A decade of doomsday predictions, political hysteria, and the investors who paid the price for listening.

This morning (April 8,2026), futures tied to the Dow surged over 1,000 points. S&P 500 futures jumped nearly 2.7%. Oil prices cratered more than 15%. The catalyst? A two-week ceasefire between the United States and Iran, brokered through Pakistani mediation, appears to be the beginning of the end of a five-week conflict that rattled global markets and sent crude above $115 a barrel.

If you have been reading the headlines over the past month, you would have been convinced this was the beginning of World War III. You would have been told to sell everything. You would have been assured that this time was different.

It was not different. It never is.

What follows is a walk-through of the last decade of panic, the people who stoked it, and the extraordinary cost investors have paid for listening. The through line is not complicated: when politics infects your portfolio, your portfolio suffers. Period.

Meet the Panicans

First, a definition. A Panican is a pundit, strategist, or commentator who consistently predicts catastrophic market outcomes with high confidence, is proven wrong by the subsequent data, and yet never updates their framework. The term is intentional. These are not analysts making reasonable risk assessments. They are performers whose panic is the product.

Before we walk through the timeline, let me introduce you to a cast of characters. Some are economists. Some are market strategists. Some are media personalities. What they all have in common is a pattern: confident, loud predictions of doom that turned out to be spectacularly wrong at exactly the moments when investors should have been getting more aggressive, not less.

These are not bad people. Most of them are genuinely smart. But intelligence without discipline is a liability, and when political bias or structural bearishness infects your worldview, it turns your analysis into a contrarian buy signal for the rest of us.

The Econ and Political Pundits

PAUL KRUGMAN — Nobel Prize-winning economist, New York Times columnist

“If the question is when markets will recover, a first-pass answer is never. We are very probably looking at a global recession, with no end in sight.”

Said on election night 2016. The Dow hit an all-time high 9 hours later. He later admitted he “reacted badly.” The Atlantic diagnosed him with “Trump Derangement Syndrome.”

STEVE LIESMAN — CNBC Senior Economics Reporter

“What President Trump is doing is insane. It is absolutely insane. There is just no other way of describing it.”

Said on air in March 2025 about tariffs. By December 2025, inflation had moderated to 2.7% and the S&P 500 posted its third consecutive year of double-digit gains. He was visibly stunned on live television by the positive CPI data.

TOM WOODS — Libertarian economist and commentator

Persistent warnings about government spending, deficits, and inevitable economic collapse.

Has been forecasting imminent fiscal catastrophe for years while the S&P 500 has roughly quadrupled from its 2016 levels. The deficit hawks have been right about the deficits and wrong about the market consequences for an entire generation.

The Market Strategists

MARKO KOLANOVIC — Former Chief Market Strategist, JPMorgan Chase

“We do not see equities as attractive investments at the moment, and we don’t see a reason to change our stance.” S&P 500 target: 4,200.

Maintained this bearish call through 2023 and 2024 while the S&P 500 rallied over 40%. Was bullish through the 2022 bear market, then flipped bearish right at the October 2022 bottom. JPMorgan showed him the door in July 2024. CNBC had once called him “half-man, half-god.” Bloomberg called him “Gandalf.” The market called him wrong.

BOB ELLIOTT — CEO, Unlimited Funds (Bridgewater alum)

Repeatedly warned that stock market optimism was “getting ahead of economic realities” and cautioned that conditions resembled 1970s-style stagflation.

Throughout 2023 and 2024, while Elliott cautioned the economy would slow and markets were overpriced, the S&P 500 posted back-to-back gains of 24% and 23%. The recession he warned about never materialized.

MIKE GREEN — Chief Strategist, Simplify Asset Management

“We’re possibly setting ourselves up for the worst financial experience of all time” due to passive investing flows.

Green’s thesis that passive investing has created catastrophic structural fragility has been a consistent theme for years. Meanwhile, the very passive index funds he warns about have delivered one of the greatest stretches of returns in market history. Three consecutive years of double-digit S&P 500 returns.

LUKE GROMEN — Founder, Forest for the Trees (FFTT)

“Recession is inevitable.” Called for dollar collapse, sovereign debt crisis, and Treasury market dysfunction as imminent risks.

Predicted recession was inevitable in 2023. It never came. Warned of dollar collapse. The dollar remained resilient. Forecast Treasury dysfunction as near-term certainty. None materialized on his timeline. His macro framework is intellectually fascinating and may eventually prove correct, but following it as a trading signal has cost his audience years of compounding returns.

SCOTT GALLOWAY — NYU Professor, host of Pivot and Prof G podcasts

“I think we’re on the precipice of like a $10 trillion dollar wipeout.” Warned that the Iran war would trigger an ’08-style “which bank is next?” moment through emerging market sovereign defaults.

Said on Pivot podcast in March 2026, weeks before the ceasefire. The S&P 500 never even reached a 10% correction. No emerging market sovereign defaults materialized. Oil is already down 15% this morning. The $10 trillion wipeout did not happen.

Here is the critical point about these individuals: they are not dumb. Several of them are brilliant. But brilliance without humility, without the ability to say “I was wrong and the market is right,” becomes a trap. And that trap has cost their followers dearly.

Now, let us walk through the episodes where their warnings were loudest and where the buying opportunities were greatest.

NOVEMBER 2016

The Election That Would End the World

The night Donald Trump won the presidency, S&P 500 futures plummeted nearly 5%. Dow futures crashed 800 points. The financial media declared it a catastrophe in real time.

Krugman published his “markets will never recover” take before most Americans had gone to bed. Larry Summers projected “a protracted recession to begin within 18 months.” Steve Rattner promised “a market crash of historic proportions.” Eric Zitzewitz, formerly of the IMF, predicted “a likely crash in the broader market.”

What actually happened? The Dow soared 257 points the very next day, brushing against all-time highs. That “never” recovery took roughly nine hours. Over the following year, the Dow climbed approximately 35%, adding some $6 trillion in household wealth.

+35%

DOW JONES RETURN IN THE YEAR FOLLOWING THE 2016 ELECTION

Q4 2018

The First Trade War

By the fall of 2018, the U.S.-China trade conflict dominated headlines. Tariff escalation, a hawkish Federal Reserve, and a brief yield-curve inversion sent markets into a tailspin. The S&P 500 fell 13.5% in the fourth quarter, posting its worst December since 1931. The index nearly entered bear market territory, dropping 19.4% from its September peak to its Christmas Eve trough.

The bears were everywhere. The recession callers were triumphant. The “Trump’s trade war will destroy the economy” narrative was treated as established fact. This was the first major test of a pattern we would see repeated again and again: escalation, panic, resolution, violent repricing higher.

Then the calendar turned. In 2019, the S&P 500 returned 31.5%, its best year since 2013. Investors who added to their positions during that gut-wrenching December were rewarded handsomely. Those who sold near the lows spent the next year watching from the sidelines.

+31.5%

S&P 500 RETURN IN 2019, FOLLOWING THE Q4 2018 PANIC

MARCH 2020

COVID: The Fastest Bear Market in History

On February 19, 2020, the S&P 500 closed at an all-time high. Thirty-three days later, it had fallen 34%. Circuit breakers tripped multiple times. On March 16, the index dropped nearly 12%, the worst day since 1987. The panicans were in full throat. The world was ending. The economy would never recover.

On March 18, 2020, with the S&P 500 already down over 25% and still falling, our CEO Aaron Tuttle hosted a market update call with clients. While the financial media was running wall-to-wall panic and most strategists were calling for further downside, Aaron drew on a historical precedent that almost no one was talking about.

“When the Spanish flu subsided in February 1919, the market began an increase of 50%. It does provide encouragement that once the coronavirus begins to subside, the market will bounce back once again.”

— AARON TUTTLE, CEO, GATEWOOD WEALTH SOLUTIONS, MARCH 18, 2020

Aaron did not stop at the historical comparison. He made a specific call about the shape and speed of the recovery that, in the moment, sounded almost reckless in its optimism.

“Every indication is that once this passes it could be very, very quick and we’ve seen it right… it’s just as quick on the upside.”

— AARON TUTTLE, CEO, GATEWOOD WEALTH SOLUTIONS, MARCH 18, 2020

He pointed to the massive fiscal and monetary stimulus that was already being deployed, noting that “if you have that much fuel, it’s going to come back much, much faster.” And he predicted that “confidence should quickly rebound once the event passes simply due to the relief.”

That call was made five days before the S&P 500 hit its absolute low on March 23. The V-shaped recovery Aaron described is exactly what happened. The index doubled from its lows in 354 trading days, the fastest bull market doubling since World War II.

Here is what is remarkable about the contrast. While Aaron was telling clients to stay the course and prepare for a rapid snapback, the panican class was doing the opposite. Kolanovic, to his credit, made a similar bullish call in late March 2020, predicting the S&P 500 would quickly recover to all-time highs. It was bold, contrarian, and correct. But the tragedy of Kolanovic’s story is what came next. Having earned enormous credibility, he proceeded to stay bullish through the entire 2022 bear market, then turned bearish at the exact bottom in October 2022, and remained bearish through a 40%+ rally. He turned one spectacular correct call into two years of wrong calls that ended his career at JP Morgan.

Aaron, by contrast, has maintained the same disciplined framework across every crisis on this list. Market corrections and bear markets are normal. Selloffs end. Stay invested. The consistency of that message, delivered calmly during the worst moments, is what separates an advisor from a pundit.

For the rest of us, the lesson from COVID was clear: the investors who sold at the bottom missed one of the greatest buying opportunities of a generation. The four-year annualized return from that March 23, 2020 bottom? Approximately 25.7%.

+150%

S&P 500 TOTAL RETURN IN THE 4 YEARS FOLLOWING THE COVID LOW

LATE 2021 – 2022

Inflation Was Not Transitory

To be fair, there was one moment where the establishment consensus was dangerously wrong in the other direction. Throughout 2021, the Federal Reserve insisted that surging inflation was “transitory.” It was not.

Consumer prices hit 40-year highs. The Fed was forced into the most aggressive rate-hiking cycle in a generation. The S&P 500 fell 25% from its January 2022 peak to its October trough. The Nasdaq plunged 33%.

This is where the structural bears had their moment. Gromen’s fiscal concerns were manifesting in real-world inflation. Credit where credit is due.

But being right about the diagnosis does not mean you were right about the prescription. The bears told you to sell. They told you recession was “inevitable.” Eighty percent of economists predicted a 2023 recession. It never came. The S&P 500 rallied off its October 2022 lows and posted double-digit gains in 2023, 2024, and 2025. Three consecutive years.

Being right about the problem does not make you right about the solution. The bears correctly identified inflation. They were dead wrong about what it meant for equity investors who stayed the course.

APRIL 2025

Liberation Day and the Tariff Tantrum

On April 2, 2025, President Trump announced sweeping “reciprocal” tariffs that exceeded even the most bearish expectations. In four days, the S&P 500 shed more than 12%. The Dow lost nearly 4,600 points.

Liesman went on CNBC and called the tariff policy “insane,” comparing it to “steering the Titanic towards the iceberg.” UBS warned of a “meaningful recession.” The panicans were vindicated. For about a week.

Seven days later, Trump announced a 90-day pause. The S&P 500 surged 9.5% in a single session. By May 13, the index was positive for the year. By June 27, 2025, it hit a new all-time high. By December 2025, inflation had moderated to 2.7% and Liesman was visibly stunned on live television by how good the data looked.

This is where the pattern becomes undeniable. And this is where our Chief Investment Officer, Chris Arends, published an internal framework that we believe every investor should understand.

In March 2026, our CIO Chris Arends distributed an internal briefing we titled “The Trump Conflict Playbook.” The thesis is straightforward: since Trump’s 1st term, every major geopolitical and trade conflict has followed a repeating 10-step cycle from escalation to resolution. Every single one has ended with a deal.

The cycle moves through three phases. First, a Pressure Phase where posturing and escalation build credibility. Second, a Volatility Phase where markets price in a prolonged conflict and defensive positioning reaches an extreme. Third, a Resolution Phase where de-escalation signals emerge, a deal is struck, and markets reprice violently higher.

The key insight: the repricing is abrupt, not gradual, because by the time a deal becomes credible, investors are already defensively positioned. When uncertainty collapses, those positions unwind all at once. This pattern played out in the April 2025 tariff pause, the August 2025 extension, the October 2025 China deal, the January 2026 Greenland/EU deal, the February 2026 India deal, and now the Iran ceasefire.

The playbook’s conclusion, written five weeks before today’s ceasefire: “Trump does NOT want a forever war. His top three policy priorities are all directly undermined by a prolonged conflict. Investors currently defensively positioned should expect that unwind to be swift.”

+16%

S&P 500 RETURN IN THE YEAR SINCE “LIBERATION DAY” (APRIL 2025)

APRIL 2026

The Iran Conflict: Today’s Resolution

On February 28, 2026, the United States and Israel launched airstrikes on Iran. The conflict closed the Strait of Hormuz, sent oil surging nearly 70%, pushed gasoline above $4 a gallon, and knocked the S&P 500 down nearly 10% from its highs.

The Conflict Playbook called it in real time. In early March, with markets deep in the Volatility Phase (Step 6), the framework identified that Brent crude crossing $85, the Dow falling over 1,100 points, and markets pricing in prolonged conflict risk were the exact conditions that historically precede de-escalation. The playbook noted key thresholds: Brent above $90, equities down 5%+, and gas prices up 10%+ as triggers that would substantially raise the probability of negotiation headlines.

“We’re on week three. I know it sounds a little crazy to think this could be done in 2 to 3 weeks, but that has really become our base case that it’s not a prolonged conflict. He wants to make you think it is because that’s his steps before de-escalation.”

— Chris Arends, MARCH 20th, 2026

Our team’s conviction was rooted in a simple observation: a prolonged war accomplished none of Trump’s stated objectives. As we noted at the time, “I think Trump signaled he wants this conflict to be done before he goes to China and has that summit.” The escalation was not the strategy. The escalation was the leverage. The strategy was always the deal.

Every threshold was breached. And exactly as the framework predicted, the resolution followed. A ceasefire brokered through Pakistan, a commitment to reopen the Strait of Hormuz, and peace talks scheduled for Friday in Islamabad.

As of this morning, S&P 500 futures surged 2.7%. Dow futures jumped over 1,000 points. Oil cratered more than 15%. The S&P 500 sits at roughly 6,600, just 5.5% below its all-time high. The conflict’s maximum drawdown never even reached the technical definition of a correction.

Step 10 of the playbook: “The violent repricing and political victory lap.” That is today.

The Panicans as Contrarian Indicators

Here is the uncomfortable truth that nobody on financial television will say out loud: the loudest voices during market panics are almost always the best contrarian buy signals available.

When Krugman says markets will “never” recover, buy. When Kolanovic’s bearish target is the lowest on Wall Street, buy. When Liesman calls policy “insane” on live television, buy. When Gromen says recession is “inevitable,” buy. When Green warns of “the worst financial experience of all time,” buy. When 80% of economists predict a recession, buy.

This is not a joke. This is a decade of data. Every single major bottom on this list was accompanied by maximum bearish consensus from the panican class. And every single one was followed by substantial gains for investors who had the discipline to act against the prevailing narrative.

Kolanovic’s story is perhaps the most instructive. He was once the most respected strategist on Wall Street. He made one of the great calls of the COVID era. And then his bearish bias consumed him. He maintained a 4,200 S&P target while the index screamed past 5,500. JPMorgan let him go in July 2024. The S&P 500 has gained roughly 40% since the October 2022 bottom he told everyone to sell.

The loudest voices during market panics are almost always the best contrarian buy signals available. This is not an opinion. This is a decade of data.

Trump Derangement Syndrome Destroys Portfolios

There is a pattern in every single one of these episodes, and it goes beyond simple fear. It is politically motivated fear. It is what happens when a person’s deep-seated political bias distorts their ability to think clearly about markets, economics, and risk.

When someone suffers from Trump Derangement Syndrome, their analytical framework collapses. They cannot see the economy for what it is because they are too busy seeing it through the lens of what they desperately want it to be. They want the other side to fail. They want the market to punish the country for making what they consider the wrong electoral choice. And that desire, whether conscious or not, infects every financial decision they make.

Look at the evidence. Krugman predicted a “global recession with no end in sight” not because his models told him so, but because he was horrified by the election result. The Atlantic later diagnosed Krugman specifically with Trump Derangement Syndrome by name. He himself admitted he “reacted badly.”

Liesman, separately, called tariff policy “insane” on live television not because the data supported that conclusion, but because his political priors told him protectionism could not possibly work. When the inflation data came in better than expected months later, he was visibly shocked on his own broadcast.

Tom Woods, for all his economic sophistication, has been so consumed by his ideological opposition to government intervention that he has missed one of the greatest wealth-creation periods in American history. His audience has been told for years that the fiscal house of cards is about to collapse. It has not. And every year they stayed underweight equities on that thesis, they fell further behind.

On the market strategist side, the pattern is slightly different but equally costly. Kolanovic, Elliott, Green, and Gromen are not motivated by partisan politics in the same way. Their bias is structural. They see systemic risks, passive flow distortions, fiscal unsustainability, and market fragility. And they are not entirely wrong about any of those things. But the gap between “these are real risks” and “sell your stocks now” is where fortunes are made and lost. Being aware of structural risk is wisdom. Letting structural risk prevent you from participating in a generational bull market is tragedy.

The panicans are often directionally correct. Deficits are unsustainable. Passive flows do distort price discovery. Valuations do get stretched. Geopolitical risk is real. But direction without timing is not an investment thesis. It is a worry. And worries do not compound. Equities do.

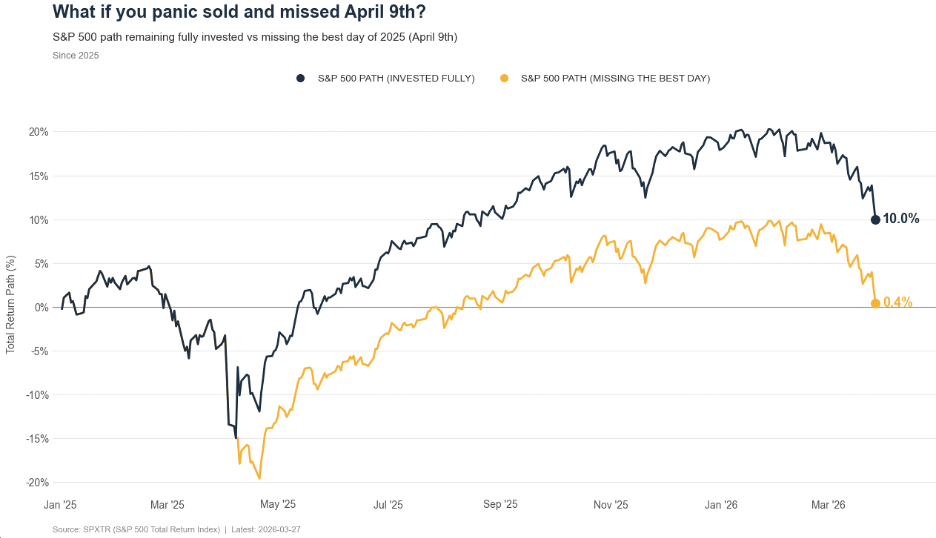

The chart above from Ritholtz tells the story as well as any paragraph can. Missing just the single best day of 2025, April 9th, the day Trump announced the tariff pause, turned a 10% annual return into a 0.4% return. One day. The difference between a strong year and a lost year. That is the cost of panicking. That is the tax the panicans impose on their followers.

If you take one thing from this piece, let it be this: your political opinions and your investment strategy must live in separate rooms. The moment you allow your feelings about a president, a party, or a policy to dictate your financial decisions, you have given control of your wealth to the least rational part of your brain.

The market does not care who you voted for. It does not care how you feel about the person in the Oval Office. It cares about earnings, cash flows, innovation, and the long-term trajectory of the most dynamic economy the world has ever produced.

Stay invested. Stay disciplined. Stay rational. And when the panicans start screaming again, and they will, remember: that is your signal to get more aggressive, not less.

Sometimes the hardest part isn’t what the market is doing—it’s knowing how to respond in the moment. Having the right perspective can make all the difference. If this raises questions or you’d like to go deeper, feel free to schedule a conversation with us below.

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

The fast price swings in commodities will result in significant volatility in an investor’s holdings. Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors. Indexes are unmanaged and cannot be invested in directly.

The NASDAQ Composite Index measures all NASDAQ domestic and non-U.S. based common stocks listed on The NASDAQ Stock Market. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the Index.