Much has changed since then. Tax filing season opened on January 26th, more than three million families have now signed up, a Super Bowl ad ran during the pregame broadcast, President Trump promoted the accounts during his State of the Union address on February 24th and directed the nation to trumpaccounts.gov, and a new online sign-up option just launched.

Here’s our refreshed take on what this program means for your family.

The Basics: What Are Trump Accounts?

Trump Accounts, formally known as 530A Accounts under the One Big Beautiful Bill Act, are a new type of individual retirement account designed specifically for children. They’re custodial in nature, meaning a parent or guardian controls the account until the child turns 18.

How the Trump Accounts Actually Work

Eligibility: Any U.S. citizen under age 18 with a valid Social Security number can have an account opened on their behalf. Each child may have only one Trump Account.

Account Benefits

The $1,000 Seed: Children born between January 1, 2025 and December 31, 2028 who are U.S. citizens are eligible for a one-time $1,000 pilot program contribution from the U.S. Treasury. This deposit is expected no earlier than July 4, 2026.

Annual Contributions: Families, employers, and others may contribute up to a combined $5,000 per child per year. Employers may contribute up to $2,500 (per employee) of that amount under Section 128 as a fringe benefit. The $5,000 limit will be adjusted for inflation starting in 2027. No earned income is required, and contributions don’t affect traditional or Roth IRA limits for the contributor.

Account Limitations

Charitable & Government Contributions: Qualified general contributions from government entities and 501(c)(3) organizations do not count against the $5,000 annual limit. These are separate and additive.

Investment Rules: All funds must be invested in low-cost, broad U.S. equity index funds or ETFs tracking qualified indexes such as the S&P 500. Annual fees are capped at 0.10% (10 basis points), and no leverage is permitted.

No Withdrawals Before 18: Generally, no distributions may be made before the year the child turns 18, with very limited exceptions for death, excess contributions, and certain rollovers.

What’s New About Trump Accounts Since December

1. Tax Season Sign-Ups Are Live

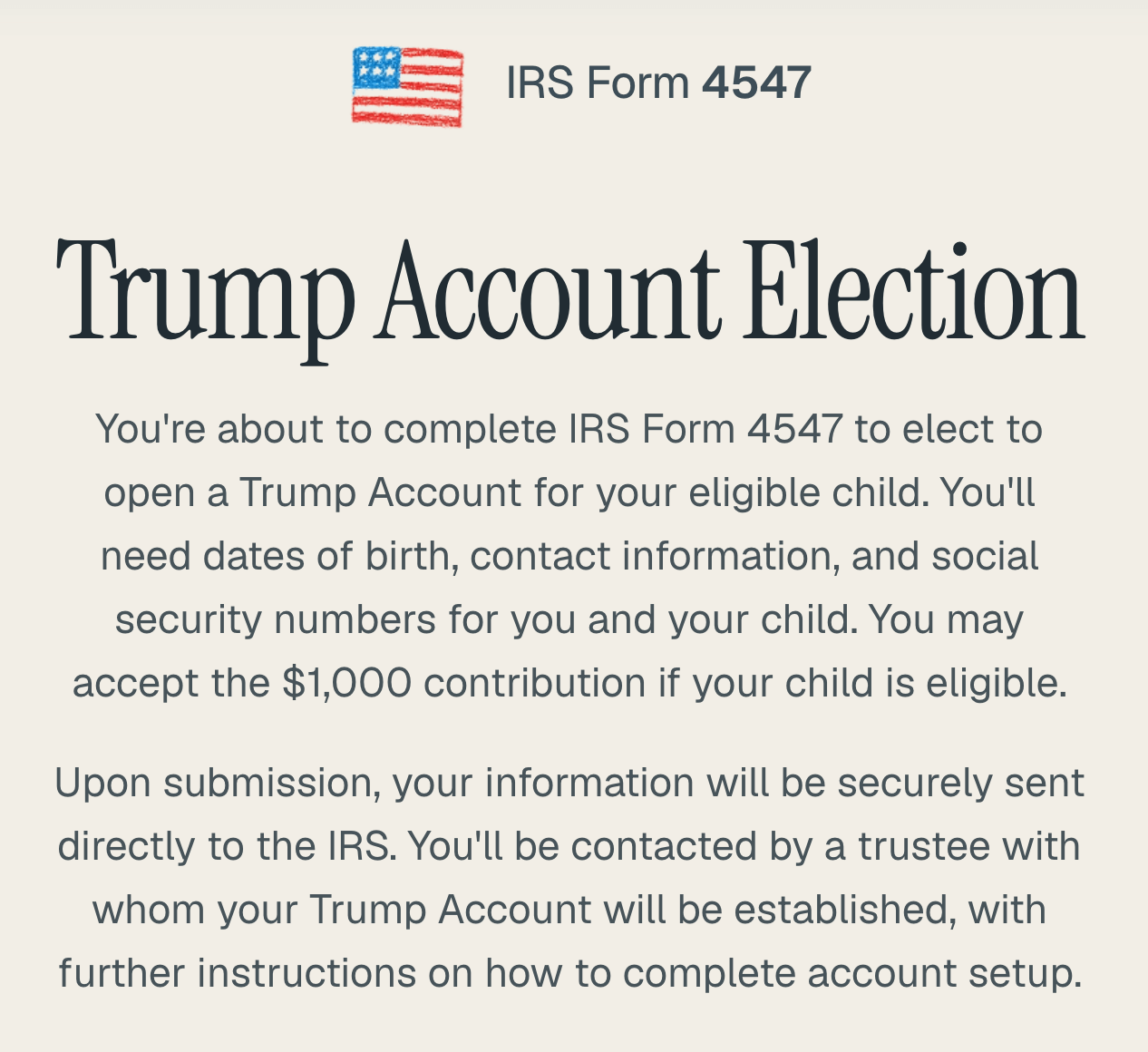

As of January 27, 2026, families can elect to open Trump Accounts by filing IRS Form 4547 with their 2025 federal tax return. The form includes two elections: one to open the account and one to request the $1,000 pilot program contribution (if eligible).

The form accommodates up to two children and families with more eligible children can attach additional copies. Filing electronically with your tax return is the fastest and easiest method.

2. New Online Sign-Up Option

Following the Invest America Super Bowl ad last weekend, a new online sign-up form launched at trumpaccounts.gov, ahead of the originally planned mid-2026 timeline. This gives families a second pathway to open accounts outside of the tax filing process. Here’s what the sign-up experience looks like:

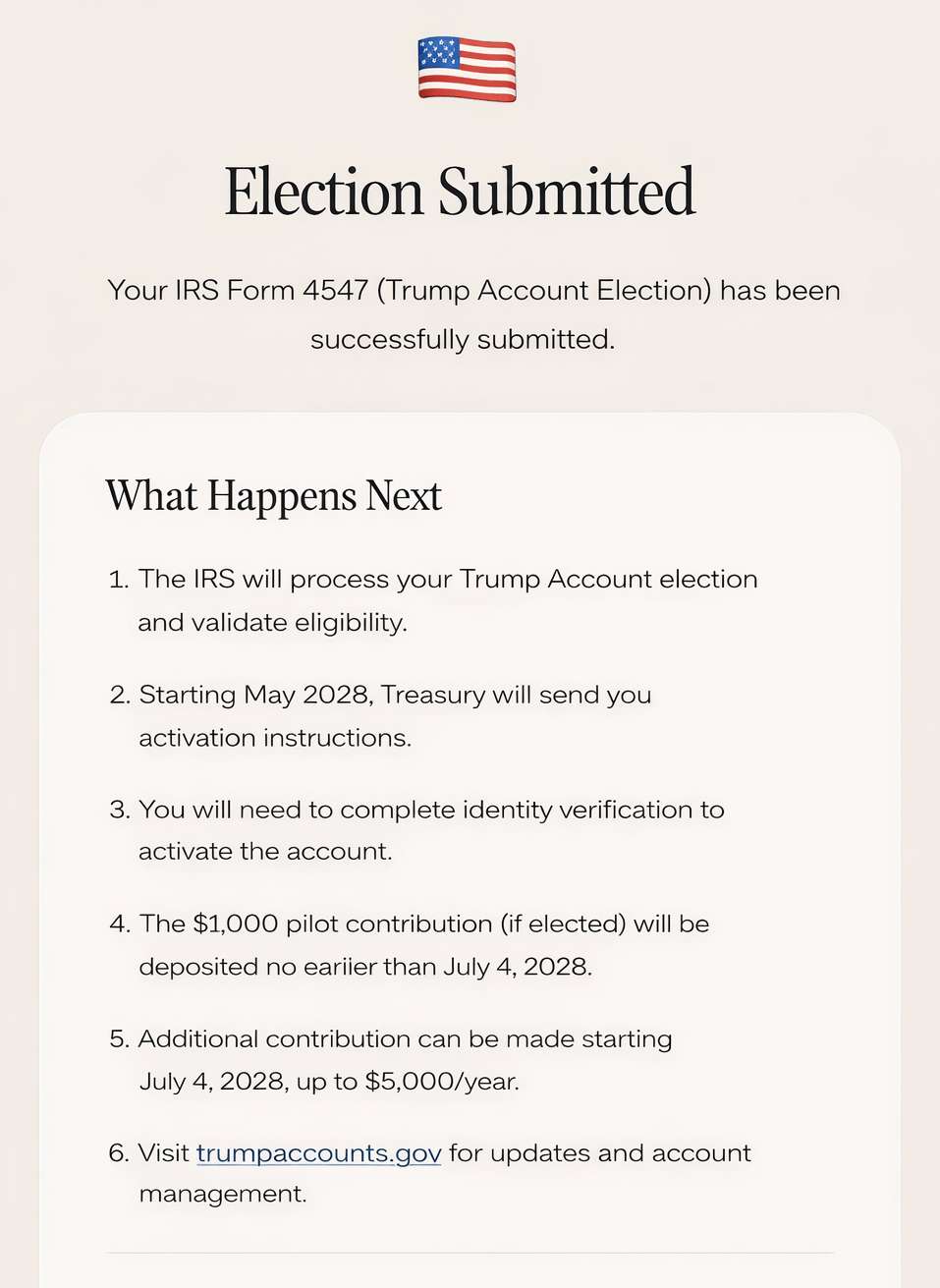

The Form 4547 election page at trumpaccounts.govConfirmation and next steps after submission

3. Over Three Million Families Have Enrolled

According to the White House, more than three million families had signed up as of the State of the Union address on February 24th. That milestone was up from one million just five days into tax filing season, and Treasury Secretary Scott Bessent noted that approximately 500,000 elections were made in the first three days alone. During the speech, President Trump called the program “something that’s so special” that has “taken off and gone through the roof,” and directed the nation to sign up at trumpaccounts.gov.

4. Activation Timeline

After filing Form 4547, the Treasury Department will contact parents starting in May 2026 to complete an identity verification process and activate accounts. You’ll be contacted by the partner financial firm where your Trump Account will be held with further instructions. Contributions and seed deposits will begin on July 4, 2026.

5. The Dell Foundation Gift

Michael and Susan Dell have pledged $6.25 billion to seed accounts for approximately 25 million children who missed the eligibility cutoff for the $1,000 federal deposit. Their gift provides $250 per eligible child. To qualify for the Dell contribution, children must be age 10 or under, born before January 1, 2025, and live in ZIP codes where the median household income is below $150,000. This is expected to reach children across roughly 75% of U.S. ZIP codes.

An important clarification: The Dell gift goes to a different population than the Treasury’s $1,000. It is not $250 on top of $1,000. Children born 2025 through 2028 receive the $1,000 government seed. Children born before 2025 who are age 10 and under may receive the $250 Dell contribution. Both groups benefit, but through separate funding streams.

6. Growing Employer and Corporate Support

A growing list of major U.S. corporations have pledged matching deposits or contributions for employees. Venture capitalist Brad Gerstner has also pledged $250 for each child under five with a Trump Account in Indiana. We expect this trend of employer and philanthropic participation to continue expanding.

How the Tax Treatment Works

Understanding the tax treatment matters because it affects whether you should add your own money to these accounts or use other vehicles instead.

Think of it in two phases:

PHASE 1: Before Age 18 (The Accumulation Phase)

During childhood, contributions are made with after-tax dollars, and investment growth accumulates tax-deferred. Parents or guardians maintain control of the account during this period. This phase is straightforward.

PHASE 2: After Age 18 (The IRA Conversion Phase)

At age 18, Trump Accounts automatically convert to traditional IRAs. This conversion fundamentally changes how the account functions:

What Changes on Trump Accounts for Those Over 18?

Access and Control: The young adult gains full control as the account becomes a traditional IRA in their name.

Withdrawals and Taxes: This is where it gets important. Distributions are taxed as ordinary income on all earnings and growth (though your original contributions come back tax-free). Additionally, the 10% early withdrawal penalty applies to distributions before age 59½.

The Exception Rules:

The 10% penalty (not the taxes) can be waived for:

First-time home purchases (up to $10,000)

Qualified education expenses

Business startup costs in certain circumstances

Here’s the crucial point many families miss: These “qualified expenses” only waive the 10% penalty—they do NOT eliminate the ordinary income tax on the earnings. Even when funding college or buying a first home, you’ll owe income tax on all the growth.

Investment Flexibility: After conversion, the account can be invested more broadly according to traditional IRA rules, no longer restricted to designated index funds.

Why This Matters: This automatic conversion to a traditional IRA means families should carefully consider whether contributing their own funds makes sense compared to other savings vehicles like 529 plans (where qualified education withdrawals are completely tax-free) or custodial accounts (where flexibility is greater).

Our General Perspective on Trump Accounts

Accept the free money. If your child qualifies for the $1,000 Treasury seed or the $250 Dell contribution, opening an account is straightforward. You’re accepting a gift with no cost to you. We’d help every eligible family capture this benefit. The Treasury projects that the $1,000 seed alone could grow to roughly $6,000 by age 18, $15,000 by age 27, or over $243,000 by age 55, assuming historical market returns.

Think carefully about your own contributions. For most families whose primary goal is funding education, 529 plans still deliver better tax outcomes. A 529 offers completely tax-free growth potential and withdrawals for qualified education expenses. Trump Accounts tax all growth as ordinary income at withdrawal, even for education. That’s a meaningful difference.

When Trump Accounts Make Sense for Your Plan

That said, Trump Accounts can make sense when:

You’re already maximizing 529 contributions and want additional tax-advantaged savings

Your priority is very long-term wealth building, with retirement savings starting at birth

You’re targeting a first home down payment for your child

Your employer is offering matching contributions, which is additional free money worth capturing

You want to diversify across savings vehicles with different tax treatments

Check with your employer. A growing number of companies are pledging contributions to Trump Accounts as an employee benefit. If your employer is participating, that’s money you don’t want to leave on the table, similar to a 401(k) match.

Action Steps for Families

File Form 4547 with your 2025 tax return. This is the fastest way to open an account and elect the $1,000 pilot program contribution for eligible children. You can also sign up online at trumpaccounts.gov now.

Check your employer’s plans. Ask your HR or benefits team whether your company is making Trump Account contributions under Section 128.

Don’t rush your own contributions. Contributions won’t be accepted until July 4. Use this time to evaluate whether a Trump Account, 529 plan, or combination makes the most sense for your family’s goals.

Keep records. Documentation of contribution sources matters for future distribution taxes and rollover reporting. Start organized from day one.

How Gatewood Can Help You Analyze Trump Accounts

This program launches on July 4, which gives us time to plan strategically together. The questions we help families answer are straightforward but important:

Does your family qualify for the maximum benefits?

Should you contribute your own funds, or does a 529 or custodial account better serve your goals?

And how does this fit into your broader wealth-building strategy?

We specialize in exactly these conversations, the kind where “it depends” actually becomes “here’s exactly what makes sense for you.” We’re fiduciary advisors, so this isn’t about selling you on Trump Accounts. It’s about helping you make the most informed choice for your family’s specific circumstances.

Ready to discuss strategy?

Important Considerations

This program is new, and IRS regulations continue to evolve. The information provided here reflects program details as understood in December 2025, but specific rules and procedures may change as implementation progresses. Investment returns are not guaranteed, and tax laws may change. This material is educational and not a recommendation for any specific action.

For personalized guidance on whether Trump Accounts make sense for your family, we encourage you to consult with a financial advisor and tax professional who can evaluate your complete financial picture.

Important Disclosures

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. Gatewood Wealth Solutions and LPL Financial do not provide legal or tax advice or services.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Prior to investing in a 529 Plan investors should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

"A friend of a friend referred us to the team over 20 years ago, and we've been together ever since. My wife and I have changed jobs and time zones more than once, but they've been a constant through it all. Even when moving to different parts of the country, we always keep our ties to St. Louis wherever possible, and we appreciate the Midwestern values of Gatewood. The relationship we’ve developed over the years has built trust in the team that they are honest and always have our best interests in mind. They’ve helped us with everything from moving…"

"My husband and I began working with Brian in 2019 and have been very pleased with the level of service we’ve received ever since. Our client care team, Nina and Jake, have taken the time to truly listen to our goals and actively make adjustments to reflect our evolving needs over time. What I appreciate most is the combination of knowledgeable, focused guidance always delivered with genuine care and humility. We've been so impressed with their timeliness and attention that we've introduced them to our parents, siblings and adult children and now they are advising three generations of our family.…"

"As a client of Gatewood for over 10 years now, I am very pleased with the experience I’ve had with my team. Whenever I have questions or need advice, they are always available with professional and helpful guidance. They really get to know their customers so that they can provide personalized service and are very responsive when I contact them and they do a great job managing my portfolio. I had a turning point in my life, and they were very helpful in analyzing financial impacts and helping to manage through it. I highly recommend their services."

"What has stood out most over our decade-long relationship with Gatewood is how genuinely they listen. Our advisor takes the time to understand our full financial picture and has made a point to build a relationship with my wife as well, so she feels comfortable working with the team whether I'm present or not. Having everything coordinated in one place, with great online tools at our disposal, has been invaluable. Our team is responsive whenever we have questions and has always followed through with care and professionalism. Beyond the planning itself, it's the personal relationships we've developed that make this…"

"Our relationship with Gatewood Wealth Solutions has evolved over the years right along with our family. From building and protecting our wealth to retirement and estate planning, Gatewood has guided us and enabled our objectives. It’s assuring to know skilled professionals we trust are working with us to optimize what we have worked for all our lives."

"My wife and I have had the benefit of working with John Gatewood for over thirty-five years. Initially, John worked with us planning our personal and business life insurance needs. As his service offerings expanded, we took advantage of his expertise to help us with our family's financial planning. We could not be more pleased than what we are with the plan the Gatewood Wealth Solutions team developed for us. The team members are well-trained, intelligent, friendly, enthusiastic, and very good listeners. We have two scheduled reviews of the plan every year with one of the principals and at least…"

"Partnering with Gatewood Wealth Solutions has been one of the best decisions we have made in the last five years. I have met with numerous financial planners who’ve all come to me with similar ideas and recommendations that don’t seem to prove that they are thinking outside the box for me individually. But when Gatewood came to me with their plan it was strategically designed with so many aspects taken into consideration that I was surprised at how uniquely competent and professional they were. They brought me many ideas and recommendations that would not bring them profit. They brought me…"

"I have known John Gatewood, the founder of Gatewood Wealth Solutions, for many years. We became friends well before we talked about business, and it was a natural decision to turn to John for help with our affairs when I needed it because I had grown to know and trust him. It really is true that John and his team at Gatewood Wealth Solutions are completely focused on helping ordinary families like ours to become financially independent. The family part especially means something: One day my 20-something son called to ask if I thought our group would be willing to…"

"Gatewood Wealth Solutions gives me confidence that my retirement savings are being monitored and managed with MY best interest in mind. All of the staff is welcoming, friendly and respectful. They have comprehensive knowledge of long-term financial planning, estate planning and tax planning. I have been with Gatewood for many years and hope to be with them for many more years to come."

"I have been with Gatewood Wealth Solution for seven years, and I would highly recommend them for wealth management services. They are a very efficient, effective, knowledgeable team that provides highly personalized, client-centered services. If I didn't know better, I would think that I am their only client! They have an excellent working relationship with a highly respected law firm that provides assistance with trusts and estate planning. They also have an excellent working relationship with a tax accounting firm. All of this so that all aspects of my financial planning needs are seamlessly coordinated. Their quarterly meetings are well…"

"I’ve been with Gatewood Wealth Solutions and its predecessor for 21 years as our financial advisors. I first met John Gatewood in 2002 when I purchased a life insurance policy from him when he was with Northwestern Mutual. Shortly after having additional discussions with John, we started using them as our only financial advisors. They continued over the years to more than perform above my expectations and also started to bring in additional talent within their organization in order expand and meet client’s expectations. Since they’ve organized as Gatewood Wealth Solution and separated from Northwestern Mutual, they’ve continued to add…"

"I have worked with Gatewood Wealth Solutions since its inception and could not speak more highly of my experience. Gatewood Wealth Solutions provides comprehensive wealth management services for my family in a very sophisticated way. Their planning services are comprehensive and consider all assets of our family, not just what they manage. This is important for our family since we have a real estate business which must be considered in our planning. They also help us with our estate and tax planning each year. Their service is exceptional and is proactive and not reactive. I have referred members of my…"

"Navigating the complexities of my corporate life was already a challenge, but when my husband passed away, it felt like an insurmountable mountain of emotions and paperwork. The team at Gatewood Wealth Solutions stepped in with compassion, efficiency, and expertise, guiding me through the entire estate settlement process. Their unwavering support made a world of difference during such a challenging time. I am profoundly grateful for all they've done and continue to do for me. Their services are truly unparalleled, and I wholeheartedly trust and recommend them."

"My wife and I became a client of Gatewood Wealth Solutions twelve years ago on the recommendation of a friend who was also a Gatewood client, and I am very glad that we did. Until that time, I had managed our 401(k) and investments, but with retirement on the horizon, we felt it important to get professional help for retirement planning and investment management. The Gatewood team developed an integrated financial and retirement plan that we refined together. It was based on information such as our current financial position, desired retirement date and lifestyle, anticipated job and retirement income, expenses,…"

"My wife and I have known and worked with John Gatewood and his team for nearly a decade. The values-driven team of Gatewood Wealth Solutions is motivated, caring, highly competent and personally fueled by character and integrity. I recommended Gatewood to friends and family - including my children - because their deep desire to help clients 'give purpose to their wealth' gives us all the opportunity to better serve our families and communities."

The statements provided are testimonials by clients of the financial professional. The clients listed have not been paid or received any other compensation for making these statements. As a result, the client does not receive any material incentives or benefits for providing the testimonial. These views may not be representative of the views of other clients and are not indicative of future performance or success.