United in Wealth: How to Become a Financial Power Couple

If you’re a high earner, you may be interested in partnering with someone with similar education, income, and goals. Becoming a financial “power couple” can help you both achieve your goals sooner. Because money disputes are one of the leading causes of divorce, finding someone with whom you’re financially compatible can smooth the path of your relationship¹. Below, we discuss a few tips to help guide your joint journey.

1. Open Communication

Open communication is the gold standard for any relationship. But it becomes even more important when both partners have high incomes (especially if those jobs involve high stress). It’s not uncommon for one partner to feel insecure or jealous about another partner’s earning capacity, especially in times of uncertainty. You can build trust with your partner by getting all your emotions—even the negative ones—out on the table.

2. Set Mutual Goals

You and your partner may want to set financial goals that you both aspire to, such as saving for a house, paying off debt, investing for retirement, or starting a business. First, break down these goals into smaller, actionable steps. You can then decide who is best suited to perform each step and hold each other accountable along the way.

3. Create a Budget

One of the biggest advantages of a dual-income household is the ability to save a significant percentage of your salary—expenses like rent or a mortgage don’t double just because two people live there instead of one. This makes it easier to avoid lifestyle creep, which is discussed below.

4. Live Below Your Means

Living below your means allows you to free up funds for savings and investments. Prioritize spending on things that bring value and happiness, not just instant gratification. One rule of thumb when contemplating large purchases is to wait a week and see if you’re still thinking about it. This can help you avoid impulse buys.

5. Maximize Income

You’ll build an unshakable partnership by supporting your partner’s career goals and aspirations and celebrating each other’s successes along the way.

6. Manage Debt Wisely

Work together to manage and pay off any debts like student loans, credit card debt, or mortgage payments. Each dollar that goes toward servicing high-interest debt is a dollar that can’t be used to support your lifestyle or save for retirement, so the quicker you knock out this debt, the better.

However, debt isn’t always bad. Some types of debt can be used to leverage an entrepreneurial venture or real estate investment. In these situations, you’ll want to evaluate the pros and cons with your partner carefully and perhaps run the idea by your financial professional.

7. Protect Your Assets

For many high earners, especially those early in their careers, their biggest asset is their earning ability. This means protecting your assets by getting enough insurance coverage is crucial. This can include life insurance, health insurance, disability insurance, and long-term care insurance. You may also want an umbrella liability policy to protect yourself against claims that exhaust your other insurance coverage options.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This article was prepared by WriterAccess.

Insurance Considerations for New Parents

Becoming a parent is a life-changing experience filled with joy, excitement, and new responsibilities.

Amidst the preparations for welcoming your little one, it’s crucial to review and update your various insurance policies. This can potentially provide peace of mind and financial security for your growing family.

Health

Before welcoming your baby, review your existing policy to ensure it covers things like maternity care, and assess what coverage you’ll need for pediatric services and subsequent checkups for your baby. Having a child is a qualifying life event, so you’ll be able to add them as a dependent and adjust or upgrade your coverage as needed. Just make sure to check with your provider about deadlines and specific requirements.

Life

Life insurance is a vital component of financial planning for new parents. The primary purpose is to provide a financial safety net for your family in the event of an untimely death. So if you don’t currently have a life insurance policy, now is the time to get one. Assess finances to ensure you purchase a policy, whether it whole or term, that adequately covers the obligations you would leave behind, including mortgage or rent, student loans, and other debts.

Homeowners or renters

With the addition of baby-related items or home upgrades, your home becomes even more valuable. Update your homeowners or renters insurance policy so it covers the increased value of your possessions and property, and be sure to add any new items, including baby gear, furniture, and electronics, to your personal home inventory. Additionally, evaluate your liability coverage to protect against potential accidents or injuries that may occur on your property, such as those involving pools, trampolines, or playground equipment.

Auto

If you’re considering upgrading your vehicle to better accommodate your growing family, make sure to check with your insurance provider about premiums. Depending on the age and size of the car you purchase, your monthly cost could end up being higher or lower. It’s also a good idea to review your current auto insurance policy to ensure it provides adequate liability, collision, and comprehensive coverage, especially if you plan to partake in carpools in the future. And you’ll want to check that your policy provides coverage for a car seat, meaning your insurance provider would likely pay for the cost of a replacement should you ever be involved in an accident.

Disability

Disability insurance can help replace a portion of your income if you become unable to work due to an illness or injury. This can be a valuable tool for new parents since your ability to earn a living is crucial for supporting your child. You can purchase short-term or long-term disability insurance, either of which can go a long way toward helping you and your family through any challenging circumstance.

As new parents, it’s incredibly important to protect your growing family’s financial security. Consider consulting with an insurance professional or financial advisor who can provide valuable guidance in choosing the right policies and coverage amounts for your family’s specific needs, allowing you to better focus on the joys of parenthood without unnecessary financial worries.

Important Disclosures

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. For information about specific insurance needs or situations, contact your insurance agent. This article is intended to assist in educating you about insurance generally and not to provide personal service. They may not take into account your personal characteristics such as budget, assets, risk tolerance, family situation or activities which may affect the type of insurance that would be right for you. In addition, state insurance laws and insurance underwriting rules may affect available coverage and its costs. Guarantees are based on the claims paying ability of the issuing company. If you need more information or would like personal advice you should consult an insurance professional. You may also visit your state’s insurance department for more information.

How Will all the Retiring Baby Boomers Impact the Economy

For those unfamiliar with the “baby boom,” it is the period that stretches from 1946 to 1964, children born at the tail end of the trials and tribulations of World War II right up to the start of the Vietnam War. It is true that baby boomers are working longer than before; however, as they retire, the impact may be noticeable across the economy.

As baby boomers retire and leave the labor force, their departure could impact the economy in several ways, including:

· Productivity rates could decrease

· There could be a shortage of workers

· The costs associated with an aging population may put a strain on the economy

· Their exit may create a “talent gap” as decades of industry experience go out the door with them.

Despite the uncertainties of the economic future, baby boomers with retirement on the horizon are not sitting idle. They are taking proactive steps to prepare for this new phase of life. Here are a few measures they are implementing:

1. Postponing their retirement

It is becoming more common for baby boomers to put off retiring for a few years to put a little bit more money away. The uncertain economic landscape leaves many wary of how long their money can stretch if faced with unforeseen financial surprises like a recession or depression, consistently rising cost of living, and high interest rates.

2. Create a retirement spending budget

One way of managing your spending in retirement is to determine how much you could have on the date you want to retire. Then, determine how much you can comfortably spend versus your household income after you stop working, such as Social Security benefits, your pension (if you get one), withdrawals from a retirement account, and any other sources of income. You have a number that for your future expenses, you can focus on working toward a lifestyle where you can make that work, for example, downsizing and reducing expenses like utilities, lawn service and landscaping, excessive HOA fees, and more.

3. Review your investment portfolio

As you near retirement, there is a good chance you will have a nest egg built up. You may have a significant amount of that money in a traditional savings account, for example, but you have been interested in something that provides a higher interest rate. Consider reviewing your investment portfolio and modifying it if necessary in pursuit of your financial goals. There is no guarantee that you will earn the returns you anticipate, as all investments have risk.

4. Establish an emergency fund if you don’t have one

It is impossible to predict the future and medical care for people after retirement can be expensive. Having an emergency fund and cash available when needed can help mitigate the risk of insufficient money to cover costs such as medical events. According to Bankrate, more than 1 in 5 Americans have no emergency savings. An estimated one in three had some emergency savings but not enough to cover three months of expenses.

5. Consulting with their financial professional

Nearing retirement can be stressful, especially during uncertain times with a perceptively unstable economy. Whether you feel confident that you saved up enough over the course of your working years or not, consider consulting a financial professional to help you redesign your retirement and savings strategy and stay aligned with your long-term goals.

Important Disclosures

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This article was prepared by LPL Marketing Solutions

LPL Tracking # 577572

4 Financial Lessons from America’s Founding Fathers

America’s Founding Fathers created the foundation of a nation like no other. Each had goals and dreams, many with high expectations of what the United States of America could become. For today’s citizens, it may be possible to look back on these men and the financial insights they used as guides for inspiration. Here are some of their insights.

John Adams believed financial education and insight were critical to have. In a letter written to Thomas Jefferson, he states, “All the perplexities, confusion, and distress in America arise not from the defects of the Constitution, not from want of honor or virtue, so much as from downright ignorance of the nature of coin, credit, and circulation.” 1

There is little doubt that all Americans need to understand financial affairs, both their own and those of their country.

Compounding is a process that might build value over time. Suppose you have an investment that creates a positive return. Compounding may occur when you reinvest those returns to gather profits while building up value as long as you do not suffer a loss. For some, investing early in life enables you to have a longer period of potential growth.

Benjamin Franklin had this to say about the importance of compounding. “Remember that Money is of a prolific generating Nature. Money can beget Money, and its Offspring can beget more, and so on. Five Shillings turn’d, is Six: Turn’d again, ’tis Seven and Three Pence; and so on ’til it becomes an Hundred Pound. The more there is of it, the more it produces every Turning, so that the Profits rise quicker and quicker.” 2

While there is no quote to show it, George Washington was a man who tracked his spending carefully. During the war, he accepted the position as Commander in Chief of the Continental Army but refused to take a salary. Instead, he kept track of his expenses and requested reimbursement later. He did the same for most of his life, including managing his Mount Vernon estate. He accounted for each penny he spent.3

Thomas Jefferson shared words of wisdom on financial matters when he wrote the following to his granddaughter in 1811. He stated, “Never spend your money before you have earned it.” 4 He also wrote the following, speaking of living within your means. “But I know nothing more important to inculcate into the minds of young people than the wisdom, the honor, and the blessed comfort of living within their income, to calculate in good time how much less pain will cost them the plainest stile of living which keeps them out of debt, than after a few years of splendor above their income, to have their property taken away for debt when they have a family growing up to maintain and provide for.” 5

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

With summer on the horizon, many of us are eagerly awaiting exciting activities and well-deserved getaways. However, these adventures can also lead to higher expenses that put extra strain on our wallets. The key to enjoying a stress-free summer lies in effective budgeting. By planning ahead and managing your finances wisely, you can make the most of the season without breaking the bank.

Creating a summer budget

The easiest way to begin building your budget is by considering what expenses you already have planned, such as vacations, summer camps, or home improvements. You’ll want to factor in costs for travel, accommodation, transportation, dining out, entertainment, or any other activities you may be interested in. You can assign a specific dollar amount to each category, ensuring you account for both fixed and variable expenses.

Of course, the summer months may also bring several unexpected expenses, whether that’s surprise home or car repairs, spontaneous trips, or suddenly higher bills. So it’s always a good idea to leave extra wiggle room in your budget. Take these steps to help ensure you have the funds you need to cover all your costs this season.

Assess your financial situation

When creating a budget, first take a moment to review your income and savings. Be sure to consider all potential sources of income this summer, including your regular salary, possible bonuses, and any other side hustles you might have or could pick up. This will give you a better idea of what you can expect to bring in during the summer months and what you may be able to afford.

Besides your income, it’s also important to make note of your regular fixed monthly expenses such as rent or mortgage, utilities, and groceries. By subtracting them from your expected income, you can get an estimate of how much discretionary funds you’ll have available for summer activities, allowing you to create a more accurate budget.

Set clear goals

After you have a good idea of your income and expenses, you can create goals for what you want to do this summer. Whether you dream of a tropical vacation, exploring local attractions, or simply enjoying quality time with loved ones, having a clear vision to guide your budgeting process will help you allocate funds to the areas that matter most to you.

Managing expenses

After you’ve established your budget, you’ll need to work to keep to it by using these strategies throughout the season.

Do your research

Before booking flights, hotels, or attraction tickets, it’s important that you thoroughly research and compare prices and look for deals, discounts, or early-bird specials. Doing so may take longer, but it could make a world of a difference by helping you save money and more comfortably afford what’s ahead. If you can discover a way to cut costs significantly in one area, you can then adjust your budget by shifting that money toward another summer-related expense.

Monitor your spending

Throughout the summer, take care to monitor your spending and check to see that you’re staying on budget. If you find that you’re deviating in a certain area, you can adapt accordingly and be more mindful about where and on what you’re spending your money. Utilize spreadsheets, online tools, or budgeting apps like Mint to simplify the process. By maintaining a detailed record, you’ll have a clear understanding of where your money is going and be able to make adjustments if necessary.

Stay flexible

Because life is unpredictable, unexpected expenses may arise during the summer, so it’s essential to be flexible with your budget when you need to. Consider building an emergency fund you can use to handle unexpected costs, and prepare ways you can shift your budget as needed without derailing your overall financial goals.

While it’s always better to save in advance, it’s never too late to begin budgeting for your upcoming expenses. By taking this step now, you can better ensure that you have a fun-filled, stress-free season spent doing the things that you love.

3 Golf Tips to Keep Your Retirement Plan on Course

In golf, as in finances, there are a few rules of thumb that may improve your game: keep a level head, avoid traps, practice before trying something new and stay the course. Applying lessons from the golf course to your financial life and vice versa may help you improve your game in both arenas. Here are three tips that may help you work toward success on andoff the golf course.

Avoid Hazards

Getting bogged down in a sand or water trap may cause frustration and add many strokes to your ultimate score. While it may not be possible to avoid financial hazards, it is important to do your due diligence before making new investments or any major changes. Before taking a financial step, consider the potential outcomes and the probabilities of each. It may make sense to take several smaller steps toward your goal in some situations instead of taking a long shot that could put everything at risk. In other circumstances, the potential upside of hitting the green on the first shot might overcome the risk of missing.

Find a Good Caddie

When you are on the course, your focus should be on the game with no distractions. Just like a caddie may help you keep your gear safe and accessible and provide you with sage advice on how to work toward your goals, a financial professional might be your partner on your journey in seeking to build wealth. Consider using their assistance for things like rebalancing your portfolio, analyzing your risk tolerance and asset allocation, preparing financial statements, tax documents and other key tasks. Having the help of a financial professional may free up your time to focus on what matters, like playing more golf.

And just like with a golfer and caddie, compatibility between you and your financial professional is the key to a successful relationship. You may need to interview several financial professionals before you find one whose style and methods match well with your own.

Do Not Let a Bogey Send You Off-Course

In life and golf, mistakes are inevitable. But it is important not to let one bogey (or even one bad game) send your attitude into a tailspin. Complications inevitably arise, whether it is an investment that soured, an interruption in income, or a sudden unexpected expense that sends your budget off the rails. What matters is that these problems do not take you away from your short- and long-term goals.

Whenever you encounter a financial bogey, consider what led to it, what it means, and what actions you may take to prevent similar situations from occurring in the future. In some cases, these slips may occur due to no fault of your own, and there may not be much you may do to prevent their recurrence. Instead, you may need to plan and prepare for it. In other cases, there may have been red flags or other warning signs leading up to the mistake, which you may be better able to spot and avoid in the future.

Important Disclosures

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

Rebalancing a portfolio may cause investors to incur tax liabilities and/or transaction costs and does not assure a profit or protect against a loss.

Asset allocation does not ensure a profit or protect against a loss.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

Tips for Navigating Inflation as a Small Business Owner

Small business owners face many challenges, which may become even more significant during inflation. As inflation hit new highs in recent years, small business owners are being tested and challenged by high costs and high interest rates that have caused some to close their doors. So, how do small business owners weather the storm of inflation? Here are a few tips to help you get through it.

1. Know Your Numbers

One of the most important tips for small business owners is to know your numbers. As a small business owner, you should know the numbers on your financial statements and balance sheets and understand your cash flow. You also should always have budgets and projections, so you have a basis for comparison and should spot when things start going askew before it is too late to get back on track.1

2. Optimize Your Goods and Services

When costs and interest rates are high, supply chain issues may occur. Managing your goods and services to make a solid profit is vital. Take the time to calculate the revenue and costs of each product and service you offer to determine their gross margin and net profit. Find any poor performers and consider eliminating them so you don’t waste valuable time, material, and resources on products and services that yield little profit.1

3. Know How Inflation Might Impact Other Areas Outside Your Business

Your business is likely to be your top priority, but it is equally important to understand that inflation also affects other areas outside your business. Inflation may affect your ability to borrow, lead to a business slowdown, and drastically affect your pricing models for your products and services. Understanding all the peripheral areas affected by inflation may make your business more resilient and better able to withstand the ups and downs.1

4. Know the Difference Between Strategic and Non-Strategic Spending and Cost-Cutting

In times of disruption, it is easy for business owners to panic and begin cutting costs or spending without developing a plan to either lower company costs or outdo the competition. In either case, spending or cutting costs without following a strategy may lead to severe problems, especially during times of inflation. Always do your due diligence before implementing new spending or cost-cutting measures to ensure they align with the company’s goals and needs.2

5. Automate if Possible

The more work you automate, the more efficiently you can run your business. Perform a time study of each operation in your business. If any operations take longer than they should, or if there would be a more time-saving way to automate them, see if the cost would be worth the time it would save. You may even want to look at your daily tasks to see if there are ways to automate some of your processes to free up time to develop more business for your company.

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

Navigating Risk: Understanding Your Ability Vs. Your Willingness

Investing Is Not Just About the Numbers—It’s About Knowing Yourself

Investing is not just about the numbers; it’s about understanding yourself. Two key factors to consider are one’s ability to take risks and willingness to take risks. While both play pivotal roles in shaping your investment strategy, they cater to different aspects of your financial life.

Ability is an objective measure based on financial standing, while willingness is a subjective reflection of personal comfort and experiences. This blog aims to demystify these concepts, offering insights and a self-assessment tool to help you gauge your own risk profile.

The Ability to Take Risks: A Financial Assessment

Your ability to take risks is determined by your financial resilience—the capacity to absorb losses without derailing your financial independence or lifestyle. It’s influenced by several key factors:

Debt Levels: High debt can constrict your ability to weather financial storms, as obligations may necessitate the premature liquidation of investments at a loss.

Emergency Savings: Adequate emergency reserves provide a financial buffer, allowing you to endure investment volatility without needing to cash out investments, especially during down markets.

Time Horizon: The length of time until you need to access your invested funds can significantly affect your ability to take risks. A longer horizon allows more time for recovery from market downturns.

Insurance Protection: Proper insurance coverage (health, life, disability) shields against unforeseen financial hits, indirectly supporting a higher risk capacity.

Income Stability: Consistent and reliable income bolsters your ability to take on investment risks, providing regular contributions to offset potential losses.

Illustrating Ability with Real-World Examples

Consider Anna, a young professional with minimal debt, substantial emergency savings, and a long-term investment outlook. Her stable job and comprehensive insurance coverage position her with a high ability to take investment risks.

In contrast, Brian, nearing retirement with significant debt and limited savings, faces a constrained ability to absorb financial volatility.

Willingness to Take Risks: The Psychological Dimension

Willingness to take risks reflects your psychological comfort with the uncertainty and potential for loss in your investments. It’s shaped by:

Investment Experience: Familiarity with market dynamics can temper fear, potentially increasing your risk tolerance.

Financial Knowledge: Understanding how markets operate can empower you to take calculated risks.

Personal Experiences: Past financial successes or traumas significantly influence one’s comfort with risk.

Risk Perception: Your view of the current economic and market conditions can sway your willingness to invest aggressively or conservatively.

Personalizing Willingness Through Stories

Jennifer, an experienced investor who has weathered several market cycles, possesses a high willingness to take risks, trusting in the market’s long-term growth.

Conversely, Jack, who suffered significant losses in a past downturn, exhibits a cautious approach despite having a solid financial foundation.

Finding Your Equilibrium: Balancing Ability & Willingness

An effective investment strategy aligns your ability and willingness to take risks. Discrepancies between the two can lead to discomfort or missed opportunities. Striking a balance ensures that your investment choices resonate with both your financial reality and your personal comfort level.

Self-Assessment Questionnaire: Gauging Your Risk Profile

To better understand your own risk tolerance, consider the following statements and rate your agreement on a scale of 1 (low) to 3 (high):

My debt-to-income ratio is low, giving me financial flexibility.

I have emergency savings that cover at least six months of living expenses.

My need to withdraw from my investments is more than 10 years away.

I have comprehensive insurance coverage to protect against significant financial losses.

My income source is stable and expected to remain so.

I am comfortable with the potential of losing money in the short term for the possibility of higher returns in the long term.

I have experienced market downturns before and remained calm.

I actively seek to expand my financial knowledge and understanding of investments.

Scoring Risk Tolerance:

Ability to Take Risks: Sum scores from questions 1–5.

Willingness to Take Risks: Sum scores from questions 6–8.

Interpreting Your Scores:

High Ability and Willingness: You’re suited for potentially higher-return, higher-risk investments.

High Ability but Low Willingness: Consider educating yourself on risk management to possibly become more comfortable with taking calculated risks.

Low Ability but High Willingness: Focus on strengthening your financial base to align your investment strategy with your risk appetite.

Low Ability and Willingness: Conservative investments might be more aligned with your current financial situation and risk comfort.

Conclusion

Understanding the distinction between your ability and willingness to take risks is crucial for crafting a personalized investment strategy. By assessing both aspects through honest self-evaluation, you can navigate the investment world with confidence, making decisions that align with both your financial objectives and personal comfort level.

A seasoned advisor can offer expertise, perspective, and customized solutions that cater to your unique circumstances. At Gatewood Wealth Solutions, we stand ready to assist you in understanding and striving to optimize your risk profile.

Our team of experienced advisors is equipped to analyze your financial situation comprehensively, taking into account both your ability and willingness to take risks. We work collaboratively with you to develop a robust investment strategy that aligns with your goals and comfort level. Whether you’re seeking to maximize returns or prioritize capital preservation, we’re committed to helping you seek to achieve financial success.

Take the first step toward a more confident financial future. Reach out to Gatewood Wealth Solutions today to schedule a consultation with one of our knowledgeable advisors. Let us guide you toward a path of confidence and prosperity in your investment journey.

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Investing involves risk including loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

Am I Prepared to Sell my Business?

Jared Freese, CFP®, CLU®, ChFC®, CEPA

Certified Exit Planner & Wealth Advisor

INTRODUCTION

Meet John Carter, a seasoned business owner contemplating the sale of his successful tech startup. For over two decades, John has nurtured his business from a fledgling company into a major player in the tech industry. Recently, he’s been contemplating selling his company. While the thought of cashing in on his years of hard work is appealing, it’s mingled with a cocktail of uncertainty, nostalgia, and fear of the unknown. Selling his business isn’t just a financial decision—it’s a personal one, tied deeply to his identity and future lifestyle.

THE EMOTIONAL JOURNEY

The thought of letting go of his life’s work can be unsettling. John wonders if he is ready to part with his business and whether the sale will support his desired lifestyle. The mix of emotions is overwhelming, making it clear that selling his business is a life-altering decision that extends beyond financial gain.

KEY QUESTIONS TO ASSESS READINESS TO SELL YOUR BUSINESS

1. Why am I selling my business? Understanding the underlying reasons for selling-whether for retirement, pursuing other interests, or financial necessity-helps clarify goals and expectations.

2. Is now the right time to sell? Assessing market conditions, industry trends, and the current state of the business can determine whether it’s a favorable time to sell.

3. What is my business truly worth? A professional valuation is essential to set a realistic price and understand the factors that contribute to the business’s value.

4. What are the tax implications of selling my business? Consulting with tax professionals can help minimize tax liabilities and maximize net proceeds from the sale.

5. How will the sale affect my personal financial situation? Understanding how the proceeds from the sale will impact personal finances, retirement plans, and lifestyle is critical.

6. Who should be on my advisory team? Having the right team, including a business broker, investment banker, accountant, financial advisor, and attorney, can guide the process and ensure that all aspects are handled professionally.

7. What information will buyers want to see? Preparing thorough and transparent documentation about the business’s financial health, operations, and market position is crucial for due diligence.

8. How will I find the right buyer? Identifying whether the buyer should be an individual, a competitor, a strategic buyer, or a financial buyer influences the marketing approach and the negotiation strategy.

9. What are my plans after selling the business? Considering life post-sale, including potential new ventures, hobbies, or retirement activities, is important for a smooth transition.

10. How will the sale impact my employees and customers? Planning for the transition to maintain continuity for employees and service for customers can affect the legacy of the business and its continued success under new ownership.

HOW GATEWOOD WEALTH SOLUTIONS CAN HELP

At Gatewood Wealth Solutions, we understand the complexities involved in selling a business. Our team of Certified Exit Planners, Attorneys, Certified Financial Planner Professionals, and Chartered Financial Analysists are equipped to guide business owners like John through every step of the selling process.

SERVICES PROVIDED BY GWS

Our team of professionals provide:

· Pre-Sale Financial Planning: Aligning business and personal finances with post-sale goals.

· Business Valuation: Professional analysis to determine and justify your business’s market value.

· Tax Planning: Strategies to minimize taxes before, during, and after the sale.

· Letter of Intent Analysis: Professional review and analysis of LOI proposed deal structures.

· Investment Education: Demystifying the stock market and creating tailored investment strategies.

· Investment Management: Designing investment portfolios focused on preservation of purchasing power and income distribution.

· Emotional and Lifestyle Transitioning: Support in transitioning to life after business, maintaining an identity, and striving to achieve new goals.

OVERCOMING RELUCTANCE TO INVEST CASH POST-SALE

John Carter, like many business owners, harbors a deep-seated reluctance to invest in the stock market—a realm he perceives as volatile and beyond his control. His comfort zone has always been his business, where he could influence outcomes and directly see the impact of his decisions. This transition from a controlled, familiar environment to the unpredictable nature of the stock market is daunting.

EMPOWERING INVESTING THROUGH EDUCATION

At Gatewood Wealth Solutions, we understand the trepidation business owners feel about entering the stock market. We tackle this by educating John about investment fundamentals, crafting personalized strategies, and managing investments to generate stable income, ensuring his family’s lifestyle is maintained. Our approach is rooted in education and transparency. We provide:

· Educational Workshops and Resources: We demystify the stock market by explaining its mechanisms, the role of diversification, and the importance of asset allocation. This knowledge empowers our clients to make informed decisions.

· Tailored Investment Strategies: Recognizing that each client’s risk tolerance and financial goals are unique, we craft personalized investment strategies. These strategies are designed not just to preserve wealth but to generate income that supports your family’s lifestyle.

MANAGING INVESTMENTS FOR SUSTAINED INCOME

Post-sale, the income that once flowed from the business needs to be replaced to maintain the lifestyle John and his family are accustomed to. Our team Chartered Financial Analysts (CFA®’s) and Investment Committee at Gatewood Wealth Solutions manage investments utilizing our cash management and distribution strategy with a keen focus on generating reliable income distributions while remaining confidently invested in the market.

COMPREHENSIVE FINANCIAL PLANNING WITH FORECASTS & BENCHMARKS

To further instill confidence in the investment process, we develop a comprehensive financial plan for each client. This plan includes:

· Financial Forecasts: We project future growth and income based on current assets and investment strategies, allowing clients to see potential financial scenarios.

· Benchmarks: Regular benchmarks are set to monitor progress and make necessary adjustments. This helps our clients remain on track to meet their financial goals and can adapt to changes in the market or personal circumstances.

Our detailed financial plan with forecasts and benchmarks provides John with a clear vision of his family’s financial future, including potential growth and income from investments.

SCORING SYSTEM & CALL TO ACTION

To help you gauge your preparedness for selling your business, Gatewood Wealth Solutions offers a comprehensive readiness assessment. This assessment scores your readiness across several critical areas, helping you identify gaps and plan effectively.

WHY CHOOSE US?

Gatewood Wealth Solutions isn’t just a financial advisor; we’re a team of experienced credentialed professionals who care about you and your family. We want to be your partner in this pivotal transition. With our holistic approach, we work so no stone is left unturned in preparing you for a successful sale and a fulfilling transition into your next life’s chapter.

ARE YOU READY TO TAKE THE NEXT STEP?

Contact Gatewood Wealth Solutions today. Let us help you navigate the complexities of selling your business, ensuring you work towards accomplishing your financial goals and transition smoothly into the next phase of your life.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Investing involves risk including loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

Business value estimates are not an official appraisal of a businessʼs value and may not be provided to a third party or used for lending or third party sales. A Business Value Estimate is intended to be used as part of the business planning or personal financial planning process. Business Value Estimates are provided by a third party such that LPL makes no representations regarding the accuracy of the illustrations. LPL does not independently verify the accuracy of the information you provide or of the illustrations presented (149-LPL).

Going to the (Stock) Market: Investing Tips for Mothers

Mothers are busy people, which means saving and investing for the future can often take the back burner to more urgent priorities. Not only that, but the stock market can seem risky. During the Great Recession, the value of the average retirement account dropped greatly, by about 25%.[1] Unfortunately, if you did not start investing early in life, you could have more ground to make up for later.² Below, we’ll discuss three key tips that can help mothers clarify and work toward their financial goals.

Make Your Goals As Specific As Possible

Creating goals can be tough—especially when retirement is decades in the future. But while you may not yet be able to calculate the precise amount of money you’ll need in 2050, setting specific and measurable goals can help guide your financial path. For example, if you’d prefer to retire early, you may want to pursue aggressive investments and save a significant amount of your pay.³

By writing down why you want to invest, what your financial goals are (for the short, medium, and long term), and what assets and resources you have available to work toward these goals, you’ll have a plan to help guide your path.

Consider Different Investment Accounts Available

Not all investing is created equal, even if you’re investing in the exact same assets in each account. Some investment accounts like a 401(k) or traditional individual retirement account (IRA) are pre-tax, where contributions reduce your taxable income now but are taxed upon withdrawal; others, like a Roth 401(k) or Roth IRA accept post-tax funds and offer tax-free growth in return.⁴ There are also Health Savings Accounts (HSAs), 529 college savings accounts, and Uniform Transfers to Minors (UTMA) accounts that generally allow you to purchase investments within them.

To determine which accounts you should prioritize over others, you may want to answer a few questions with a financial professional:

● When do you hope to retire?

● What’s your effective tax rate?

● How close are you to the next tax bracket?

● Do you expect to be in a higher tax bracket at retirement than you are now?

● Do you have a pension or another source of retirement income?

The answers to these questions, and more, may help you decide between accounts that are taxable, tax-deferred, and tax-advantaged. You don’t need to commit to one of these accounts for life; one year you may want to fund your Roth IRA, the next year you could focus on your traditional IRA or 401(k).

Know Your Risk Tolerance

Investing doesn’t just require the diligence to set aside funds regularly. It also requires knowing your tolerance level when it comes to downward-trending stocks. By ensuring that all your investments fit cleanly within your risk tolerance, you can help avoid the temptation to make sudden market moves that are driven by emotion rather than logic or analysis. Generally, the higher your risk tolerance and the longer your horizon, the more aggressively you can invest.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual security. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax.

The Roth IRA offers tax deferral on any earnings in the account. Withdrawals from the account may be tax free, as long as they are considered qualified. Limitations and restrictions may apply. Withdrawals prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Future tax laws can change at any time and may impact the benefits of Roth IRAs. Their tax treatment may change.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

The Gatewood Planning Foundation: Why It Matters for Your Investment Strategy

The CFA® Designation – A Hallmark of Excellence

Are you familiar with the CFA® designation?

The Chartered Financial Analyst (CFA®) designation is considered the gold standard in the field of investment analysis and portfolio management. It is globally recognized and given by the CFA Institute, validating an individual’s competence and integrity in investment management. It signifies a rigorous course of study and a commitment to the highest ethical standards.

At Gatewood Wealth Solutions, our team includes CFA® credentialed investment professionals bring expertise and credibility to our clients’ investment strategies.

Not All Strategies are Created Equally

In the realm of financial advisory services, not all strategies are created equal. While many advisors opt to delegate investment management to outside money managers or rely on predetermined strategies within their firms, others take a more passive approach by simply allocating funds to passive or index funds and ETFs, often without active portfolio management tailored to the individual’s total asset mix and risk profile.

At Gatewood Wealth Solutions, we take a different approach. We use the CFA® Goals Based Planning Methodology for Portfolio Management in which a client’s assets are first categorized into three different buckets based upon the type of risk they face.

This approach allows us to provide personalized investment strategies that align with our clients’ needs and aspirations, rather than adopting a one-size-fits-all approach.

Let’s break down each bucket:

The Personal Risk Bucket

Purpose:

The first bucket is for low risk liquidity. It helps us make sure we have enough cash so we can weather any economic storm. We typically recommend 6-30 months of cash depending upon one’s life stage. This bucket is designed to cover essential needs and core lifestyle expenses. It’s the foundational component of one’s wealth and aims to ensure that even in adverse market conditions, an individual or family can maintain a basic standard of living without having to liquidate assets at the wrong time.

Asset Types:

Typically, this bucket includes assets with low volatility and risk: cash, high-quality short- to intermediate-term bonds, fixed annuities, and other conservative assets. It also includes one’s primary residence.

Risk Profile:

The focus here is on preservation of principal and liquidity, so assets in this bucket generally have minimal exposure to market downturns. The expected return of these assets is below inflation.

The Market Risk Bucket

Purpose:

The market risk bucket is essentially your “core retirement bucket”. It’s the net present value of all the cash you’ll need in retirement. The goal is not preservation of principal, but preservation of purchasing power. Inflation is best hedged with a diversified investment portfolio. The goal for this bucket is meant for generating returns that will outpace inflation and grow wealth over time.

Our aim with this bucket is to keep up with the benchmarks rather than try to drastically outperform the market. This way, as families navigate their way through retirement, education, and other life goals, their capital account can keep up with the growth of these expenses. It addresses the need for long-term financial security beyond just the essential needs covered in the personal risk bucket.

Asset Types:

This bucket contains a diversified mix of assets that include equities, longer-term bonds, mutual funds, ETFs, and other traditional investment vehicles.

Risk Profile:

This bucket has a moderate to high risk, with the understanding that market fluctuations can impact its value in the short to medium term. However, over longer periods, it’s expected to provide positive real returns. The expected return is above inflation.

The Aspirational Risk Bucket

Purpose:

Anything in excess of the first two buckets we consider aspirational. This is the “swing for the fences” bucket. The goal is to achieve substantial or outsized returns that greatly exceed the market and can move the individual up the wealth spectrum. However, it should be money that an individual can afford to lose without affecting their basic standard of living or long-term financial security.

Asset Types:

These are illiquid assets like a business or real estate, or concentrated assets like a single stock or equity compensation. It also includes high-risk, high-reward investments like startups, speculative stocks, and hedge funds.

Risk Profile:

This bucket is high risk, and there’s a significant chance of loss. The expected return is to greatly exceed the market and inflation.

Putting It All Together

What is our ultimate strategy with these buckets when helping clients pursue financial independence?

We first want clients to enter retirement with no debt, their homes fully paid for, and enough cash in their personal risk bucket to weather any economic storm and insulate their portfolios from being liquidated at the wrong time.

Next, we want their market risk bucket fully funded with the net present value of all their future cash needs in retirement invested in a diversified portfolio that when stress-tested they have a 90% or better chance of never running out of money.

Anything in excess of this bucket can be invested for legacy planning or a cause that is important to them.

It is important to remember that “wealth is made through concentration but preserved through diversification”.

Conclusion

The beauty of this approach is in its intuitive separation of assets based on their purpose and risk. By allocating wealth across these three buckets, individuals can ensure they’re covered for basic needs, have a strategy for long-term growth, and can pursue high-reward opportunities without jeopardizing their fundamental financial security.

Stepping Up to the Plate: Four Baseball Money Lessons

Baseball and financial management can have more in common than meets the eye. Below, we discuss four key lessons that investors—and everyone else—can learn from America’s favorite pastime.

Diversification of Assets is Critical

Having nine power-hitters who are weak in the outfield can help your team rack up high scores—but may not be enough to win the game. Just as you want your baseball team to include a good mix of a variety of skills and abilities, you should want your investment portfolio to include a diverse mix of stocks and more conservative assets, domestic and international assets, and tax-deferred and tax-advantaged accounts.

And like any good manager, it’s also important to have solid, identifiable expectations of the assets in your portfolio and to know when to cut certain “players” loose. Whether this means selling an asset once it hits a certain price or engaging in more complex strategies like tax loss harvesting, knowing when to call it a game can be the key between winning and losing.

You Need a Plan to Manage Losing Streaks

Few teams are able to consistently stay on top; even the best franchises have gone through tough times. And if the Chicago Cubs’ 107-season World Series drought is any indication, baseball can be full of some long down periods.1

Investors and baseball fans should be prepared for these down periods, no matter when they occur. Look back at historical statistics to reassure yourself that these events happen periodically, and with good planning and a bit of luck, winning seasons can come back. Having a plan to get yourself through these slumps can help investors and sports fans weather even the most discouraging times.

Try to Avoid One-Hit Wonders

Who doesn’t love to see a player blast a 500-foot home run, or watch a penny stock or crypto coin increase by over a thousand times in value nearly overnight? While these types of opportunities are fun to watch and present great feel-good stories, having a portfolio composed of power-hitters can also leave you vulnerable to major fluctuations in value.

All investments have some degree of risk, but it’s important for these risks to be compensated—in other words, investments that have a likelihood of increasing in value that corresponds to their risk, not those that will depend on overcoming the slimmest of odds to create a small group of lottery winners.

Take Advantage of the Seventh-Inning Stretch

The seventh-inning stretch gives fans an opportunity to get a brief change of scenery to focus on the last couple of innings of the game. Investing for years without setting aside time to evaluate your asset allocation, your tax reduction strategies, and your retirement plans can leave you scrambling once it’s time to make decisions about your future. Give yourself a virtual “seventh inning stretch” by stepping back and taking a holistic look at your finances so that you can buckle down with renewed focus.

With a solid game plan and prudent evaluation of risk, you’re ready to get started!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

GWS Planning Services – Where Your Financial Dreams Become Our Mission

At Gatewood Wealth Solutions (GWS), we understand that financial planning is more than just numbers on a page; it’s the roadmap to your dreams, security, and legacy. It’s about the confidence that comes from knowing you’re prepared for the future, the excitement of seeing your goals within reach, and the comfort of knowing you’re not alone in this journey.

At Gatewood Wealth Solutions, we are committed to providing you with the highest level of personalized financial planning services. We believe in building a secure financial future for every client, no matter the size of your investment with us.

Why Our Planning is Invaluable:

Embarking on the path to financial freedom can be daunting, but with GWS, you’re not just getting a service; you’re gaining a partnership that cherishes your aspirations as much as you do. We charge a planning fee for accounts under $500,000 because the depth and breadth of our work necessitate it. This fee enables us to dedicate the necessary resources to craft a financial plan as unique as you are, ensuring we can operate at the highest standards of service and expertise. We invest in your future so that you can enjoy the present, secure in the knowledge that every aspect of your financial well-being is being meticulously managed.

Our commitment is to provide you with a personalized financial plan that includes retirement planning, insurance management, investment strategy, cash flow optimization, tax efficiency planning, estate planning, education funding, and debt management. These comprehensive services are designed to bring you closer to your financial goals, no matter the complexity of your needs.

Client Stories of Success:

Gatewood Wealth Solutions was founded in 1981, and since then, we have had the privilege of witnessing numerous success stories by being a steadfast guide and support for our clients during pivotal life events. We have navigated them through both challenging and prosperous times, tackled complexities, simplified matters, and stood by their side during moments of adversity and satisfaction.

Please click the link below to see profiles of clients we have served:

Our fee structure is designed to reflect the value and expertise we bring to your financial life, especially for clients with account balances under $500,000. We have implemented a financial planning fee which is composed of a $3,000 upfront fee and a $1,500 annual fee for accounts below $200,000, and a $3,000 upfront one-time fee for accounts between $200,001 and $500,000.

Here are the key reasons why this fee model is beneficial for you:

Comprehensive Planning: We undertake an in-depth analysis of your financial situation, including retirement planning, investment management, and more, to create a plan that is as unique as your fingerprint.

Breadth of Expertise: Our team of Certified Financial Planning® professionals and other specialists is equipped to manage complex financial situations, offering advice on tax efficiency planning, estate planning, and other specialized areas.

Personalized Attention: Your dedicated Wealth Planner ensures that your individual needs are met with the utmost care and attention.

Continual Monitoring and Adjustment: Financial landscapes change, and so do your life circumstances. Our ongoing fee allows us to proactively adjust your financial plan to align with these changes, ensuring you remain on course to achieve your goals.

Resource Allocation: The fee ensures that our firm can continue to allocate the necessary resources and tools that facilitate the high-quality services you deserve.

A Fair Model: For accounts under $500,000, the cost of providing in-depth financial planning services can exceed the income from typical asset-based advisory fees. Our model allows us to offer these services at a break-even or a mild profit, maintaining the sustainability of our high-caliber advisory service.

Your Partner at Every Step:

We understand that fees are an important consideration. This is why we want to be upfront about the costs associated with managing your wealth. Your trust in us is paramount, and we strive to ensure that every dollar you invest in our services brings you value, security, and confidence your financial goals and dreams can be realized.

Our commitment to your financial well-being is unwavering, and we invite you to discuss with us how our comprehensive advisory services can make a difference in your life.

Thank you for your understanding and trust. We are here to help you navigate your financial journey with confidence and clarity.

Building Financial Resilience: Determining Emergency Cash Reserves

At Gatewood Wealth Solutions, we prioritize empowering our clients with robust financial strategies, including effective cash management to weather market uncertainties. Understanding the importance of maintaining liquidity during bear markets while remaining confidently invested for the long-term, we review and update cash needs regularly. Here’s how we determine appropriate emergency reserves tailored to different life stages using our Gatewood Rules-of-Thumb:

Cash Management: Pursuing Stability During Market Fluctuations

The primary strategy is to maintain sufficient cash reserves for liquidity needs, especially during bear markets. By holding targeted cash reserves during one’s financial journey, individuals can mitigate the risk of selling investments during down markets and remain confidently invested for the long-term.

Determining Emergency Cash Reserves by Life Stage

Emergency reserve targets are based upon an individual’s life phase and total monthly expenses.

We follow the Gatewood Rules-of-Thumb below for the number on months’ worth of total household expenses one should keep in cash:

Life Phase 1 – Early-Career Accumulation (3-6)

Life Phase 2 – Mid-Career Accumulation (6-18)

Life Phase 3 – Late-Career Nearing Retirement (12-24)

Life Phase 4 – Retirement Income Distribution (18 – 30)

We then determine one’s near-term lump sum expense needs. These include significant financial commitments, such as making a down payment on a new house, buying a new car, funding a home renovation project, or covering tuition fees for a child’s education.

Calculating the Cash Total Target

To determine the total cash target, we assess:

Emergency Reserves (3-30 Months’ Expenses – Life Phase Based)

+ Near-Term Lump Sum Expense Need (0-24 Months from Now)

= TOTAL CASH TARGET

Conclusion

By targeting emergency cash reserves according to your life stage and financial needs, we aim to provide investor confidence during economic uncertainties. Contact Gatewood Wealth Solutions today to explore how we can tailor a cash management plan to align with your specific financial goals and aspirations.

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

The Evolution of GATORS: Gatewood Wealth Solutions Pillars of Culture

Aaron Tuttle, CFA®, CFP®, CLU®, ChFC®

Chief Executive Officer

INTRODUCTION

At Gatewood Wealth Solutions (GWS), our journey is defined by more than just financial success—it’s about fostering a culture that inspires growth, integrity, and resilience. At GWS, culture isn’t just a buzzword—it’s the heartbeat of our organization.

But how did we arrive at this ethos? Let’s take a stroll down memory lane to uncover the origins of our distinctive culture and the birth of the GATORS. Our journey towards cultivating a vibrant and values-driven culture began with the passion and dedication of our founder, John Gatewood. He instilled in us a commitment to excellence, integrity, and continuous improvement.

ORIGINS OF THE GATORS

Our founder, John Gatewood, had a keen eye for detail and an unwavering commitment to excellence. When he corrected errors or provided guidance, it became known as being “Gatored.” This dedication to improvement laid the foundation for our core values, which would later be encapsulated in the acronym GATORS.

CRAFTING THE GATORS

As the firm’s ownership changed hands, there was a collective desire to formalize our values. Thus, the GATORS were born—a set of guiding principles that reflect our commitment to excellence, trust, ownership, resilience, and seeking sustainable solutions. These values aren’t just words on a page; they’re the fabric of our culture, shaping how we interact with each other and serve our clients. From leadership to frontline, every team member is measured by these values.

GROWTH – is on the other side of adversity: Commit to a lifetime of learning and becoming a better version of you, both personally and professionally. Becoming comfortable can lead to complacency, push yourself outside of your comfort zone and embrace change.

ATTITUDE – is an expression of your values, beliefs, and expectations. Make it great: Be quick to admit mistakes and take corrective action. Be willing to give and receive positive and constructive feedback. Be responsible for your words and actions.

TRUST – is earned over 1,000 actions but lost in 1: How consistently do I keep my promises and act with honesty in all situations. Do I demonstrate reliability over time and am I willing to take responsibility for my actions. Am I transparent with my fellow team members?

OWNERSHIP – because you are more than your job title. To the client, you are the company: You are responsible for learning, doing, improving, and advancing your own career. You are responsible to know and follow GWS policies and procedures. No one is above any job, if something needs to be done, do it. Don’t make it someone else’s responsibility.

RESILIENCE – never give up! When you fall 7 times, get up 8 times. How effectively do I handle unexpected challenges and maintain a positive outlook? How determined am I to keep trying despite obstacles and failures?

SOLUTIONS – not answers: When faced with an obstacle, seek the solution to the problem, not just an answer that provides a temporary resolution.

WHY IT MATTERS

Our culture isn’t just about us—it’s about our clients and our team members. For our clients, it means entrusting their financial futures to a team that embodies integrity, resilience, and a relentless pursuit of excellence. For our team members, it means being part of a workplace where they feel valued, empowered, and inspired to make a positive impact.

LEARN IT! LIVE IT! DEFEND IT!

At GWS, our culture isn’t just a set of guidelines—it’s a way of life. We breathe life into our values, defending them fiercely and embodying them in everything we do. By embracing the GATORS, we not only create a better workplace but also deliver superior service to our clients.

As we continue to uphold the legacy of excellence and integrity that defines Gatewood Wealth Solutions, we invite you to join us on this journey. Learn it. Live it. Defend it. GATOR up!

At Gatewood Wealth Solutions, we’re not just about preparing for the best; we’re about being ready for the worst. Our approach to retirement income planning revolves around a core philosophy: keeping our clients “Bear Market Ready, but Bull Market Positioned.” In this blog post, we’ll delve into our robust methodology for cash management in retirement, highlighting the importance of cash reserves and strategic investment planning.

Understanding the Cash Target

Our firm has worked hard to develop an approach that allows us to pinpoint exactly where that “sweet spot” is, based on clients’ expenses, life stages, and our investment committee’s outlook on the market. Our financial planning and investment management teams work closely together to ensure no stone goes unturned in making this assessment.

The cornerstone of our approach is what we call the “Cash Target.” This is the amount we recommend our clients keep readily available in cash to weather market downturns without the need to sell off investments at unfavorable times. Determining this Cash Target involves a meticulous process that takes into account various factors such as annual expenses, income, market conditions, and life stages.

Steps to Calculate the Cash Target

1. Assess Annual Expenses: We start by evaluating our clients’ total annual expenses, including lifestyle costs, taxes, insurance, and other financial obligations.

2. Review Income: Next, we analyze the client’s income streams, ensuring we have a clear picture of their financial inflows.

3. Incorporate Market Outlook: Our Investment Committee routinely evaluates market conditions to adjust the Cash Target Timeframe. This is the recommended duration, in months, for which one should hold enough cash to cover total expenses, tailored to the current economic environment

4. Calculate the Cash Target: Using a specialized formula, we compute the precise number of months required to cover one’s total expense needs, subtracting regular income received. This Cash Target is based on the client’s expenses, income, and the designated Cash Target Timeframe.

5. Fund the Cash Hub Account: Once the Cash Target is determined, we allocate funds accordingly, so our clients have the necessary cash reserves in place.

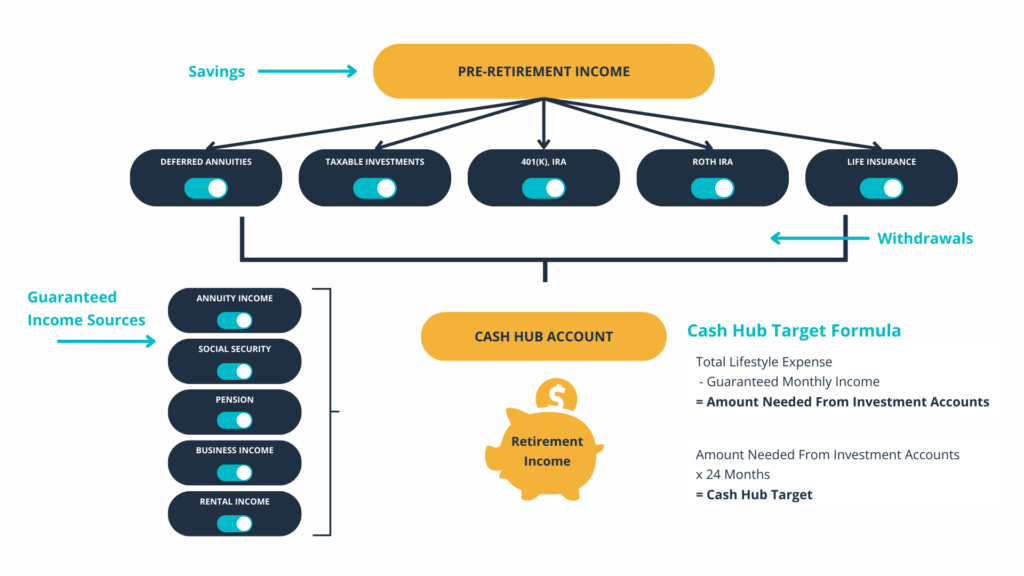

Retirement Income Distribution Planning

The cash hub account is just one small part of our overall distribution planning approach, which you can see below. Our planning team constantly turns these funnels on and off based on our clients’ specific financial situations and life goals. We can make sure we correctly put our clients’ money to work for them while maximizing their tax-saving strategies.

Cash – Invest or Keep?

Understanding the role of cash in retirement is crucial. While investments offer growth potential, cash provides stability and liquidity, acting as a safeguard against market volatility. By maintaining an adequate cash reserve, individuals can avoid the need to sell off investments during market downturns, thus preserving their long-term financial security.

Real Life Example

Consider Jane Smith, who illustrates the significant impact of having a cash reserve during retirement. By strategically tapping into her cash reserves during market downturns, Jane was able to preserve her IRA balance and substantially enhance her long-term financial outcome.

Life Stage Considerations

We tailor our cash management approach to different life stages, recognizing that the cash needs of individuals vary depending on whether they’re in the accumulation phase, distribution phase, or approaching retirement.

Adapting to Market Conditions

Our Investment Committee remains vigilant, adjusting the number of months for one’s Cash Target in retirement to market highs and downturns. This is crucial when clients rely on their investments for retirement income. In bearish markets, we will draw from cash reserves to avoid liquidating assets during unfavorable conditions, whereas in bullish markets, we rebuild cash reserves to the target.

Conclusion

At Gatewood Wealth Solutions, we believe in empowering our clients with robust retirement income planning strategies. By strategically managing cash reserves and investments, we aim to ensure financial stability and long-term prosperity for all our clients. If you’re ready to take control of your retirement finances, we’re here to guide you every step of the way.

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

The Gatewood Team Structure: Personalized Guidance for Every Financial Stage

At Gatewood Wealth Solutions, our philosophy is centered around providing personalized and proactive financial guidance for our clients.

In our experience, as clients’ net worth builds, so does their financial complexity. Given this relationship — and recognizing the importance of navigating various needs based on specific life circumstances — we carefully divide our clients into three groups:

Private Client Care: Ultra-high net worth, ultra-high financial complexity.

Client Care Plus: High net worth, high financial complexity.

Client Care: Average net worth and financial complexity.

Within these segments, we designate specific Client Care Teams to serve a particular number of families, so they can familiarize themselves with typical client needs within those segments. This also helps ensure that no financial plan or investment portfolio is ever reliant on just one person. If something ever happened to one of the advisors — whether retirement, promotion, death, or any other unforeseen circumstance — there would always be another team member familiar with the client’s goals, objectives, and moving pieces to step in and manage their account moving forward.

While some firms take the traditional, one-client-to-one-advisor approach, we set the standard on a true family-to-firm approach. This continuity plan ensures we can deliver on our promises to the families we serve for generations to come.

Client Care Team structure

As a Gatewood client, you receive an on-call Client Care Team tailored to your needs and aligned to your segment. Each member of the team specializes in a particular area related to your account, and all team members work together so that no stone is left unturned when it comes to keeping you on track towards reaching your goals.

While your Wealth Planner is your day-to-day contact, you also have at least three other team members working behind the scenes at all times on your account, not to mention our specialists who can be called in at a moment’s notice to advise as needed.

Wealth Planner: Navigating Your Financial Future

Your Wealth Planner is your family’s personal Certified Financial Planning professional. The CFP® designation demonstrates their proficiency in financial planning, risk management, investment, tax efficiency, retirement, and estate planning advising. They serve as your trusted guide to create and maintain your personalized financial plan that aligns with your goals and aspirations, going beyond simply providing day-to-day services. He or she will be your go-to for most questions!

While the Wealth Planner focuses on your financial strategy, the Wealth Advisor strives to make your client care journey with Gatewood is nothing short of exceptional, especially during times of crucial or complex life decisions. They are dedicated to enhancing your overall experience with the firm, ensuring that every interaction with Gatewood reflects our commitment to excellence.

Your Wealth Planner is supported by a dedicated Wealth Coordinator who takes care of the administrative details of your accounts, from information updates to paperwork. They are the glue that holds the team together, and they work tirelessly to ensure your family has its financial details covered.

Specialists: Providing Experienced Account Support

Our specialists are always ready to provide nuanced knowledge to your family precisely when you need it. Whether you need advice from the Gatewood Investment Committee, a complex strategy from our tax and estate planning specialists, a consultation for employer sponsored retirement plans, or business owner exit planning, we’ll bring in just the right specialist from our team of advisory professionals.

Gatewood Investment Committee: Overseeing and Optimizing your Portfolio

The Gatewood Investment Committee works behind the scenes every day to ensure we’re positioning your investments in a way that helps you pursue your goals. Be sure to tune into our Monthly Market Insights videos to hear their transparent take on the market!

Educational Excellence and Advanced Credentials

At Gatewood, we pride ourselves on the exceptional educational background and advanced credentials of our team members. With a roster that includes MBAs, MAccs, MSFs, MSFSs, JDs, and a suite of distinguished certifications such as CFA®, CFP®, CPA, CEPA®, CMT®, and CAIA®, our professionals bring a depth of knowledge and a breadth of expertise to the table.

In addition to years of experience, this wealth of education and certification translates into a discerning eye for detail and a comprehensive approach to financial strategy. As a client, you benefit from our team’s informed guidance and ability to create sophisticated solutions to meet the complexities of today’s financial landscape.

Gatewood Culture

At Gatewood Wealth Solutions, our culture isn’t just about serving clients; it’s also about nurturing our team members’ growth so they can continue to provide excellent service for years to come. We prioritize a supportive and empowering environment where every individual is encouraged to thrive personally and professionally. This commitment to our team’s well-being fuels their dedication to delivering nothing short of exceptional client experiences, making our culture the driving force behind our success.

Our Commitment to Your Family

Our team structure is designed to ensure that, regardless of life’s changes, you have a consistent, knowledgeable, and dedicated group of professionals ready to support you. As your life evolves, so does our service, adapting to provide the relevant expertise that your situation demands.

If you have any questions about your own Client Care Team structure, please reach out to your Wealth Planner. Not only are we passionate about your success, but we’re also deeply committed to excellence, continually striving to get better, and staying competitive. We will always go the extra mile for our clients and our teammates!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC.

The Essential Shield: Life Insurance in Business Continuity

Christina Shockley, JD, CFP®

Partner & Chief Planning Officer

INTRODUCTION