A decade of doomsday predictions, political hysteria, and the investors who paid the price for listening.

This morning (April 8,2026), futures tied to the Dow surged over 1,000 points. S&P 500 futures jumped nearly 2.7%. Oil prices cratered more than 15%. The catalyst? A two-week ceasefire between the United States and Iran, brokered through Pakistani mediation, appears to be the beginning of the end of a five-week conflict that rattled global markets and sent crude above $115 a barrel.

If you have been reading the headlines over the past month, you would have been convinced this was the beginning of World War III. You would have been told to sell everything. You would have been assured that this time was different.

It was not different. It never is.

What follows is a walk-through of the last decade of panic, the people who stoked it, and the extraordinary cost investors have paid for listening. The through line is not complicated: when politics infects your portfolio, your portfolio suffers. Period.

Meet the Panicans

First, a definition. A Panican is a pundit, strategist, or commentator who consistently predicts catastrophic market outcomes with high confidence, is proven wrong by the subsequent data, and yet never updates their framework. The term is intentional. These are not analysts making reasonable risk assessments. They are performers whose panic is the product.

Before we walk through the timeline, let me introduce you to a cast of characters. Some are economists. Some are market strategists. Some are media personalities. What they all have in common is a pattern: confident, loud predictions of doom that turned out to be spectacularly wrong at exactly the moments when investors should have been getting more aggressive, not less.

These are not bad people. Most of them are genuinely smart. But intelligence without discipline is a liability, and when political bias or structural bearishness infects your worldview, it turns your analysis into a contrarian buy signal for the rest of us.

The Econ and Political Pundits

PAUL KRUGMAN — Nobel Prize-winning economist, New York Times columnist

“If the question is when markets will recover, a first-pass answer is never. We are very probably looking at a global recession, with no end in sight.”

Said on election night 2016. The Dow hit an all-time high 9 hours later. He later admitted he “reacted badly.” The Atlantic diagnosed him with “Trump Derangement Syndrome.”

STEVE LIESMAN — CNBC Senior Economics Reporter

“What President Trump is doing is insane. It is absolutely insane. There is just no other way of describing it.”

Said on air in March 2025 about tariffs. By December 2025, inflation had moderated to 2.7% and the S&P 500 posted its third consecutive year of double-digit gains. He was visibly stunned on live television by the positive CPI data.

TOM WOODS — Libertarian economist and commentator

Persistent warnings about government spending, deficits, and inevitable economic collapse.

Has been forecasting imminent fiscal catastrophe for years while the S&P 500 has roughly quadrupled from its 2016 levels. The deficit hawks have been right about the deficits and wrong about the market consequences for an entire generation.

The Market Strategists

MARKO KOLANOVIC — Former Chief Market Strategist, JPMorgan Chase

“We do not see equities as attractive investments at the moment, and we don’t see a reason to change our stance.” S&P 500 target: 4,200.

Maintained this bearish call through 2023 and 2024 while the S&P 500 rallied over 40%. Was bullish through the 2022 bear market, then flipped bearish right at the October 2022 bottom. JPMorgan showed him the door in July 2024. CNBC had once called him “half-man, half-god.” Bloomberg called him “Gandalf.” The market called him wrong.

BOB ELLIOTT — CEO, Unlimited Funds (Bridgewater alum)

Repeatedly warned that stock market optimism was “getting ahead of economic realities” and cautioned that conditions resembled 1970s-style stagflation.

Throughout 2023 and 2024, while Elliott cautioned the economy would slow and markets were overpriced, the S&P 500 posted back-to-back gains of 24% and 23%. The recession he warned about never materialized.

MIKE GREEN — Chief Strategist, Simplify Asset Management

“We’re possibly setting ourselves up for the worst financial experience of all time” due to passive investing flows.

Green’s thesis that passive investing has created catastrophic structural fragility has been a consistent theme for years. Meanwhile, the very passive index funds he warns about have delivered one of the greatest stretches of returns in market history. Three consecutive years of double-digit S&P 500 returns.

LUKE GROMEN — Founder, Forest for the Trees (FFTT)

“Recession is inevitable.” Called for dollar collapse, sovereign debt crisis, and Treasury market dysfunction as imminent risks.

Predicted recession was inevitable in 2023. It never came. Warned of dollar collapse. The dollar remained resilient. Forecast Treasury dysfunction as near-term certainty. None materialized on his timeline. His macro framework is intellectually fascinating and may eventually prove correct, but following it as a trading signal has cost his audience years of compounding returns.

SCOTT GALLOWAY — NYU Professor, host of Pivot and Prof G podcasts

“I think we’re on the precipice of like a $10 trillion dollar wipeout.” Warned that the Iran war would trigger an ’08-style “which bank is next?” moment through emerging market sovereign defaults.

Said on Pivot podcast in March 2026, weeks before the ceasefire. The S&P 500 never even reached a 10% correction. No emerging market sovereign defaults materialized. Oil is already down 15% this morning. The $10 trillion wipeout did not happen.

Here is the critical point about these individuals: they are not dumb. Several of them are brilliant. But brilliance without humility, without the ability to say “I was wrong and the market is right,” becomes a trap. And that trap has cost their followers dearly.

Now, let us walk through the episodes where their warnings were loudest and where the buying opportunities were greatest.

NOVEMBER 2016

The Election That Would End the World

The night Donald Trump won the presidency, S&P 500 futures plummeted nearly 5%. Dow futures crashed 800 points. The financial media declared it a catastrophe in real time.

Krugman published his “markets will never recover” take before most Americans had gone to bed. Larry Summers projected “a protracted recession to begin within 18 months.” Steve Rattner promised “a market crash of historic proportions.” Eric Zitzewitz, formerly of the IMF, predicted “a likely crash in the broader market.”

What actually happened? The Dow soared 257 points the very next day, brushing against all-time highs. That “never” recovery took roughly nine hours. Over the following year, the Dow climbed approximately 35%, adding some $6 trillion in household wealth.

+35%

DOW JONES RETURN IN THE YEAR FOLLOWING THE 2016 ELECTION

Q4 2018

The First Trade War

By the fall of 2018, the U.S.-China trade conflict dominated headlines. Tariff escalation, a hawkish Federal Reserve, and a brief yield-curve inversion sent markets into a tailspin. The S&P 500 fell 13.5% in the fourth quarter, posting its worst December since 1931. The index nearly entered bear market territory, dropping 19.4% from its September peak to its Christmas Eve trough.

The bears were everywhere. The recession callers were triumphant. The “Trump’s trade war will destroy the economy” narrative was treated as established fact. This was the first major test of a pattern we would see repeated again and again: escalation, panic, resolution, violent repricing higher.

Then the calendar turned. In 2019, the S&P 500 returned 31.5%, its best year since 2013. Investors who added to their positions during that gut-wrenching December were rewarded handsomely. Those who sold near the lows spent the next year watching from the sidelines.

+31.5%

S&P 500 RETURN IN 2019, FOLLOWING THE Q4 2018 PANIC

MARCH 2020

COVID: The Fastest Bear Market in History

On February 19, 2020, the S&P 500 closed at an all-time high. Thirty-three days later, it had fallen 34%. Circuit breakers tripped multiple times. On March 16, the index dropped nearly 12%, the worst day since 1987. The panicans were in full throat. The world was ending. The economy would never recover.

On March 18, 2020, with the S&P 500 already down over 25% and still falling, our CEO Aaron Tuttle hosted a market update call with clients. While the financial media was running wall-to-wall panic and most strategists were calling for further downside, Aaron drew on a historical precedent that almost no one was talking about.

“When the Spanish flu subsided in February 1919, the market began an increase of 50%. It does provide encouragement that once the coronavirus begins to subside, the market will bounce back once again.”

— AARON TUTTLE, CEO, GATEWOOD WEALTH SOLUTIONS, MARCH 18, 2020

Aaron did not stop at the historical comparison. He made a specific call about the shape and speed of the recovery that, in the moment, sounded almost reckless in its optimism.

“Every indication is that once this passes it could be very, very quick and we’ve seen it right… it’s just as quick on the upside.”

— AARON TUTTLE, CEO, GATEWOOD WEALTH SOLUTIONS, MARCH 18, 2020

He pointed to the massive fiscal and monetary stimulus that was already being deployed, noting that “if you have that much fuel, it’s going to come back much, much faster.” And he predicted that “confidence should quickly rebound once the event passes simply due to the relief.”

That call was made five days before the S&P 500 hit its absolute low on March 23. The V-shaped recovery Aaron described is exactly what happened. The index doubled from its lows in 354 trading days, the fastest bull market doubling since World War II.

Here is what is remarkable about the contrast. While Aaron was telling clients to stay the course and prepare for a rapid snapback, the panican class was doing the opposite. Kolanovic, to his credit, made a similar bullish call in late March 2020, predicting the S&P 500 would quickly recover to all-time highs. It was bold, contrarian, and correct. But the tragedy of Kolanovic’s story is what came next. Having earned enormous credibility, he proceeded to stay bullish through the entire 2022 bear market, then turned bearish at the exact bottom in October 2022, and remained bearish through a 40%+ rally. He turned one spectacular correct call into two years of wrong calls that ended his career at JP Morgan.

Aaron, by contrast, has maintained the same disciplined framework across every crisis on this list. Market corrections and bear markets are normal. Selloffs end. Stay invested. The consistency of that message, delivered calmly during the worst moments, is what separates an advisor from a pundit.

For the rest of us, the lesson from COVID was clear: the investors who sold at the bottom missed one of the greatest buying opportunities of a generation. The four-year annualized return from that March 23, 2020 bottom? Approximately 25.7%.

+150%

S&P 500 TOTAL RETURN IN THE 4 YEARS FOLLOWING THE COVID LOW

LATE 2021 – 2022

Inflation Was Not Transitory

To be fair, there was one moment where the establishment consensus was dangerously wrong in the other direction. Throughout 2021, the Federal Reserve insisted that surging inflation was “transitory.” It was not.

Consumer prices hit 40-year highs. The Fed was forced into the most aggressive rate-hiking cycle in a generation. The S&P 500 fell 25% from its January 2022 peak to its October trough. The Nasdaq plunged 33%.

This is where the structural bears had their moment. Gromen’s fiscal concerns were manifesting in real-world inflation. Credit where credit is due.

But being right about the diagnosis does not mean you were right about the prescription. The bears told you to sell. They told you recession was “inevitable.” Eighty percent of economists predicted a 2023 recession. It never came. The S&P 500 rallied off its October 2022 lows and posted double-digit gains in 2023, 2024, and 2025. Three consecutive years.

Being right about the problem does not make you right about the solution. The bears correctly identified inflation. They were dead wrong about what it meant for equity investors who stayed the course.

APRIL 2025

Liberation Day and the Tariff Tantrum

On April 2, 2025, President Trump announced sweeping “reciprocal” tariffs that exceeded even the most bearish expectations. In four days, the S&P 500 shed more than 12%. The Dow lost nearly 4,600 points.

Liesman went on CNBC and called the tariff policy “insane,” comparing it to “steering the Titanic towards the iceberg.” UBS warned of a “meaningful recession.” The panicans were vindicated. For about a week.

Seven days later, Trump announced a 90-day pause. The S&P 500 surged 9.5% in a single session. By May 13, the index was positive for the year. By June 27, 2025, it hit a new all-time high. By December 2025, inflation had moderated to 2.7% and Liesman was visibly stunned on live television by how good the data looked.

This is where the pattern becomes undeniable. And this is where our Chief Investment Officer, Chris Arends, published an internal framework that we believe every investor should understand.

In March 2026, our CIO Chris Arends distributed an internal briefing we titled “The Trump Conflict Playbook.” The thesis is straightforward: since Trump’s 1st term, every major geopolitical and trade conflict has followed a repeating 10-step cycle from escalation to resolution. Every single one has ended with a deal.

The cycle moves through three phases. First, a Pressure Phase where posturing and escalation build credibility. Second, a Volatility Phase where markets price in a prolonged conflict and defensive positioning reaches an extreme. Third, a Resolution Phase where de-escalation signals emerge, a deal is struck, and markets reprice violently higher.

The key insight: the repricing is abrupt, not gradual, because by the time a deal becomes credible, investors are already defensively positioned. When uncertainty collapses, those positions unwind all at once. This pattern played out in the April 2025 tariff pause, the August 2025 extension, the October 2025 China deal, the January 2026 Greenland/EU deal, the February 2026 India deal, and now the Iran ceasefire.

The playbook’s conclusion, written five weeks before today’s ceasefire: “Trump does NOT want a forever war. His top three policy priorities are all directly undermined by a prolonged conflict. Investors currently defensively positioned should expect that unwind to be swift.”

+16%

S&P 500 RETURN IN THE YEAR SINCE “LIBERATION DAY” (APRIL 2025)

APRIL 2026

The Iran Conflict: Today’s Resolution

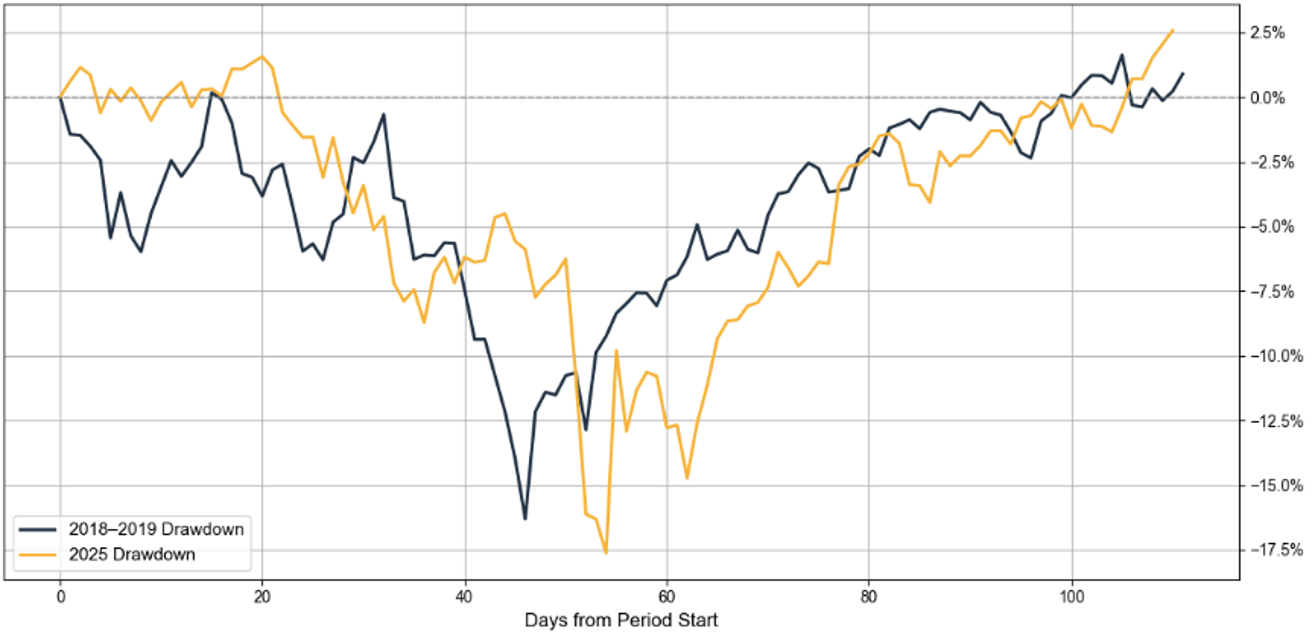

On February 28, 2026, the United States and Israel launched airstrikes on Iran. The conflict closed the Strait of Hormuz, sent oil surging nearly 70%, pushed gasoline above $4 a gallon, and knocked the S&P 500 down nearly 10% from its highs.

The Conflict Playbook called it in real time. In early March, with markets deep in the Volatility Phase (Step 6), the framework identified that Brent crude crossing $85, the Dow falling over 1,100 points, and markets pricing in prolonged conflict risk were the exact conditions that historically precede de-escalation. The playbook noted key thresholds: Brent above $90, equities down 5%+, and gas prices up 10%+ as triggers that would substantially raise the probability of negotiation headlines.

“We’re on week three. I know it sounds a little crazy to think this could be done in 2 to 3 weeks, but that has really become our base case that it’s not a prolonged conflict. He wants to make you think it is because that’s his steps before de-escalation.”

— Chris Arends, MARCH 20th, 2026

Our team’s conviction was rooted in a simple observation: a prolonged war accomplished none of Trump’s stated objectives. As we noted at the time, “I think Trump signaled he wants this conflict to be done before he goes to China and has that summit.” The escalation was not the strategy. The escalation was the leverage. The strategy was always the deal.

Every threshold was breached. And exactly as the framework predicted, the resolution followed. A ceasefire brokered through Pakistan, a commitment to reopen the Strait of Hormuz, and peace talks scheduled for Friday in Islamabad.

As of this morning, S&P 500 futures surged 2.7%. Dow futures jumped over 1,000 points. Oil cratered more than 15%. The S&P 500 sits at roughly 6,600, just 5.5% below its all-time high. The conflict’s maximum drawdown never even reached the technical definition of a correction.

Step 10 of the playbook: “The violent repricing and political victory lap.” That is today.

The Panicans as Contrarian Indicators

Here is the uncomfortable truth that nobody on financial television will say out loud: the loudest voices during market panics are almost always the best contrarian buy signals available.

When Krugman says markets will “never” recover, buy. When Kolanovic’s bearish target is the lowest on Wall Street, buy. When Liesman calls policy “insane” on live television, buy. When Gromen says recession is “inevitable,” buy. When Green warns of “the worst financial experience of all time,” buy. When 80% of economists predict a recession, buy.

This is not a joke. This is a decade of data. Every single major bottom on this list was accompanied by maximum bearish consensus from the panican class. And every single one was followed by substantial gains for investors who had the discipline to act against the prevailing narrative.

Kolanovic’s story is perhaps the most instructive. He was once the most respected strategist on Wall Street. He made one of the great calls of the COVID era. And then his bearish bias consumed him. He maintained a 4,200 S&P target while the index screamed past 5,500. JPMorgan let him go in July 2024. The S&P 500 has gained roughly 40% since the October 2022 bottom he told everyone to sell.

The loudest voices during market panics are almost always the best contrarian buy signals available. This is not an opinion. This is a decade of data.

Trump Derangement Syndrome Destroys Portfolios

There is a pattern in every single one of these episodes, and it goes beyond simple fear. It is politically motivated fear. It is what happens when a person’s deep-seated political bias distorts their ability to think clearly about markets, economics, and risk.

When someone suffers from Trump Derangement Syndrome, their analytical framework collapses. They cannot see the economy for what it is because they are too busy seeing it through the lens of what they desperately want it to be. They want the other side to fail. They want the market to punish the country for making what they consider the wrong electoral choice. And that desire, whether conscious or not, infects every financial decision they make.

Look at the evidence. Krugman predicted a “global recession with no end in sight” not because his models told him so, but because he was horrified by the election result. The Atlantic later diagnosed Krugman specifically with Trump Derangement Syndrome by name. He himself admitted he “reacted badly.”

Liesman, separately, called tariff policy “insane” on live television not because the data supported that conclusion, but because his political priors told him protectionism could not possibly work. When the inflation data came in better than expected months later, he was visibly shocked on his own broadcast.

Tom Woods, for all his economic sophistication, has been so consumed by his ideological opposition to government intervention that he has missed one of the greatest wealth-creation periods in American history. His audience has been told for years that the fiscal house of cards is about to collapse. It has not. And every year they stayed underweight equities on that thesis, they fell further behind.

On the market strategist side, the pattern is slightly different but equally costly. Kolanovic, Elliott, Green, and Gromen are not motivated by partisan politics in the same way. Their bias is structural. They see systemic risks, passive flow distortions, fiscal unsustainability, and market fragility. And they are not entirely wrong about any of those things. But the gap between “these are real risks” and “sell your stocks now” is where fortunes are made and lost. Being aware of structural risk is wisdom. Letting structural risk prevent you from participating in a generational bull market is tragedy.

The panicans are often directionally correct. Deficits are unsustainable. Passive flows do distort price discovery. Valuations do get stretched. Geopolitical risk is real. But direction without timing is not an investment thesis. It is a worry. And worries do not compound. Equities do.

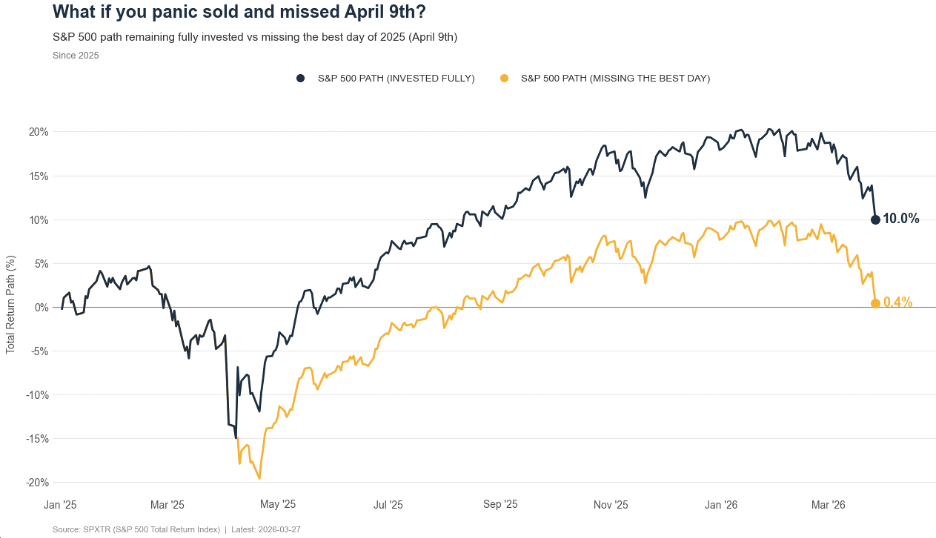

The chart above from Ritholtz tells the story as well as any paragraph can. Missing just the single best day of 2025, April 9th, the day Trump announced the tariff pause, turned a 10% annual return into a 0.4% return. One day. The difference between a strong year and a lost year. That is the cost of panicking. That is the tax the panicans impose on their followers.

If you take one thing from this piece, let it be this: your political opinions and your investment strategy must live in separate rooms. The moment you allow your feelings about a president, a party, or a policy to dictate your financial decisions, you have given control of your wealth to the least rational part of your brain.

The market does not care who you voted for. It does not care how you feel about the person in the Oval Office. It cares about earnings, cash flows, innovation, and the long-term trajectory of the most dynamic economy the world has ever produced.

Stay invested. Stay disciplined. Stay rational. And when the panicans start screaming again, and they will, remember: that is your signal to get more aggressive, not less.

Sometimes the hardest part isn’t what the market is doing—it’s knowing how to respond in the moment. Having the right perspective can make all the difference. If this raises questions or you’d like to go deeper, feel free to schedule a conversation with us below.

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

The fast price swings in commodities will result in significant volatility in an investor’s holdings. Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors. Indexes are unmanaged and cannot be invested in directly.

The NASDAQ Composite Index measures all NASDAQ domestic and non-U.S. based common stocks listed on The NASDAQ Stock Market. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the Index.

Much has changed since then. Tax filing season opened on January 26th, more than three million families have now signed up, a Super Bowl ad ran during the pregame broadcast, President Trump promoted the accounts during his State of the Union address on February 24th and directed the nation to trumpaccounts.gov, and a new online sign-up option just launched.

Here’s our refreshed take on what this program means for your family.

The Basics: What Are Trump Accounts?

Trump Accounts, formally known as 530A Accounts under the One Big Beautiful Bill Act, are a new type of individual retirement account designed specifically for children. They’re custodial in nature, meaning a parent or guardian controls the account until the child turns 18.

How the Trump Accounts Actually Work

Eligibility: Any U.S. citizen under age 18 with a valid Social Security number can have an account opened on their behalf. Each child may have only one Trump Account.

Account Benefits

The $1,000 Seed: Children born between January 1, 2025 and December 31, 2028 who are U.S. citizens are eligible for a one-time $1,000 pilot program contribution from the U.S. Treasury. This deposit is expected no earlier than July 4, 2026.

Annual Contributions: Families, employers, and others may contribute up to a combined $5,000 per child per year. Employers may contribute up to $2,500 (per employee) of that amount under Section 128 as a fringe benefit. The $5,000 limit will be adjusted for inflation starting in 2027. No earned income is required, and contributions don’t affect traditional or Roth IRA limits for the contributor.

Account Limitations

Charitable & Government Contributions: Qualified general contributions from government entities and 501(c)(3) organizations do not count against the $5,000 annual limit. These are separate and additive.

Investment Rules: All funds must be invested in low-cost, broad U.S. equity index funds or ETFs tracking qualified indexes such as the S&P 500. Annual fees are capped at 0.10% (10 basis points), and no leverage is permitted.

No Withdrawals Before 18: Generally, no distributions may be made before the year the child turns 18, with very limited exceptions for death, excess contributions, and certain rollovers.

What’s New About Trump Accounts Since December

1. Tax Season Sign-Ups Are Live

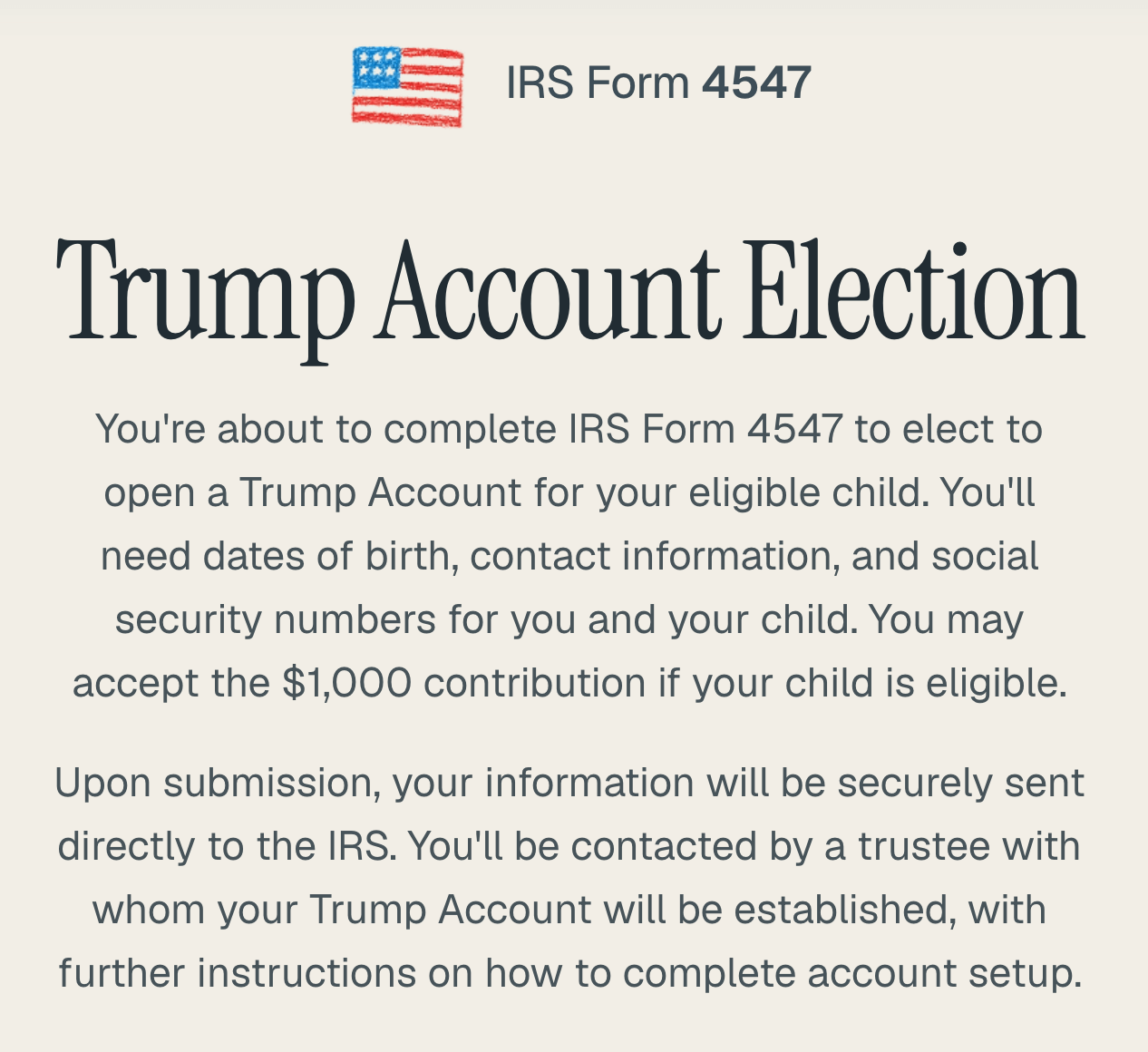

As of January 27, 2026, families can elect to open Trump Accounts by filing IRS Form 4547 with their 2025 federal tax return. The form includes two elections: one to open the account and one to request the $1,000 pilot program contribution (if eligible).

The form accommodates up to two children and families with more eligible children can attach additional copies. Filing electronically with your tax return is the fastest and easiest method.

2. New Online Sign-Up Option

Following the Invest America Super Bowl ad last weekend, a new online sign-up form launched at trumpaccounts.gov, ahead of the originally planned mid-2026 timeline. This gives families a second pathway to open accounts outside of the tax filing process. Here’s what the sign-up experience looks like:

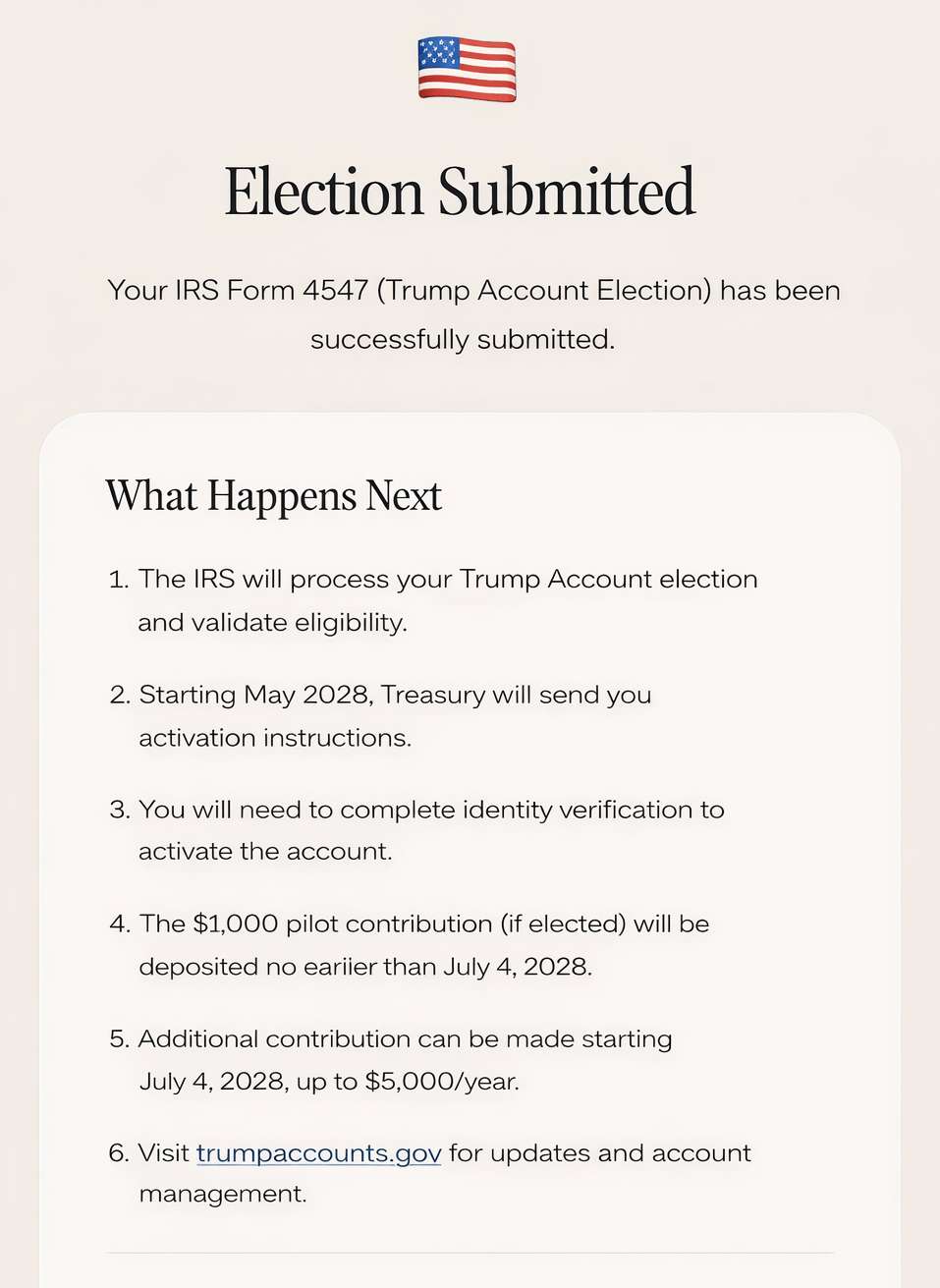

The Form 4547 election page at trumpaccounts.govConfirmation and next steps after submission

3. Over Three Million Families Have Enrolled

According to the White House, more than three million families had signed up as of the State of the Union address on February 24th. That milestone was up from one million just five days into tax filing season, and Treasury Secretary Scott Bessent noted that approximately 500,000 elections were made in the first three days alone. During the speech, President Trump called the program “something that’s so special” that has “taken off and gone through the roof,” and directed the nation to sign up at trumpaccounts.gov.

4. Activation Timeline

After filing Form 4547, the Treasury Department will contact parents starting in May 2026 to complete an identity verification process and activate accounts. You’ll be contacted by the partner financial firm where your Trump Account will be held with further instructions. Contributions and seed deposits will begin on July 4, 2026.

5. The Dell Foundation Gift

Michael and Susan Dell have pledged $6.25 billion to seed accounts for approximately 25 million children who missed the eligibility cutoff for the $1,000 federal deposit. Their gift provides $250 per eligible child. To qualify for the Dell contribution, children must be age 10 or under, born before January 1, 2025, and live in ZIP codes where the median household income is below $150,000. This is expected to reach children across roughly 75% of U.S. ZIP codes.

An important clarification: The Dell gift goes to a different population than the Treasury’s $1,000. It is not $250 on top of $1,000. Children born 2025 through 2028 receive the $1,000 government seed. Children born before 2025 who are age 10 and under may receive the $250 Dell contribution. Both groups benefit, but through separate funding streams.

6. Growing Employer and Corporate Support

A growing list of major U.S. corporations have pledged matching deposits or contributions for employees. Venture capitalist Brad Gerstner has also pledged $250 for each child under five with a Trump Account in Indiana. We expect this trend of employer and philanthropic participation to continue expanding.

How the Tax Treatment Works

Understanding the tax treatment matters because it affects whether you should add your own money to these accounts or use other vehicles instead.

Think of it in two phases:

PHASE 1: Before Age 18 (The Accumulation Phase)

During childhood, contributions are made with after-tax dollars, and investment growth accumulates tax-deferred. Parents or guardians maintain control of the account during this period. This phase is straightforward.

PHASE 2: After Age 18 (The IRA Conversion Phase)

At age 18, Trump Accounts automatically convert to traditional IRAs. This conversion fundamentally changes how the account functions:

What Changes on Trump Accounts for Those Over 18?

Access and Control: The young adult gains full control as the account becomes a traditional IRA in their name.

Withdrawals and Taxes: This is where it gets important. Distributions are taxed as ordinary income on all earnings and growth (though your original contributions come back tax-free). Additionally, the 10% early withdrawal penalty applies to distributions before age 59½.

The Exception Rules:

The 10% penalty (not the taxes) can be waived for:

First-time home purchases (up to $10,000)

Qualified education expenses

Business startup costs in certain circumstances

Here’s the crucial point many families miss: These “qualified expenses” only waive the 10% penalty—they do NOT eliminate the ordinary income tax on the earnings. Even when funding college or buying a first home, you’ll owe income tax on all the growth.

Investment Flexibility: After conversion, the account can be invested more broadly according to traditional IRA rules, no longer restricted to designated index funds.

Why This Matters: This automatic conversion to a traditional IRA means families should carefully consider whether contributing their own funds makes sense compared to other savings vehicles like 529 plans (where qualified education withdrawals are completely tax-free) or custodial accounts (where flexibility is greater).

Our General Perspective on Trump Accounts

Accept the free money. If your child qualifies for the $1,000 Treasury seed or the $250 Dell contribution, opening an account is straightforward. You’re accepting a gift with no cost to you. We’d help every eligible family capture this benefit. The Treasury projects that the $1,000 seed alone could grow to roughly $6,000 by age 18, $15,000 by age 27, or over $243,000 by age 55, assuming historical market returns.

Think carefully about your own contributions. For most families whose primary goal is funding education, 529 plans still deliver better tax outcomes. A 529 offers completely tax-free growth potential and withdrawals for qualified education expenses. Trump Accounts tax all growth as ordinary income at withdrawal, even for education. That’s a meaningful difference.

When Trump Accounts Make Sense for Your Plan

That said, Trump Accounts can make sense when:

You’re already maximizing 529 contributions and want additional tax-advantaged savings

Your priority is very long-term wealth building, with retirement savings starting at birth

You’re targeting a first home down payment for your child

Your employer is offering matching contributions, which is additional free money worth capturing

You want to diversify across savings vehicles with different tax treatments

Check with your employer. A growing number of companies are pledging contributions to Trump Accounts as an employee benefit. If your employer is participating, that’s money you don’t want to leave on the table, similar to a 401(k) match.

Action Steps for Families

File Form 4547 with your 2025 tax return. This is the fastest way to open an account and elect the $1,000 pilot program contribution for eligible children. You can also sign up online at trumpaccounts.gov now.

Check your employer’s plans. Ask your HR or benefits team whether your company is making Trump Account contributions under Section 128.

Don’t rush your own contributions. Contributions won’t be accepted until July 4. Use this time to evaluate whether a Trump Account, 529 plan, or combination makes the most sense for your family’s goals.

Keep records. Documentation of contribution sources matters for future distribution taxes and rollover reporting. Start organized from day one.

How Gatewood Can Help You Analyze Trump Accounts

This program launches on July 4, which gives us time to plan strategically together. The questions we help families answer are straightforward but important:

Does your family qualify for the maximum benefits?

Should you contribute your own funds, or does a 529 or custodial account better serve your goals?

And how does this fit into your broader wealth-building strategy?

We specialize in exactly these conversations, the kind where “it depends” actually becomes “here’s exactly what makes sense for you.” We’re fiduciary advisors, so this isn’t about selling you on Trump Accounts. It’s about helping you make the most informed choice for your family’s specific circumstances.

Ready to discuss strategy?

Important Considerations

This program is new, and IRS regulations continue to evolve. The information provided here reflects program details as understood in December 2025, but specific rules and procedures may change as implementation progresses. Investment returns are not guaranteed, and tax laws may change. This material is educational and not a recommendation for any specific action.

For personalized guidance on whether Trump Accounts make sense for your family, we encourage you to consult with a financial advisor and tax professional who can evaluate your complete financial picture.

Important Disclosures

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. Gatewood Wealth Solutions and LPL Financial do not provide legal or tax advice or services.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Prior to investing in a 529 Plan investors should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

Ten months ago, the sky was falling.

Sweeping tariff announcements sent the S&P 500 plunging nearly 20% from its February 2025 peak, wiping out over $6 trillion in market value in two trading sessions. Headlines screamed recession. Pundits predicted the worst. The temptation to sell everything and hide in cash was overwhelming.

Here’s what our clients did: absolutely nothing.

Their strategy, Fortress Gatewood, held. Their fortress held. Their portfolios recovered, and then some.

Zero families served by Gatewood Wealth Solutions panic sold during the 2025 market correction. Not one.

Today, the S&P 500 is trading near all-time highs. But we’re not writing this to celebrate. We’re writing it because the next correction is coming, and the real question is whether you’ll be ready.

What Happened: The 2025 Tariff Correction

On February 19, 2025, the S&P 500 closed at an all-time high of 6,144.

Then things got ugly. Fast.

February 19 to March 13: The S&P 500 dropped over 10% on tariff fears alone, entering correction territory before “Liberation Day” even arrived.

April 2 to April 8: Sweeping tariffs on nearly all U.S. trading partners triggered the worst two-day loss in S&P 500 history. The VIX spiked to levels not seen since the COVID-19 pandemic.

April 8: The bottom. The S&P 500 sat nearly 19% below its February peak, flirting with official bear market territory.

Then, just as quickly, the reversal. A 90-day tariff pause on April 9 sent the S&P 500 surging 9.5% in a single session, one of its best days ever. By May 13, the index was positive for the year. By June 27, it hit a new all-time high.

From the April 8 bottom to today, the S&P 500 has gained roughly 40%.

The entire round trip took about four months. Investors who sold at the bottom missed all of it.

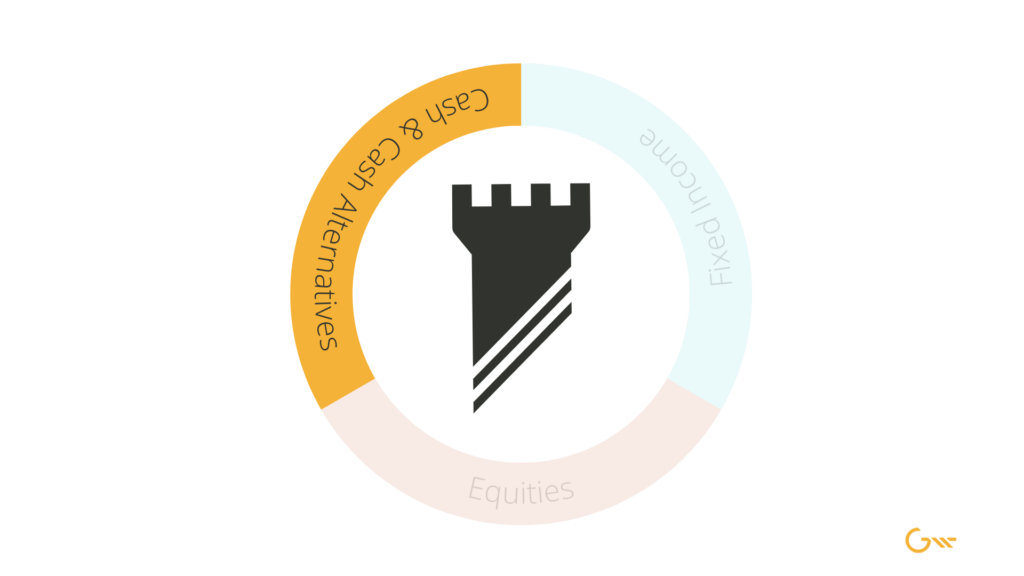

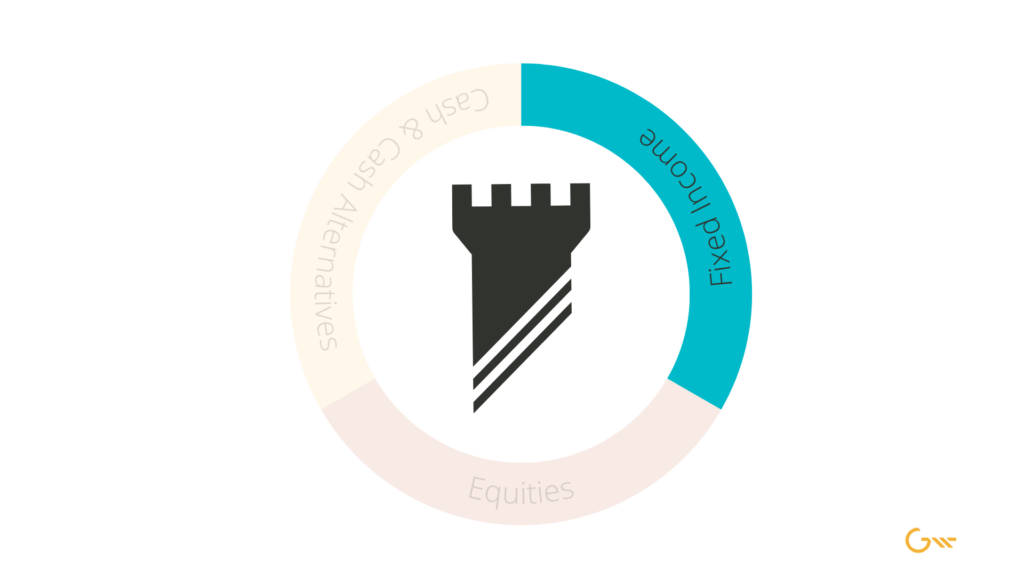

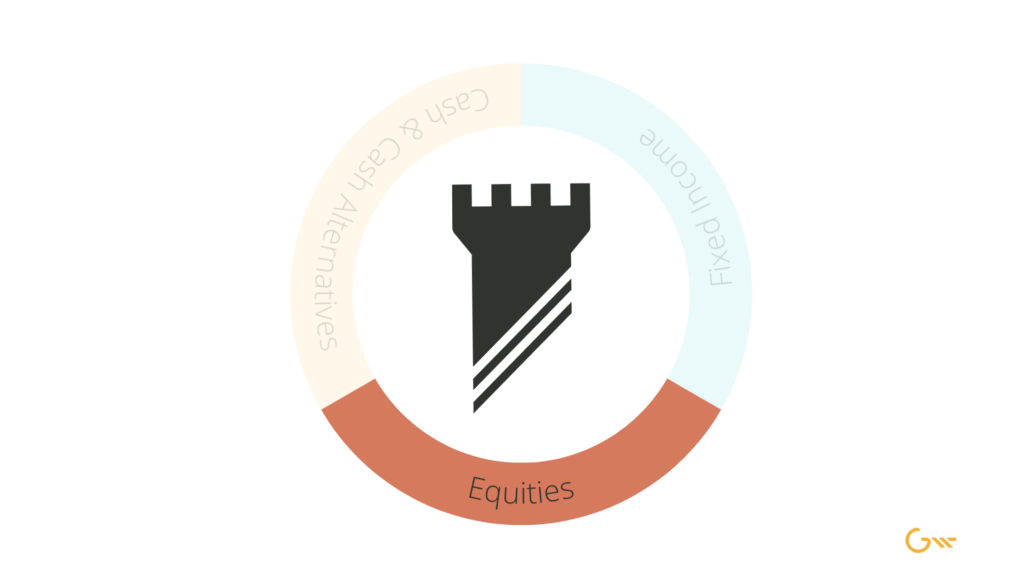

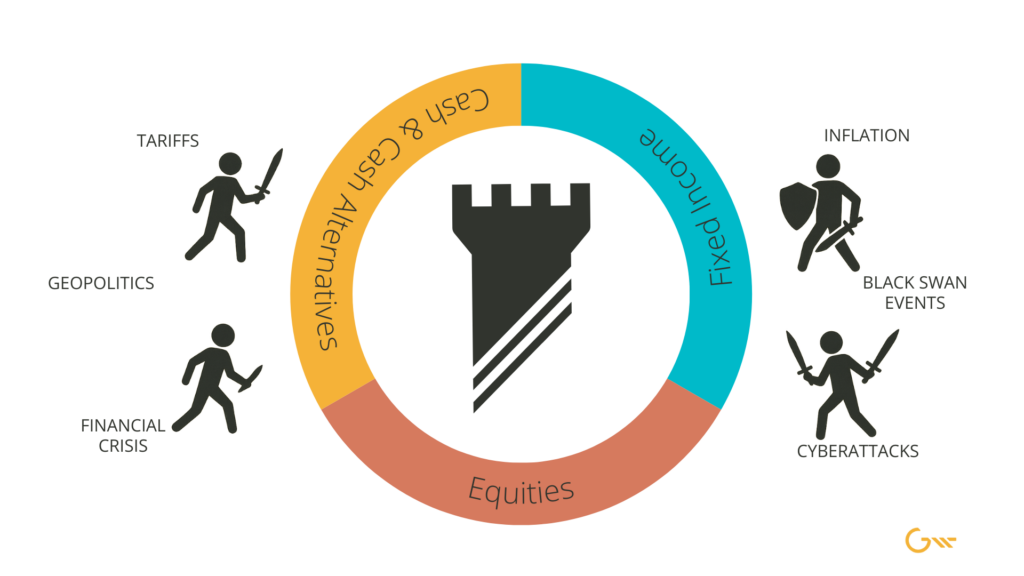

What Is Fortress Gatewood?

Fortress Gatewood is the planning framework we use to help families navigate market volatility without being forced into reactive decisions. It’s built around intentional layers (or “moats) of liquidity, income, and long-term growth, each aligned to different time horizons and real-world spending needs.

By clearly separating short-term cash needs, intermediate income sources, and long-term growth capital, the structure helps clients understand which dollars are meant to be used now, which are designed to support future income, and which are positioned for long-range objectives.

The goal isn’t to predict markets, but to create enough flexibility and clarity that market movement doesn’t dictate decisions when it matters most.

Download Your Free Copy

How the Fortress Worked

This is exactly the scenario Fortress Gatewood was designed for.

Moat Ring 1: Cash. Two years of spending in liquid reserves. No one needed to sell a single share to pay their bills. No forced selling. No panic.

Moat Ring 2: Fixed Income. Five to eight years of high-quality bonds provided less volatility with stable income. A second wall of defense while equities took the hit.

Moat Ring 3: Equities. Long-term growth capital with a 7 to 10+ year horizon. Because no one was relying on these funds for near-term needs, they could ride the storm and capture the rebound.

But here’s what made the difference: we didn’t just defend. We attacked.

On April 7, 2025, one day before the market bottomed, Chris Arends and the Gatewood Investment Committee sent guidance to every advisor on the team:

“Please contact clients with dry powder and suggest investing 1/2 to strategy now. Dry powder means funds not earmarked for short-term or mid-term spending needs. It must be long-term (>7 years).”

— Chris Arends, Gatewood Investment Committee, April 7, 2025 at 8:47 AM

That’s not a memo written in hindsight. That’s real-time guidance, issued the morning before the market hit its lowest point.

Dry powder means long-term capital not earmarked for short-term or mid-term spending. Funds with a 7+ year horizon. Because Moat Rings 1 and 2 were fully funded, we knew exactly which dollars could go to work at depressed prices, and we deployed them with conviction.

As our investment partner, Aaron Tuttle, said that same morning:

“Since 1957, we’ve had 12 corrections in the S&P 500 greater than 20%. Half were between 20-30%, three were between 30-40%, and three were greater than 40%. If you have a lot of cash, don’t overcomplicate it. Invest half now, another quarter at a 30% drop, and go all-in, buying everything you can at a greater than 40% drop. You might only get one or two opportunities at that level in your lifetime.”

Other investors were frozen. Ours were buying.

That’s the power of a fortress.

The Bigger Picture

The 2025 correction joins a pattern every investor should know by heart:

Market Event

Decline

Recovery Time

Dot-Com Crash (2000–2002)

-49.1%

7.2 Years

Global Financial Crisis (2007–2009)

-56.8%

5.5 Years

COVID-19 Crash (2020)

-34%

~6 Months

2022 Bear Market

-27.5%

~2 Years

2025 Tariff Correction

~19%

~4 Months

Every single one felt like the end of the world. Every single one recovered. Every single time, the investors who stayed disciplined won.

But Here’s What Should Keep You Up at Night

“The biggest risks are always the ones nobody sees coming. The events that aren’t on anyone’s radar are what move the world most. People are generally good at predicting the future except for the surprises that actually matter.”

— Morgan Housel, Same as Ever

The 2025 correction was the easy version. No recession. Strong consumer spending. Resilient corporate earnings. Room for the Fed to cut rates. The economy absorbed the shock and bounced back in months. V-shaped recovery!

That won’t always be the case.

When we study the last 50 years of S&P 500 bear markets, the data is clear: the presence or absence of a recession changes everything.

Bear Markets Without a Recession (1987, 2022)

Metric

Average

Decline

-30%

Peak to Trough

~6.5 months

Full Round Trip

~23.5 months (~2 years)

Bear Markets With a Recession (1980–82, Dot-Com, GFC, COVID)

Metric

Average

Decline

-42%

Peak to Trough

~17.5 months

Full Round Trip

~46 months (~3.8 years)

Recessionary bears are 12 percentage points deeper. The decline phase is 3x longer. The total round trip takes twice as long.

And if you exclude the anomalous COVID recovery (compressed by unprecedented government intervention), the three traditional recessionary bears averaged about 5 years from peak to recovery.

Since 1975, four out of six bear markets have coincided with recessions. We are statistically due for another one. The question isn’t if. It’s when.

Are you building your fortress now, while the sun is shining? Or will you try to build it in the middle of the storm?

The Danger of All-Time Highs: Complacency

Here’s the part most people don’t want to hear: all-time highs are when fortresses get built, not when they get tested.

Right now, with markets at record levels and three straight years of strong returns behind us, it’s tempting to relax. To assume the good times will continue indefinitely. To skip the disciplined work of maintaining cash reserves and rebalancing into fixed income.

But the 2025 correction is a reminder that the next downturn doesn’t send a calendar invite. It shows up unannounced, sometimes triggered by a single speech in a Rose Garden.

With the S&P 500 near 7,000 and all-time highs stacking up, most investors are relaxed. We’re not.

We’re using this moment of strength to prepare for the next moment of weakness:

Reviewing cash positions to make sure every client has their full 2-year liquidity buffer

Rebalancing into fixed income to lock in yields and maintain the 5 to 8 year spending bridge

Harvesting equity gains to fund and strengthen the outer moat rings

Stress-testing every plan against recessionary scenarios: 40%+ drawdowns, multi-year recoveries, rising unemployment

We’re not predicting a crash. We never do. We’re preparing for one, because that’s what we always do.

The Firm to Family™ Advantage: Why the Fortress Held

Zero panic selling across our entire client base is not an accident. It’s the result of how Gatewood is built.

At most firms, the investment team doesn’t talk to the financial planner. The financial planner doesn’t talk to the tax advisor. And nobody coordinates the message to the client when markets are in freefall.

At Gatewood, our Firm to Family™ structure means every professional who touches your financial life is working from the same plan, communicating continuously, and aligned on the same strategy.

When markets dropped in April, your wealth planner could tell you with precision how many months of expenses were covered without touching a single equity position. The Investment Committee was providing real-time guidance on deploying dry powder. And the planning team was tracking the tax implications of every move to make sure nothing was done without considering the full picture.

Our clients didn’t panic because they didn’t have to. They had a plan, a team, and a fortress. And they heard from their advisor, personally, before the bottom even arrived.

The 2025 correction proved the Fortress Gatewood system works. Our clients didn’t panic. They didn’t sell. They didn’t miss the recovery. Zero families. Zero panic sales. Many of them used the downturn to buy at depressed prices and came out stronger on the other side.

But the next test might not be a four-month correction. It could be a recessionary bear market that grinds on for years. The families who navigate that with confidence will be the ones who built their fortress today, while markets were strong and emotions were calm.

Don’t wait for the storm to start digging the moat.

Important Disclosures

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. Gatewood Wealth Solutions and LPL Financial do not provide legal or tax advice or services.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Appendix: Sources

S&P 500 Historical Data & 2025 Market Correction

S&P Dow Jones Indices. S&P 500 historical closing prices.

“2025 Stock Market Crash.”

NBC News. “S&P 500 Hits an All-Time High—Rebounding to Its Level When Trump’s Second Term Began.” June 27, 2025.

CBS News. “The Stock Market Is Nearing a Record High After Cratering in April. Here’s Why.” June 27, 2025.

“How the Stock Market Made Back All Its Losses After Trump Escalated the Trade War.” May 4, 2025.

CNN Business. “What to Expect From Stocks in 2026.” January 1, 2026.

S. Bank. “Stock Market Under the Trump Administration.” Updated February 4, 2026.

Trading Economics. “United States Stock Market Index.” February 10, 2026.

Bank for International Settlements. “Understanding the Swift Market Recovery After the April 2025 Tariff Shock.”BIS Quarterly Review, September 2025.

April 2025 Tariff Crash Details

CNN Business. “Dow Plunges 2,200 Points as Tariff Tumult Rocks Markets.” April 4, 2025.

“Tariff Shock: Top S&P 500 Winners and Losers (April 2–16, 2025).”

Bear Market Historical Data & Recession Analysis

S&P 500 bear market peak-to-trough and recovery data, 1975–2025.

S&P 500 historical performance and earnings data.

National Bureau of Economic Research (NBER). S. business cycle expansions and contractions.

“A History of Bear Markets.”

“A History of Stock Market Percentage Declines (15% to 50%).”

“Here’s How Often Stocks Dip 5% or More.”

Austin Wealth Management. “Dealing With the Dips.”

2026 Market Outlook & Valuation

The Motley Fool. “With the S&P 500 at an All-Time High to Start 2026, Is It Smart to Buy Stocks?” January 9, 2026.

The Motley Fool. “History Says a Turning Point Is Likely Coming for the S&P 500 in 2026.” January 1, 2026.

Visual Capitalist. “152 Years of S&P 500 Returns (and Predictions for 2026).” January 2026.

Advisor Perspectives. “S&P 500 Snapshot: Index Closes at Record High.” January 2, 2026.

Books Cited

Housel, Morgan. Same as Ever: A Guide to What Never Changes. Portfolio/Penguin, 2023.

Understanding the New Children’s Investment Accounts Launching in 2026

Every parent dreams of giving their children a head start in life. Starting in 2026, a new federal program will do exactly that—and thanks to an extraordinary $6.25 billion pledge from Michael and Susan Dell, the gift just got bigger.

Here’s what makes this program remarkable: If you have children age 10 or under, they may automatically receive up to $1,250 in free investment capital—$1,000 from the government plus $250 from the Dell Foundation. No action required beyond enrollment. For a family with two eligible children, that’s $2,500 invested in their future at no cost to you.

The question isn’t whether to accept this gift—it’s whether these “Trump Accounts” make sense as part of your broader savings strategy for your children.

What These Accounts Are Called

These accounts are commonly known as “Trump Accounts” or “Children’s Investment Accounts.” They’re formally defined in Section 530A of the One Big Beautiful Bill Act and are sometimes referenced as “530A accounts” in tax documentation.

Official Website: All program and enrollment information will be published at trumpaccounts.gov

Program Timeline

Spring 2026: Families can begin enrolling by filing IRS Form 4547 with their tax returns or through other designated methods.

Mid-2026: Online enrollment portal launches at trumpaccounts.gov.

July 4, 2026: The program formally launches with seed deposits funded, contributions enabled, and full account access available.

How Trump Accounts Work – The Basics

Eligibility

Any U.S. citizen under age 18 with a Social Security number can have an account opened on their behalf. Children born between 2025 and 2028 automatically receive a $1,000 government-funded seed deposit.

The Dell Foundation Gift

The Dell family’s $6.25 billion contribution provides an additional $250 to eligible children who meet specific criteria: age 10 and under, born before January 1, 2025, and living in ZIP codes with median household incomes of $150,000 or less. This enhancement reaches approximately 25 million children across roughly 75% of U.S. ZIP codes.

Annual Contributions

Families may contribute up to $5,000 per year per child, including employer contributions. Employers may contribute up to $2,500, which counts toward the $5,000 annual cap. Philanthropic enhancements like the Dell gift are separate and don’t count against contribution limits.

Investment Requirements

All funds must be invested in low-cost, broad U.S. equity index funds designated by the Treasury Department. Annual fees are capped at 0.1%. Accounts are initially established through the Treasury and can later be transferred to approved private financial institutions.

The Critical Detail: What Happens to the Tax Treatment

Understanding the tax treatment matters because it affects whether you should add your own money to these accounts or use other vehicles instead. Think of it in two phases:

PHASE 1: Before Age 18 (The Accumulation Phase)

During childhood, contributions are made with after-tax dollars, and investment growth accumulates tax-deferred. Parents or guardians maintain control of the account during this period. This phase is straightforward.

PHASE 2: After Age 18 (The IRA Conversion Phase)

At age 18, Trump Accounts automatically convert to traditional IRAs. This conversion fundamentally changes how the account functions:

Access and Control: The young adult gains full control as the account becomes a traditional IRA in their name.

Withdrawals and Taxes: This is where it gets important. Distributions are taxed as ordinary income on all earnings and growth (though your original contributions come back tax-free). Additionally, the 10% early withdrawal penalty applies to distributions before age 59½.

The Exception Rules:

The 10% penalty (not the taxes) can be waived for:

First-time home purchases (up to $10,000)

Qualified education expenses

Business startup costs in certain circumstances

Here’s the crucial point many families miss: These “qualified expenses” only waive the 10% penalty—they do NOT eliminate the ordinary income tax on the earnings. Even when funding college or buying a first home, you’ll owe income tax on all the growth.

Investment Flexibility: After conversion, the account can be invested more broadly according to traditional IRA rules, no longer restricted to designated index funds.

Why This Matters: This automatic conversion to a traditional IRA means families should carefully consider whether contributing their own funds makes sense compared to other savings vehicles like 529 plans (where qualified education withdrawals are completely tax-free) or custodial accounts (where flexibility is greater).

Comparing Your Options: Trump Accounts vs. 529 Plans vs. UTMA Accounts

We believe informed decisions come from clear comparisons. Here’s how Trump Accounts stack up against the savings vehicles you may already be using:

Trump Accounts offer a $1,000 government seed deposit (for children born between 2025 and 2028) plus potential philanthropic enhancements like the Dell gift. The $5,000 annual contribution limit includes employer contributions. Investment growth is tax-deferred, and the account converts to a traditional IRA at age 18. Withdrawals after 18 are taxed as ordinary income with standard IRA penalties and exceptions applying. The parent controls the account until age 18, then the child gains full access.

529 Plans have no government seed funding but offer no annual contribution limits (though lifetime caps apply by state). Contributions may be deductible at the state level. Investment growth is completely tax-free when used for qualified education expenses. Withdrawals for education are entirely tax-free, while non-education withdrawals face taxes and penalties. The account owner retains control indefinitely and can change beneficiaries.

UTMA Accounts offer no government funding and no annual limits beyond gift tax considerations. There are no tax deductions for contributions. Investment growth is taxable annually, and the kiddie tax may apply. Withdrawals can be used for any purpose benefiting the child with no special tax treatment or penalties. The child gains full, unrestricted control at age 18 to 21 (depending on state), and investment options are highly flexible.

The Bottom Line: The right choice depends entirely on your family’s priorities and timeline—which is exactly the kind of conversation we help clients navigate.

Our Perspective: When Trump Accounts Make Sense

At Gatewood, we believe in giving you straight talk about financial products—even new, politically branded ones. Here’s our professional perspective:

The free money is a no-brainer. If your child qualifies for the government seed and Dell enhancement, opening an account is essentially accepting a gift. We’d help every eligible family capture this benefit.

Your own contributions require more thought. For most families focused on education funding, 529 plans deliver better tax outcomes. The Trump Account’s conversion to an IRA at 18 means you’ll pay ordinary income tax on withdrawals—even for education. That’s objectively less attractive than a 529’s completely tax-free treatment for qualified education expenses.

But there are scenarios where these accounts shine:

You’re already maxing out 529 contributions and want additional tax-advantaged savings

Your priority is very long-term wealth building (retirement savings starting at birth)

You’re specifically targeting a first home down payment for your child

You want to diversify across multiple savings vehicles with different tax treatments

Remember that implementation details are still evolving. The IRS continues to issue guidance on program specifics, and some questions remain unanswered as of December 2025.

The key question isn’t “Are Trump Accounts good or bad?” It’s “Are they right for YOUR family’s specific goals and timeline?”

The Bigger Picture: Why This Program Was Created

This program reflects a simple idea: giving young Americans an ownership stake in the economy early can transform how they think about money, investing, and wealth-building. The policy goals include expanding equity ownership across economic classes, supplementing Social Security with private savings, and creating what policymakers call a “shareholder economy.”

Whether this achieves its lofty policy goals remains to be seen—but for individual families, the opportunity to capture free seed capital and teach children about investing is very real and tangible.

Treasury officials emphasize these accounts are designed to supplement, not replace, Social Security and other safety net programs. The long-term vision is to empower a generation with real assets, investment experience, and an ownership mindset from day one.

How Gatewood Can Help

This program launches in mid-2026, which gives us time to think strategically together. Our process focuses on three essential questions:

Does your family qualify for the maximum benefits, including the Dell enhancement?

Should you contribute your own funds, or does a 529 or custodial account better serve your goals?

How does this fit into your broader wealth-building strategy for your children’s future?

We excel at these nuanced conversations—the kind where “it depends” actually becomes “here’s exactly what makes sense for you.” This isn’t about selling you on Trump Accounts. It’s about ensuring you make the most informed choice for your family’s unique situation.

Ready to discuss your family’s strategy?

Important Considerations

This program is new, and IRS regulations continue to evolve. The information provided here reflects program details as understood in December 2025, but specific rules and procedures may change as implementation progresses. Investment returns are not guaranteed, and tax laws may change. This material is educational and not a recommendation for any specific action.

For personalized guidance on whether Trump Accounts make sense for your family, we encourage you to consult with a financial advisor and tax professional who can evaluate your complete financial picture.

Important Disclosures

Securities and advisory services are offered through LPL Financial, a registered investment advisor and broker-dealer (member FINRA/SIPC).

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Gatewood and LPL Financial are separate entities. Gatewood Wealth Solutions does not provide legal or tax advice directly. However, Gatewood Tax & Accounting, a separate entity under the Gatewood family of companies, provides comprehensive tax planning and preparation services. For legal matters, you should consult your legal advisor regarding your personal situation. Our team coordinates closely with clients’ tax and legal professionals to help ensure comprehensive planning.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax.

This information is not intended to be a substitute for individualized tax advice. We suggest that you discuss your specific tax situation with a qualified tax advisor.

Prior to investing in a 529 Plan investors should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

In the financial world, there’s a certain type of advisor you want to avoid at all costs: the Fake Fiduciary. They might dress the part, speak the lingo, and even call themselves a “fiduciary,” but behind the scenes they’re stuck in the past—selfishly peddling high-commission products, hiding critical conflicts of interest, and prioritizing their paycheck over your best interests.

In the old days, commission-driven sales models were standard. But the industry has evolved and we are decisively in the modern era of true fiduciary financial advice. True fiduciary advisors aren’t selling a product; they’re delivering personalized advice, backed by a legal and ethical obligation to put the client’s interest first. Fake Fiduciaries? They’re still clinging to the sales playbook of the 1980s.

How to Spot a Fake Fiduciary

Follow the Money: Ask how they’re compensated. If commissions are a big part of the answer, red flag.

Check Transparency: A real fiduciary is open about fees, process, and conflicts of interest. No dodging allowed.

Listen to the Pitch: If it sounds more like a sales presentation than a strategy discussion, you know what you’re dealing with.

Check FINRA’s BrokerCheck and the SEC’s Investment Advisor Public Disclosure Website: Conduct a quick background check to look for red flags prior to trusting any advisor with your investments.

Trust Your Gut: If something on an instinctual level does not feel right, run! We have clients who were swindled by Bernie Madoff, who wish they had done so.

How Gatewood Does It Differently: The Fake Fiduciary Antidote

We’ve built Gatewood Wealth Solutions to be everything a Fake Fiduciary is not. Here’s how:

1. Industry-leading Fee Transparency

Our fee schedule is public, and we even provide a fee calculator so clients can see exactly what they’ll pay (HERE).

Our client app even shows the total fees paid for any time period our clients want to review.

2. Beyond the Legal Fiduciary Standard

We follow the highest ethical codes from the CFA Institute and CFP Board—not just the legal, contractual minimum.

3. Salaried Advisors

Our advisors are salaried, removing any incentive to sell products for personal gain.

We’ve built a career path from intern to partner that rewards long-term client care, not short-term sales wins.

4. Customized Investment Decisions

The Gatewood Investment Committee is agnostic to fund companies when selecting investments.

We receive no kickbacks and have no entangling alliances with any investment fund provider.

5. A Culture of Always Doing the Right Thing

Our guiding principle: always do the right thing.

This isn’t new—our founder’s early client letter to my own parents (prior even to my tenure with the firm) proves it’s been in our DNA from day one.

At Gatewood, we’re not just fiduciaries—we’re your long-term partners in building enduring wealth with purpose. No gimmicks, no hidden agendas, and no fake fiduciary practices.

In other words, at Gatewood, we’re the antidote to the Fake Fiduciary. We focus on transparency, ethics, and a client-first culture that ensures you’re always getting the best advice, free from hidden agendas. And that’s how we do things differently.

If you’re ready to experience the Gatewood way for yourself, we’d love to chat. We’re excited to show you what true fiduciary care looks like!

Important Disclosures:

Information and interactive calculators are made available to you as self-help tools for your independent use and are not intended to provide investment, tax, or legal advice. We cannot and do not guarantee their applicability or accuracy in regards to your individual circumstances. All examples are hypothetical and are for illustrative purposes. We encourage you to seek personalized advice from qualified professionals regarding all personal finance issues.

The 10 Reasons Why People Hire a Gatewood Advisor

When considering a financial advisor, clients typically interview just one or two firms. At Gatewood Wealth Solutions, we recognize the importance of making a lasting first impression that aligns with our clients’ core values and expectations. Inspired by insights from financial expert Michael Kitces and Morningstar’s 2023 study “Why Do People Hire Their Financial Advisors?”¹ we’ve refined the top ten reasons our clients choose Gatewood:

Emotional Drivers

Trust & Integrity

Trust forms the foundation of every advisory relationship. At Gatewood, we prioritize transparency and fiduciary responsibility, aiming to ensure our clients feel secure knowing we always place their best interests first.

“The values-driven team of Gatewood Wealth Solutions is motivated, caring, highly competent and personally fueled by character and integrity.” — Dave M., Corporate Executive

Clear and Consistent Communication

We simplify complex financial concepts and maintain proactive communication. Our advisors listen deeply and seek to ensure clients always understand and feel heard throughout their financial journey.

Relief from Financial Anxiety

Managing finances alone can be overwhelming. Gatewood advisors provide confidence by taking the burden of financial complexity off clients’ shoulders, guiding them confidently toward their goals.

“Their unwavering support made a world of difference during such a challenging time. I am profoundly grateful for all they’ve done and continue to do for me.” — Carol S., Corporate Executive 09.20.23*

Financial Expertise

Personalized Investment Guidance

Gatewood offers customized investment advice meticulously aligned with our clients’ long-term objectives, so that decisions are based solely on clients’ best interests and not outside incentives.

“Gatewood Wealth Solutions gives me confidence that my retirement savings are being monitored and managed with MY best interest in mind.” — Gary B., Corporate Executive 09.27.23*

Specialized Problem-Solving

Our advisors are equipped to handle specific financial challenges such as tax optimization, retirement income planning, and estate management. We tailor each solution to address unique client circumstances effectively.

“Their planning services are comprehensive and consider all assets of our family, not just what they manage.” — Tim M., Partner/Attorney 09.22.23*

Proactive Strategic Planning

Life changes rapidly, and Gatewood advisors remain ahead of market cycles, income variations, and unexpected life events, proactively preparing clients to navigate and capitalize on these changes.

Situational Advantages

Personalized, Holistic Financial Plans

At Gatewood, financial planning extends beyond just numbers. We integrate our clients’ personal values, life stages, and aspirations into comprehensive strategies that align financial decisions with life goals.

“The Gatewood team developed an integrated financial and retirement plan that we refined together. I’m pleased to say we are well ahead on our plan!” — Phil P., Retired Corporate Executive 09.20.23*

Local Accessibility and Engagement

With our established presence in St. Louis, Gatewood clients benefit from direct access and face-to-face interactions. Our local roots and active community involvement offer reassurance and familiarity. For clients in the 30+ states outside of the St. Louis Metro Area, we frequently travel for in-person visits.

Tangible Quick Wins

We demonstrate value early by providing immediate, actionable insights and measurable results. Gatewood clients frequently experience beneficial outcomes quickly, reinforcing their decision to partner with us.

Real-Life Client Success Stories

Prospective clients appreciate authentic stories from those who’ve experienced our commitment firsthand. At Gatewood, we regularly share testimonials and case studies illustrating our dedication to client success, fostering confidence before the relationship even begins.

“As Pam and I navigate these retiring years, she and I both derive a rich sense of security knowing that John and the team at Gatewood Wealth Solutions will continue to surround and support her for as long as needed.” — Steve K., Retired Corporate Executive 09.27.23*

At Gatewood Wealth Solutions, our advisors may not address every potential motivator—but we passionately deliver on the ones that align most closely with our clients’ values: trust, clear communication, personalized strategies, and local, accessible expertise. These core areas define why our clients not only choose us initially but remain committed partners for life.

Sources:

¹Morningstar 2023, “Why Do People Hire Their Financial Advisors?” via Kitces

Important Disclosures:

*The statements provided are testimonials by clients of the financial professional as of 7/22/2025. The clients listed have not been paid or received any other compensation for making these statements. As a result, the client does not receive any material incentives or benefits for providing the testimonial. These views may not be representative of the views of other clients and are not indicative of future performance or success.

There’s a glaring contradiction in today’s economic discourse, and it clouds the investment outlook. The loudest voices warning about America’s unsustainable federal deficit are often the most reflexive critics of tariffs, an essential tool that could help address the crisis. They demand “fiscal responsibility” but fall silent when asked what they’d cut from the budget. Suggest entitlement reform, and they’ll tell you it’s political suicide. Propose higher income taxes, and they bristle at the economic drag. Ask how they’d raise $2.0 to $2.8 trillion annually to close the federal budget gap, and the conversation ends.

That’s why tariffs—unfashionable, imperfect, and deeply misunderstood—may be one of the only practical tools left that can meaningfully address the deficit until the country is ready for major changes to how the government collects revenue and spends.

D.O.G.E. Promised a Trillion-Dollar Fix. It Delivered a Rounding Error.

The Department of Government Efficiency (D.O.G.E.) was supposed to be the bold solution to government waste. Originally pitched as a vehicle for cutting $1 trillion in inefficiencies, the agency—backed by Elon Musk and restructured under President Trump—quickly revised expectations downward to $150 billion. D.O.G.E. operates as a consultant would, examining costs and structure and recommending changes to achieve efficiencies across various departments.

D.O.G.E. impact is a subject of some debate. As of mid-2025, D.O.G.E. has claimed between $150 billion and $ 90 billion in savings, although independent audits dispute much of that figure. More troubling, aggressive cuts to revenue-generating agencies like the IRS reduced government income. By some estimates, DOGE’s efforts may have cost taxpayers $135 billion through re-hires, overtime, legal settlements, and lost tax collections.

While well-intentioned and fundamentally a good idea, the shortfall was a strategic failure that exposed the limits of the “cut spending” approach. D.O.G.E. aimed to trim fat but ended up delivering a rounding error instead of transformational change.

Growth Alone Won’t Save Us

With a less-than-spectacular D.O.G.E. impact, and large Government spending cuts off the table — at least for now — the bipartisan default in Washington has long been to grow the economy and let increased tax receipts shrink the deficit as a percentage of GDP over time. It’s an appealing theory that consistently fails in practice. Despite periods of strong GDP growth, federal spending continues to outpace revenue by unprecedented margins.

While the growth strategy is politically palatable and will help over time, the U.S.’s current fiscal situation, with annual deficits of over $2 trillion, is dire. We don’t have the luxury of waiting for growth to solve a crisis that compounds daily. Growth matters, but it’s not enough. We need substantial revenue, and we need it soon.

Understanding Tariffs: A Tax, Not Inflation

Let’s address the elephant in the room: tariffs are, in fact, a tax. But they are emphatically not inflation.

Inflation is a monetary phenomenon—the expansion of the money supply that dilutes currency value and drives broad-based price increases. Tariffs don’t expand the money supply or devalue the dollar. They are a targeted consumption tax applied to imported goods, with three key differences from domestic taxes:

Revenue generation: Unlike inflation, tariffs generate federal government revenue, potentially $300 billion annually

Targeted impact: They affect specific imported goods rather than the entire economy. Imports are roughly 15% of the U.S.’s GDP today.

Importer and Corporate absorption possibility: Who absorbs the cost increase from U.S. tariffs is an interesting and complex question, with the absorbing party differing by item and by importer. With energy costs roughly 10% lower than two years ago, many corporations have absorbed most of the tariff costs rather than passing them through

Despite persistent warnings from economists, tariffs have not triggered the runaway inflation they predicted.

The Hidden Costs of Corporate Absorption

However, when corporations absorb tariff costs, the economic impact doesn’t simply disappear—it gets redistributed. Companies facing compressed profit margins from tariff absorption experience a cascade of effects that ultimately flow back to the broader economy:

Reduced profit margins lead to lower corporate earnings, which translate to decreased stock valuations. This creates a diminished wealth effect as portfolio values decline, prompting consumers to reduce spending. Meanwhile, lower capital gains tax revenue partially offsets the government’s gains in tariff income.

This redistribution means that while tariffs may not be directly reflected in consumer prices, their costs still flow through the economy via financial markets and reduced economic activity.

The Regressive Reality of “Targeted” Impact

While tariffs don’t affect every sector equally, describing their impact as merely “targeted” obscures an important truth: if passed through, they disproportionately burden lower-income households. These families spend a higher percentage of their income on goods (versus services), have less flexibility to substitute away from imported products, and are more price-sensitive to increases in everyday items.

This regressive effect means that tariffs could function as a consumption tax that hits hardest those least able to absorb the cost—a significant trade-off that must be weighed against their revenue-generating potential. Kitchen table economics won 2024 for the Republicans, but it could be the reason they lose the 2026 midterm elections.

Why Income Tax Hikes Hit a Wall

One truism of taxes: Anything you tax, you get less of. That reflects human behavior and rational economic actors. Raising income taxes sounds straightforward until you encounter the Laffer Curve’s hard ceiling. Beyond a certain point, higher rates reduce total tax revenue by discouraging work, saving, and investment. Historical data suggests we may already be approaching that point, considering total income taxes collected rose when Trump dropped rates in his first administration.

The federal government’s share of GDP rarely exceeds 20%, regardless of marginal tax rates. Taxing productivity has diminishing returns and penalizes the very economic activity we need to encourage. Tariffs, conversely, are harder to avoid and don’t punish domestic output. For revenue generation with minimal collateral damage to productivity, tariffs offer a superior approach, though they come with their own distributional consequences.

Tariffs as Statecraft: Economic Leverage Without Bloodshed

One of tariffs’ most under appreciated benefits is their geopolitical utility. Unlike sanctions or military action, tariffs exert pressure with fewer human costs and less international conflict.

Consider Canada’s Digital Services Tax proposal earlier this year, which targeted U.S. tech firms. The Trump campaign’s swift threat of retaliatory tariffs prompted Canada to reverse course within days. No troops, no diplomatic standoff—just credible economic pressure accomplishing what traditional diplomacy might have taken months to achieve.