic. By sticking to the 30% rule, they ensured they wouldn’t overextend themselves financially, leaving room for savings, fun, and unexpected costs.

8. Invest for the Long-Term

Rule of Thumb: Allocate the majority of your portfolio to equities to maximize growth potential over time.

With decades to go before retirement, Lauren and Matt committed to investing heavily in equities. They set up monthly contributions to their 401(k)s and IRAs, knowing that time in the market, not timing the market, was their best ally.

9. Enjoy Life, But Stay Grounded

Rule of Thumb: Budget for the fun stuff without compromising your financial priorities.

Lauren and Matt didn’t want to give up their social life or occasional vacations, but they budgeted these expenses around their savings and debt payoff goals. By prioritizing their financial health, they found a balance between enjoying today and securing tomorrow.

The Bottom Line

For busy professionals like Lauren and Matt, knowing where to start can be half the battle. These simple rules of thumb create a foundation for financial security without requiring hours of effort.

By paying themselves first, conserving their income, planning for the future, and investing wisely, Lauren and Matt are well on their way to turning their “High Earners, Not Rich Yet” status into true wealth and financial independence.

If you’re a HENRY looking for guidance, remember: the key to success isn’t just earning more—it’s using what you earn to build a life of security and opportunity. The earlier you start, the greater the rewards.

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC

Pay Yourself First: The Simple Formula for Building Wealth

Meet Sarah. Sarah earns a strong income, has a well-documented budget, and keeps track of every dollar she spends. Yet, at the end of every month, she finds herself with little to show for her efforts. Bills pile up, unexpected expenses crop up, and her savings account barely moves. Despite her best intentions, Sarah feels like she’s treading water—always working hard but never truly getting ahead.

Now, meet Emily. Emily earns about the same as Sarah, but her approach is different. Rather than budgeting every expense down to the penny, Emily follows one simple rule: pay yourself first. Every month, Emily sets aside a fixed percentage of her income—without fail—into her savings and retirement accounts. Whatever is left, she uses for bills, discretionary spending, and fun. Unlike Sarah, Emily doesn’t stress about where every dollar goes because she knows her financial future is secure.

“Pay yourself first. Then pay everyone else.”

The Power of Paying Yourself First

The difference between Sarah and Emily isn’t income or discipline—it’s strategy. Paying yourself first is the cornerstone of financial success. It’s a simple shift in mindset: instead of saving what’s left after spending, you save first and spend what’s left. This approach helps ensure you’re building wealth systematically, rather than leaving it to chance.

Here’s why this strategy works:

Automated Success: By setting up automatic transfers to your savings or retirement accounts, you remove the temptation to spend the money elsewhere.

Freedom to Spend: When you’ve already saved, you don’t have to feel guilty about how you spend the rest. Whether it’s dining out, a spontaneous trip, or a new gadget, you’ve earned the right to enjoy your money.

Compound Growth: The earlier you start saving and investing, the more time your money has to grow. Small, consistent contributions today can turn into significant wealth tomorrow.

Why Budgets Often Fail

Budgeting can feel restrictive, and for many, it’s a system that’s easy to abandon. When you budget, you’re constantly making decisions about what to cut, which can lead to frustration and, ironically, overspending. Paying yourself first eliminates this decision fatigue. By prioritizing savings, you’re securing your future without obsessing over every expense.

Avoid the Interest Trap

There are two types of people in the world: those who earn interest and those who pay it. The “pay interest” group often spends first, saves whatever is leftover (if anything), and ends up relying on credit cards or loans to fill the gaps. This cycle of debt makes everything more expensive and creates a financial treadmill that’s hard to escape.

The “earn interest” group, however, saves first and lets their money work for them. They systematically invest, avoid unnecessary debt, and benefit from the power of compounding.

Building Wealth: The Core Principles

To position yourself for financial independence, follow these basic principles:

Live Below Your Means: Spend less than you earn, no matter your income level.

Pay Down High-Interest Debt: Attack high-interest debt like credit cards first, and free yourself from the burden of compounding interest.

Systematically Save: Set a savings goal—start with 10–20% of your income—and automate contributions.

Build an Emergency Fund: Aim for 3–6 months’ worth of expenses to cover unexpected events.

Max Out Retirement Accounts: Take full advantage of 401(k) plans, IRAs, or Roth IRAs for tax-advantaged growth.

Invest in a Diversified Portfolio: Use dollar-cost averaging to invest consistently in a balanced portfolio of stocks, bonds, and other assets. Avoid chasing high-flyers or timing the market.

The Bottom Line

Paying yourself first is the simplest and most effective way to build wealth over time. It shifts the focus from what you can’t spend to what you can save, creating a sense of freedom and confidence in your financial journey.

So, the next time you receive a paycheck, remember Emily’s example. Before you pay your bills, treat yourself—your future self, that is. Because true financial security begins with one simple act: paying yourself first.

Diversify Your Investments for Long-Term Growth: Building a Smarter Portfolio

The percentage of adult Americans who invest toward retirement is nearing an all-time high at over 63%.1 These days it is far easier to pursue different investment instruments to manage and preserve wealth and over the past few decades the average working person has realized that investing isn’t only for the rich. Whether you are new to investing or have some experience, the challenge of creating a portfolio that aligns with your financial goals remains ongoing.

There are several ways to “mix” your investments. You can invest in different instruments which are also broken up into sectors (both listed below). This is generally called “diversification.” The goal of diversification is to help avoid losing significant money from investments that don’t turn out as you may have hoped. However, just because you are diversified doesn’t mean you selected a safe composition of investments. For example, if you have many different high-risk penny stocks, the diversification may not have done much to decrease the risk that you could lose money. You have to be prudent in your investment decision-making and understand how each asset works.

Some of the investment instruments people consider for their portfolio include:

Stocks – Fractional ownership interest in a company. If the company does well, the investor tends to do well, and vice versa.

Bonds – A debt security, like an IOU. Borrowers issue bonds to raise money from investors who earn interest over time.

Mutual Funds – A company that pools money from investors and invests the money in securities such as stocks, bonds, and short-term debt. Unlike ETFs, mutual funds can only be bought and sold at the end of the trading day.

Exchange-traded funds (ETFs) – A collection of securities that tracks sectors of the market or seeks to outperform an underlying index. Unlike mutual funds, ETFs trade throughout the day on a stock exchange and their price fluctuates based on supply and demand.

Fixed-income investments (that aren’t bonds, such as certificates of deposit (CDs), money market funds, and commercial paper. Sometimes preferred stock is considered fixed income since it is a hybrid security bringing together equity and debt features) – Debt instruments that pay a fixed rate of interest.

Annuities – Financial products that provide a guaranteed income stream. Investors fund the product with a lump-sum payment or periodic payments.

Derivatives – Financial contracts between two or more parties that determine their value from an underlying asset, a group of assets, or a benchmark. These tend to be higher risk investments and you want to be extremely careful and consult a financial professional before treading in these volatile waters.

Investment Trusts – A public limited company that strives to earn money through investing in other companies. Investment trusts are closed-ended funds with a fixed number of shares and can only be traded once per day at the end of the trading day. Investment trusts generally cost less to own that a similar mutual fund but are typically more expensive than an ETF.

The sectors investors select from include:

Industrials – (Stanley Black & Decker, Caterpillar, A.O. Smith, etc.)

Historically (according to officialdata.org), since the inception of the S&P 500 in 1957 the index has produced an annual return of 10.26%. If you are an individual stock picker you know that it is hard to beat the S&P 500 over time. Even the greatest investor of all time, Warren Buffett didn’t beat the S&P 500 over the past twenty years, missing matching its return by .05%.2

What is the S&P 500 index? The S&P 500 Index or Standard & Poor’s 500 Index is a market-capitalization weighted index (market capitalization is the total dollar market value of a company’s outstanding shares of stock. Market value is the amount for which something can be sold on a given market) of the 500 leading publicly traded companies in the U.S. It is considered one of the best gauges to measure top-tier American equities’ performance and the overall stock market.

Thanks to the advent of ETFs, in 1993, that mirror the S&P 500, investors are now able to buy shares of funds that aim to produce returns equal, or close that of the S&P 500. For an investor who doesn’t have the time to conduct their own research, these investment options could be part of their overall program to assist in their long-term retirement savings goals.

Another aspect of investing that is often overlooked is the power of compounding. Compounding occurs when your investment begins to earn interest on the interest as well as the principal. The longer you hold the investment the more extraordinary the compounding has the opportunity to become. Albert Einstein is credited with saying, “Compound interest is the eighth wonder of the world. He who understands it earns it; he who doesn’t pays it.” The secret to compound interest working in your favor is being patient. Morgan Housel, the author of The Psychology of Money, said, you don’t have to be particularly smart or lucky to do well in the stock market. You just have to invest according to your risk tolerance and then be patient. Warren Buffett’s partner, investing legend Charlie Munger once said, “The first rule of compounding: Never interrupt it unnecessarily.” The concept when it comes to compounding and value investing over many decades is to buy and hold and wait. But first you have to figure out your risk tolerance.

Determine your risk tolerance

Everybody has a different risk tolerance based on their income level, lifestyle, life experiences, and many more factors. It is critical that you figure out your own risk tolerance and not somebody else’s because of FOMO (anxiety that something exciting is happening and you are missing out), which can be damaging to your finances and significantly impact your financial condition and strategy.

Allocation of assets

Based on your risk tolerance and your investment goals, you want to decide how you plan to allocate your investments, for example, a percentage in stocks, bonds, etc. This includes how much you want to keep on hand in cash.

While asset allocation does not ensure a profit or protect against a loss, being consistent with your investment allocation helps to lower volatility as you maintain your portfolio diversification. It helps to stay focused on your long-term goals and reduce impulsive decision-making based on speculative news. Remember, it is impossible to predict the future of the market or its volatility as much as it is futile to try and predict natural disasters, wars, and pandemics. Things happen in life, but consistency can help you navigate those unpredictable times.

Invest in What You Know

When it comes to investing, experienced investors often reiterate the importance of investing in what you know.

Choose businesses and companies that you are familiar with their products and services.

Do your research to get an understanding of the various investment vehicles available.

Start with investments that you are familiar with.

As you become more knowledgeable about how investing works you can begin to expand your portfolio with various forms of instruments and strategies.

Work to Master the Fundamentals

It is hard to earn a dollar, but it isn’t as hard as you might believe to build wealth over time with the right guidance and strategy. And, you don’t have to have a high-income job to do it. Think of investing as you would golf, boxing, or any other sport or skilled hobby. We’ll use golf and boxing in this example: The next time you watch either sport, notice each player’s swing looks different and in boxing each fighter’s stance is unique, however, despite their different approaches they still are able to put themselves in the position to win. This is because they understand the fundamentals. Investing is the same thing. You don’t have to have the same stock portfolio as your neighbor, co-worker, relative, or investing guru to do well over time. As long as you understand the fundamentals of investing and create the mix of investments that works for you, you can be unique and manage your wealth using your own strategy.

Everybody’s retirement and financial goals are different, their strategies are unique to them, their life experiences are distinct from their friends and neighbors, and the reasons why they make the decisions they do are personal. There is no right or wrong mix of investments when you are building a portfolio, however, there are strategies that may help you lower some of the risk of investing while preserving and working to grow your wealth.

If you have invested for a while, you probably understand that there are absolutely no guarantees that you will come out on top as an investor. Most great investors from Warren Buffett to Peter Lynch had a mentor that they learned from. They weren’t just born with financial acumen. Warren Buffett learned from Benjamin Graham. Peter Lynch’s lifelong mentor was George Sullivan. Getting help so you can improve your financial situation is a step that highly motivated investors take.

Consider consulting a financial professional

Want to learn more about your retirement planning? Just as history’s most notable investors sought the help they needed, you too can do the same. Consider consulting a financial professional to help you create an investment portfolio and strategy that can align with your retirement goals.

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments. All indexes are unmanaged and cannot be invested into directly

An investment in Exchange Traded Funds (ETF), structured as a mutual fund or unit investment trust, involves the risk of losing money and should be considered as part of an overall program, not a complete investment program. An investment in ETFs involves additional risks such as not diversified, price volatility, competitive industry pressure, international political and economic developments, possible trading halts, and index tracking errors.

Because of their narrow focus, investments concentrated in certain sectors or industries will be subject to greater volatility and specific risks compared with investing more broadly across many sectors, industries, and companies.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

Footnotes:

1 Hiltzik: Passive investing is facing critics from all sides – Los Angeles Times (latimes.com)

2 Even Warren Buffett is no match for the S&P 500 – MarketWatch

Sources:

Guide to Fixed Income: Types and How to Invest (investopedia.com)

Warren Buffett Has Underperformed the Stock Market for the Last 20 Years (linkedin.com)

Quote by Albert Einstein: “Compound interest is the eighth wonder of the w…” (goodreads.com)

The Dark Side of Deals: Beware of These Cyber Monday and Black Friday Scams

Black Friday and Cyber Monday are great times to find amazing deals, but they’re also a prime time for scammers. While you’re hunting for bargains, stay alert to avoid getting caught in a scam. Here are some common tricks to watch out for so you shop safely.

Fake Websites

Sometimes a scammer may send an email with a link to a fake website that looks like a real store. Before you buy anything, check the address bar. Many scam websites use extra letters in the URL or a capital “I” instead of an “L.” For example, WaImart.com (with a capital “I”) is almost indistinguishable from Walmart.com (with a lower-case “L” appearing as “l”). These may be hard to spot, so if in doubt, use a free URL checker like Google’s Safe Browsing. Also look at the beginning of the web address; a secure web address begins with “https.”

Too-Good-to-Be-True Deals

If something sounds too good to be true, it probably is. Scammers frequently offer dirt-cheap prices on brand-name electronics or popular shoes, etc. Stay alert; compare prices with competing stores. If one site has a product for a fraction of what everyone else is offering, you’re probably being ripped off.

Fake Order Confirmations

Beware of any email that tells you that you ordered something that you didn’t. These emails try to make you panic and click a “cancel order” button. If you are at all in doubt about whether you ordered something, check your accounts directly through the store’s website.

Gift Card Scams

Gift cards make ideal holiday presents, but sometimes they may be risky. Scammers might try to sell you worthless or stolen gift cards, so buy them only from trusted stores. Never buy electronic gift cards listed for sale on online markets, or from people or entities outside a retailer’s normal distribution channels.

Shipping Scams

Shipping scams are common at this time of year. Perhaps you’ll get a message that an item is having trouble being delivered and you should pay a fee by mailing a check or by providing some personal information. Always track shipments directly from the store or the delivery company’s website.

Social Media Scams

You may get a pop-up on your social media feed advertising a huge discount code. It might be fake. Do your homework before clicking on a link or buying anything, especially if it is from a brand you aren’t familiar with.

Fake Reviews

Scammers may leave fake reviews designed to improve the perception of their item’s quality. When looking up reviews, be discerning. Most reviews should be mixed: some good, some bad. A “perfect” rating or nothing but glowing reviews might be a red flag.

Limited Time Offers

Scammers may tell you that it’s your only chance, that the deal won’t last. They are counting on you to make an impulse purchase. DON’T. Instead, go online and see if the deal is real.

By staying alert and following these tips, you may enjoy the holiday deals without falling for a scam. Stay safe and happy shopping!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

The Power of Purposeful Giving: Tax Planning Insights For Charitable Deductions

Charitable contributions are personally rewarding and also have the potential to be tax-saving opportunities. A donation is a gift, such as cash or property, that is given to a non-profit organization to help them in pursuit of their goals. The donor must receive nothing in return to get the full deduction value for their contribution.

How Does it Work?

Contributions must be claimed as itemized deductions on Schedule A of IRS Form 1040. The limit for cash donations is generally up to 60% of the taxpayer’s adjusted gross income; however, in some cases 20%, 30%, or 50% limits may apply. Deductions are permitted by the IRS for cash and noncash contributions depending on that year’s rules and guidelines which may change, so individuals should stay up to date.

Is it Counted as a Charitable Deduction?

Deductions can only be made for contributions that plan to serve a charitable purpose. The IRS also requires the organization to qualify for tax-exempt status.

What Determines a Qualified Organization?

According to the IRS, qualifying organizations include those that operate for charitable, scientific, literary, religious, or educational pursuits, or to combat child or animal abuse. There is a long list of qualified organization examples that can be found on the official IRS website.

What if I Have Noncash Gifts?