Much has changed since then. Tax filing season opened on January 26th, more than three million families have now signed up, a Super Bowl ad ran during the pregame broadcast, President Trump promoted the accounts during his State of the Union address on February 24th and directed the nation to trumpaccounts.gov, and a new online sign-up option just launched.

Here’s our refreshed take on what this program means for your family.

The Basics: What Are Trump Accounts?

Trump Accounts, formally known as 530A Accounts under the One Big Beautiful Bill Act, are a new type of individual retirement account designed specifically for children. They’re custodial in nature, meaning a parent or guardian controls the account until the child turns 18.

How the Trump Accounts Actually Work

Eligibility: Any U.S. citizen under age 18 with a valid Social Security number can have an account opened on their behalf. Each child may have only one Trump Account.

Account Benefits

The $1,000 Seed: Children born between January 1, 2025 and December 31, 2028 who are U.S. citizens are eligible for a one-time $1,000 pilot program contribution from the U.S. Treasury. This deposit is expected no earlier than July 4, 2026.

Annual Contributions: Families, employers, and others may contribute up to a combined $5,000 per child per year. Employers may contribute up to $2,500 (per employee) of that amount under Section 128 as a fringe benefit. The $5,000 limit will be adjusted for inflation starting in 2027. No earned income is required, and contributions don’t affect traditional or Roth IRA limits for the contributor.

Account Limitations

Charitable & Government Contributions: Qualified general contributions from government entities and 501(c)(3) organizations do not count against the $5,000 annual limit. These are separate and additive.

Investment Rules: All funds must be invested in low-cost, broad U.S. equity index funds or ETFs tracking qualified indexes such as the S&P 500. Annual fees are capped at 0.10% (10 basis points), and no leverage is permitted.

No Withdrawals Before 18: Generally, no distributions may be made before the year the child turns 18, with very limited exceptions for death, excess contributions, and certain rollovers.

What’s New About Trump Accounts Since December

1. Tax Season Sign-Ups Are Live

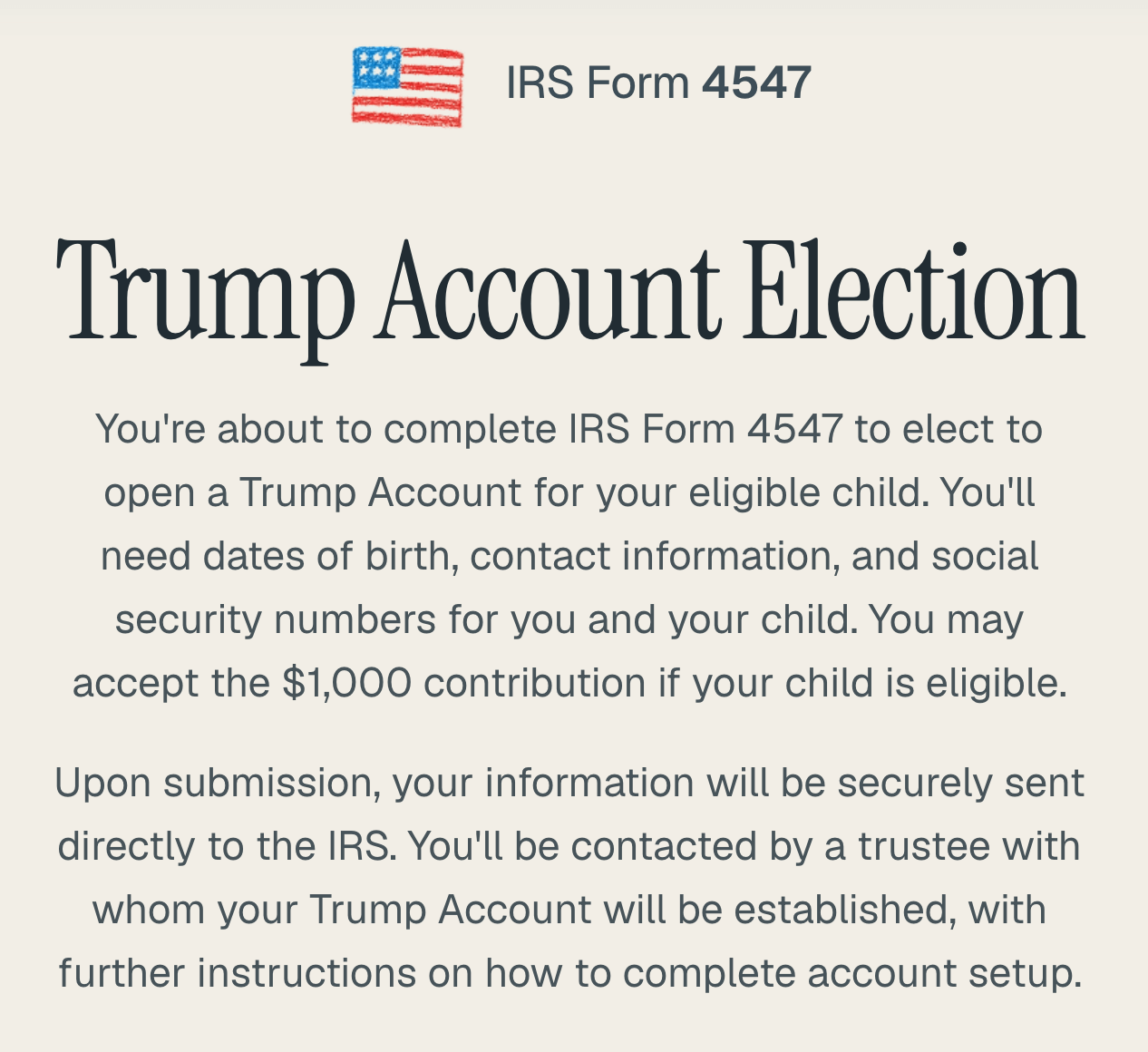

As of January 27, 2026, families can elect to open Trump Accounts by filing IRS Form 4547 with their 2025 federal tax return. The form includes two elections: one to open the account and one to request the $1,000 pilot program contribution (if eligible).

The form accommodates up to two children and families with more eligible children can attach additional copies. Filing electronically with your tax return is the fastest and easiest method.

2. New Online Sign-Up Option

Following the Invest America Super Bowl ad last weekend, a new online sign-up form launched at trumpaccounts.gov, ahead of the originally planned mid-2026 timeline. This gives families a second pathway to open accounts outside of the tax filing process. Here’s what the sign-up experience looks like:

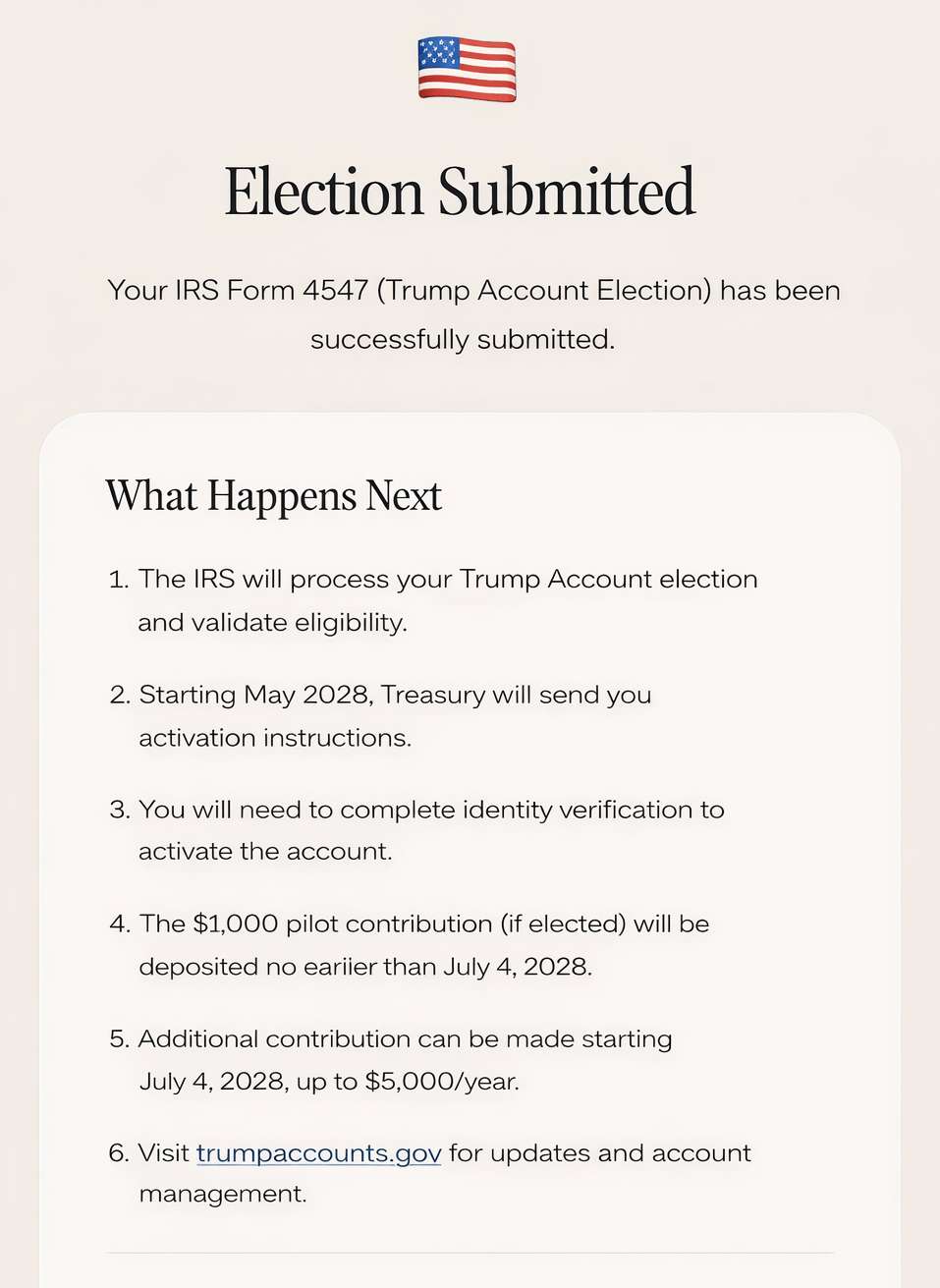

The Form 4547 election page at trumpaccounts.govConfirmation and next steps after submission

3. Over Three Million Families Have Enrolled

According to the White House, more than three million families had signed up as of the State of the Union address on February 24th. That milestone was up from one million just five days into tax filing season, and Treasury Secretary Scott Bessent noted that approximately 500,000 elections were made in the first three days alone. During the speech, President Trump called the program “something that’s so special” that has “taken off and gone through the roof,” and directed the nation to sign up at trumpaccounts.gov.

4. Activation Timeline

After filing Form 4547, the Treasury Department will contact parents starting in May 2026 to complete an identity verification process and activate accounts. You’ll be contacted by the partner financial firm where your Trump Account will be held with further instructions. Contributions and seed deposits will begin on July 4, 2026.

5. The Dell Foundation Gift

Michael and Susan Dell have pledged $6.25 billion to seed accounts for approximately 25 million children who missed the eligibility cutoff for the $1,000 federal deposit. Their gift provides $250 per eligible child. To qualify for the Dell contribution, children must be age 10 or under, born before January 1, 2025, and live in ZIP codes where the median household income is below $150,000. This is expected to reach children across roughly 75% of U.S. ZIP codes.

An important clarification: The Dell gift goes to a different population than the Treasury’s $1,000. It is not $250 on top of $1,000. Children born 2025 through 2028 receive the $1,000 government seed. Children born before 2025 who are age 10 and under may receive the $250 Dell contribution. Both groups benefit, but through separate funding streams.

6. Growing Employer and Corporate Support

A growing list of major U.S. corporations have pledged matching deposits or contributions for employees. Venture capitalist Brad Gerstner has also pledged $250 for each child under five with a Trump Account in Indiana. We expect this trend of employer and philanthropic participation to continue expanding.

How the Tax Treatment Works

Understanding the tax treatment matters because it affects whether you should add your own money to these accounts or use other vehicles instead.

Think of it in two phases:

PHASE 1: Before Age 18 (The Accumulation Phase)

During childhood, contributions are made with after-tax dollars, and investment growth accumulates tax-deferred. Parents or guardians maintain control of the account during this period. This phase is straightforward.

PHASE 2: After Age 18 (The IRA Conversion Phase)

At age 18, Trump Accounts automatically convert to traditional IRAs. This conversion fundamentally changes how the account functions:

What Changes on Trump Accounts for Those Over 18?

Access and Control: The young adult gains full control as the account becomes a traditional IRA in their name.

Withdrawals and Taxes: This is where it gets important. Distributions are taxed as ordinary income on all earnings and growth (though your original contributions come back tax-free). Additionally, the 10% early withdrawal penalty applies to distributions before age 59½.

The Exception Rules:

The 10% penalty (not the taxes) can be waived for:

First-time home purchases (up to $10,000)

Qualified education expenses

Business startup costs in certain circumstances

Here’s the crucial point many families miss: These “qualified expenses” only waive the 10% penalty—they do NOT eliminate the ordinary income tax on the earnings. Even when funding college or buying a first home, you’ll owe income tax on all the growth.

Investment Flexibility: After conversion, the account can be invested more broadly according to traditional IRA rules, no longer restricted to designated index funds.

Why This Matters: This automatic conversion to a traditional IRA means families should carefully consider whether contributing their own funds makes sense compared to other savings vehicles like 529 plans (where qualified education withdrawals are completely tax-free) or custodial accounts (where flexibility is greater).

Our General Perspective on Trump Accounts

Accept the free money. If your child qualifies for the $1,000 Treasury seed or the $250 Dell contribution, opening an account is straightforward. You’re accepting a gift with no cost to you. We’d help every eligible family capture this benefit. The Treasury projects that the $1,000 seed alone could grow to roughly $6,000 by age 18, $15,000 by age 27, or over $243,000 by age 55, assuming historical market returns.

Think carefully about your own contributions. For most families whose primary goal is funding education, 529 plans still deliver better tax outcomes. A 529 offers completely tax-free growth potential and withdrawals for qualified education expenses. Trump Accounts tax all growth as ordinary income at withdrawal, even for education. That’s a meaningful difference.

When Trump Accounts Make Sense for Your Plan

That said, Trump Accounts can make sense when:

You’re already maximizing 529 contributions and want additional tax-advantaged savings

Your priority is very long-term wealth building, with retirement savings starting at birth

You’re targeting a first home down payment for your child

Your employer is offering matching contributions, which is additional free money worth capturing

You want to diversify across savings vehicles with different tax treatments

Check with your employer. A growing number of companies are pledging contributions to Trump Accounts as an employee benefit. If your employer is participating, that’s money you don’t want to leave on the table, similar to a 401(k) match.

Action Steps for Families

File Form 4547 with your 2025 tax return. This is the fastest way to open an account and elect the $1,000 pilot program contribution for eligible children. You can also sign up online at trumpaccounts.gov now.

Check your employer’s plans. Ask your HR or benefits team whether your company is making Trump Account contributions under Section 128.

Don’t rush your own contributions. Contributions won’t be accepted until July 4. Use this time to evaluate whether a Trump Account, 529 plan, or combination makes the most sense for your family’s goals.

Keep records. Documentation of contribution sources matters for future distribution taxes and rollover reporting. Start organized from day one.

How Gatewood Can Help You Analyze Trump Accounts

This program launches on July 4, which gives us time to plan strategically together. The questions we help families answer are straightforward but important:

Does your family qualify for the maximum benefits?

Should you contribute your own funds, or does a 529 or custodial account better serve your goals?

And how does this fit into your broader wealth-building strategy?

We specialize in exactly these conversations, the kind where “it depends” actually becomes “here’s exactly what makes sense for you.” We’re fiduciary advisors, so this isn’t about selling you on Trump Accounts. It’s about helping you make the most informed choice for your family’s specific circumstances.

Ready to discuss strategy?

Important Considerations

This program is new, and IRS regulations continue to evolve. The information provided here reflects program details as understood in December 2025, but specific rules and procedures may change as implementation progresses. Investment returns are not guaranteed, and tax laws may change. This material is educational and not a recommendation for any specific action.

For personalized guidance on whether Trump Accounts make sense for your family, we encourage you to consult with a financial advisor and tax professional who can evaluate your complete financial picture.

Important Disclosures

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. Gatewood Wealth Solutions and LPL Financial do not provide legal or tax advice or services.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Prior to investing in a 529 Plan investors should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

What is the biggest risk you face in retirement? If you said the stock market, you are not alone. Most retirees point to market volatility as the thing that keeps them up at night. A bad quarter. A correction. A bear market that arrives at the worst possible time. Those fears are real, and they are understandable.

But what if the biggest risk is not the one that makes headlines? What if it is the one that never makes a sound?

Volatility is the risk you can see. Inflation is the risk you can feel.

A market downturn is dramatic. It shows up on the news, in your quarterly statement, and in conversations at dinner parties. But inflation works differently. It does not announce itself. It does not send a notification. It simply makes everything around you a little more expensive, year after year, until the retirement you planned for costs far more than you expected. And by the time most people notice, the damage is already done.

This is not a theoretical concern. If the last few years have taught us anything, it is that inflation is not a relic of the 1970s. It is here, it is real, and it affects every family planning for or living in retirement. Between 2021 and 2023, Americans experienced the sharpest rise in consumer prices in over four decades. Grocery bills surged. Healthcare costs climbed. Energy prices spiked. And for retirees living on a fixed income, every one of those increases landed harder than it did for someone still receiving annual raises at work.

The question is not whether inflation will affect your retirement. It is whether your plan accounts for it.

What Inflation Actually Does to Your Money

Inflation is often described as the rate at which prices rise. But for a retiree, a more useful definition is this: inflation is the rate at which your money loses its ability to support your life.

Think of your retirement savings as a block of ice on a warm day. You can see the block. You can measure it. It looks solid. But the moment you set it outside, it begins to shrink. Not quickly. Not dramatically. But steadily and relentlessly. Inflation works the same way. Your account balance may look the same on paper, but its ability to buy the things you need is slowly melting away.

Consider what everyday costs looked like just 20 years ago. In 2005, a gallon of milk cost about $3.20. Today, that same gallon runs about $4.05. A movie ticket was $6.41. Today, the average is closer to $11. A first-class postage stamp cost $0.37. Today, it is $0.73, nearly double. These are not luxury items. These are the ordinary costs of living.

Now multiply that pattern across everything a retiree spends money on: groceries, utilities, property taxes, home maintenance, insurance, travel, and especially healthcare. Healthcare costs have risen more than 120% since 2000, consistently outpacing overall inflation. For retirees who spend a larger share of their income on medical care, the effective rate of inflation they experience is often significantly higher than the headline number.

Your grocery bill does not care what the CPI says. It charges you what it charges you.

And that headline number, the one you hear on the news, is itself misleading. The Consumer Price Index is an average across all consumers. It weighs housing, transportation, food, healthcare, and dozens of other categories into a single number.

But retirees do not spend like the average consumer. They spend disproportionately more on healthcare, which has been rising at 5% to 6% per year. They spend more on housing maintenance, insurance, and prescription drugs. Less on gas for a daily commute. Less on work clothing. The official inflation rate might say 3%. But the inflation a retiree actually experiences at the checkout counter, at the pharmacy, and at the doctor’s office can be 4%, 5%, or higher.

Headline inflation is a national average. Your inflation is personal. And for most retirees, it is higher than the number they see on the evening news. This gap between the reported rate and the rate you actually live with is one of the most underestimated risks in all of retirement planning.

The Raise You No Longer Get

Here is something most people never think about until it is too late: for your entire working career, you had a built-in defense against inflation. It was called a raise.

Every year or two, your salary went up. Maybe it was a cost-of-living adjustment. Maybe it was a promotion. Maybe it was a new job with a higher offer. Whatever the reason, your income was quietly rising alongside the cost of living. You may not have even noticed inflation during those years because your paycheck was keeping pace. The groceries cost more, but you were earning more. The insurance premiums went up, but so did your bonus. The escalator was carrying you upward, and you barely had to think about it.

The moment you retire, that escalator stops.

Your income becomes fixed. Your expenses do not.

Now you are taking the stairs. Every price increase you encounter, at the grocery store, at the pharmacy, on your insurance bill, comes directly out of your purchasing power with no offsetting raise to absorb it. The inflation that was invisible during your working years suddenly becomes very visible, because there is no longer an automatic mechanism to counteract it.

This is one of the most jarring transitions in retirement, and one of the least discussed. People plan for the loss of a paycheck. They plan for the shift from saving to spending. But very few plan for the loss of the annual raise that was silently protecting them from inflation their entire adult lives.

Think of it like running on a moving sidewalk at the airport. You feel like you are keeping a comfortable pace, but the belt beneath your feet is doing half the work. The moment you step off that belt and onto the regular floor, you realize how much effort it actually takes to maintain the same speed. Retirement is the moment you step off the belt. Inflation is the distance you now have to cover on your own.

You do not feel inflation when your income is rising. You feel every bit of it when your income stops.

The 20-Year and 30-Year Reality: What Retirement Actually Costs

Here is where the math becomes personal.

Meet Richard and Diane. Both are 65 and just retired. Their annual living expenses are $100,000. They feel comfortable. Their savings are solid. Their Social Security is in place. They believe they have enough.

But have Richard and Diane considered what their life costs at 85? What about at 95?

At an average inflation rate of just 3% per year, which is close to the long-term historical average, here is what happens to their purchasing power:

Year

Age

Annual Cost of the Same Lifestyle

Purchasing Power of Original $100,000

Today

65

$100,000

$100,000

Year 10

75

$134,400

$74,400

Year 20

85

$180,600

$55,400

Year 30

95

$242,700

$41,200

*Assumes 3% average annual inflation. Figures are approximate and for illustrative purposes only.

Read that last row again. If Richard and Diane live to 95, their $100,000 lifestyle will cost nearly $243,000 per year just to maintain the same standard of living. And if they did nothing to grow their savings, the purchasing power of every dollar they set aside would be worth less than 42 cents.

Their account balance did not shrink. Their life just got more expensive around it.

And this assumes a 3% rate. Healthcare inflation has historically averaged closer to 5% to 6%. For retirees whose medical costs represent a growing share of their budget with each passing year, the erosion is even steeper.

This is not a hypothetical exercise. People are living longer. A healthy 65-year-old couple today has a reasonable probability that at least one of them will live past 90. A 30-year retirement is no longer an outlier. It is a planning reality. And that means inflation is not a short-term nuisance. It is a structural force that your portfolio must be designed to outpace.

The Social Security “Raise” That Doesn’t Keep Up

At this point, many retirees will say, “But my Social Security is adjusted for inflation. I get a cost-of-living increase every year.”

That is true. Social Security provides an annual cost-of-living adjustment, known as the COLA. And on the surface, it sounds like the perfect protection. Prices go up, your benefit goes up. Problem solved.

Except the COLA is not calibrated to your life.

The Social Security COLA is based on a measure called the CPI-W, which tracks inflation for urban wage earners and clerical workers. Not retirees. Wage earners. That index reflects the spending patterns of someone still working: commuting costs, work clothing, lunches out, childcare. It underweights the categories that dominate a retiree’s budget, particularly healthcare, prescription drugs, supplemental insurance, and long-term care.

So what does this mean in practice? In a year where the COLA gives you a 2.8% increase, your actual cost of living may have risen 4% or 5% because your healthcare premiums climbed, your prescription costs increased, and your Medicare Part B went up more than the general index. You received a raise. It just was not big enough.

Every year the COLA falls short, the gap compounds. And it never catches up.

Think of it like a roof with a slow leak. Each year, a little more water gets in. In year one, you barely notice. By year five, there is a stain on the ceiling. By year fifteen, the damage is structural. The COLA is patching the roof every January, but it is using a patch that is slightly too small. Over a 20- or 30-year retirement, the cumulative shortfall between what your COLA covers and what your life actually costs can amount to tens of thousands of dollars in lost purchasing power.

This is not a flaw in Social Security. The program does what it was designed to do. But it was never designed to be your sole defense against inflation. It was designed to be a floor, not a ceiling. The rest of the protection has to come from your investment portfolio, your withdrawal strategy, and the planning that ties them together.

If your plan assumes the COLA fully protects you from inflation, your plan has a gap. And that gap gets wider every year you are in retirement.

The Conservation Trap: Why Playing It Safe Can Be the Riskiest Move

Here is where the well-meaning instinct of most retirees can actually work against them.

Meet Carol. Carol just retired at 65 with $1.2 million in savings. She worked hard for that money. She watched it grow over decades. And now that she has crossed the finish line into retirement, her first instinct is to preserve it. She tells her advisor, “I don’t want to lose what I’ve built. Let’s move everything into something safe.”

It is a natural reaction. After a career of accumulating, the shift to spending feels vulnerable. The idea of a market decline wiping out years of savings is terrifying. So, Carol moves heavily into bonds, CDs, and money market funds. She feels confident.

But is Carol’s money actually less vulnerable?

If Carol’s “less vulnerable” portfolio earns 3% to 4% per year, and inflation averages 3%, her real return, the growth that actually matters, is close to zero. She is running on a treadmill. Her balance may hold steady, but its ability to fund her life is declining every single year. In 20 years, her $1.2 million buys what $660,000 buys today. In 30 years, it buys what $490,000 buys today.

Preservation of principal is not the same thing as preservation of purchasing power.

This is the distinction that changes everything. The goal of retirement investing is not to keep your account balance from going down. The goal is to make sure your money can still support your life five, ten, twenty, and thirty years from now. A portfolio that never declines but never grows in real terms is not less vulnerable. It is slowly failing.

Think of it this way. If you put food in the freezer to preserve it, the food looks the same. The weight is the same. The packaging is intact. But if the freezer is slowly losing power, the food is spoiling from the inside out. By the time you open it years later, what looked preserved is no longer usable. That is what inflation does to a portfolio that is not built to grow.

The real risk in retirement is not a bad quarter in the stock market. It is a quiet decade of falling behind.

The Tax Toll: Why Your Returns Are Smaller Than You Think

If the inflation conversation stopped here, it would be concerning enough. But there is another force working against your purchasing power that makes the math even more difficult: taxes.

When you hear that a conservative portfolio returned 4% to 5% last year, that number is pre-tax. But inflation does not charge you pre-tax prices. Every gallon of milk, every doctor’s visit, every utility bill, every property tax payment is made with after-tax dollars. The cost of living is an after-tax reality. And that mismatch is where many retirees quietly fall behind.

Let us walk through the math. Suppose your portfolio earns 5% in a given year. Depending on the type of account and the nature of the income, whether it is ordinary income from bonds or a traditional IRA distribution, or capital gains from a taxable brokerage account, you may owe 15% to 30% or more in federal and state taxes on those gains. At a 25% effective tax rate, your 5% return becomes 3.75% after taxes. Now subtract inflation at 3%. Your real, after-tax return is 0.75%.

Less than one percent. That is what you actually kept.

And remember, that 3% inflation figure is the headline number. If your personal inflation rate is closer to 4% or 5% because of healthcare costs, your real after-tax return may be zero. Or negative. You earned a positive return on your statement, paid taxes on it, and still lost ground to the cost of living.

Think of it like a tollway. Your investment returns are driving toward your wallet. But before they arrive, they have to pass through a tax tollbooth. A portion of every dollar is collected before it ever reaches you. Meanwhile, inflation is raising the prices at your destination at the full rate, no tollbooth, no discount, no deduction. The prices you pay at the grocery store, the pharmacy, and the gas station are not reduced because you paid taxes on your investment gains. Inflation charges full fare on the other side of the toll.

Your returns are taxed. Inflation is not. That asymmetry is one of the most overlooked realities in retirement planning. It means that a portfolio earning 4% to 5% before taxes, which sounds reasonable, may only deliver 2% to 3.5% after taxes. And when you subtract real-world inflation at 3% to 5%, you are left with a razor-thin margin, or worse, you are going backward.

This is precisely why keeping up with inflation requires more than a conservative portfolio.

You need the type of growth that equities provide, and you need a strategy that manages your tax exposure along the way. Roth conversions, tax-efficient withdrawal sequencing, asset location across taxable, tax-deferred, and tax-free accounts: these are not optional add-ons. They are essential tools for making sure more of your return actually reaches your purchasing power.

It is not what your portfolio earns that matters. It is what you get to keep after taxes, after inflation, after life.

Why Equities Still Matter After You Retire

If inflation is the disease, then equities are the long-term medicine.

Historically, stocks have been the only asset class that has consistently outpaced inflation over extended periods. Bonds provide balance. Cash provides liquidity. But neither has the growth engine necessary to keep your purchasing power intact over a 20- or 30-year retirement.

This does not mean a retiree should have 100% of their portfolio in stocks. It means that having too little in equities may actually be more dangerous than having too much, especially when the retirement could last three decades.

Here is the tension most retirees face: they understand, at least intellectually, that they need growth. But when the market drops 15% or 20%, the emotional response is overwhelming. They want to sell. They want to move to cash. They want to make the pain stop. And if their advisor has not built a strategy to manage that emotional reality, the client often makes the worst possible decision at the worst possible time.

You cannot outrun inflation from the sideline. You have to stay in the game.

So how do you stay invested in equities, which you need for long-term growth, while also preserving your assets from the short-term volatility that makes equities so difficult to hold? How do you keep your foot on the gas and still feel confident?

At Gatewood Wealth Solutions, this is exactly the problem our cash strategy was designed to solve.

Bear Market Ready, Bull Market Positioned: How Our Cash Strategy Works

Most advisors and institutions approach retirement investing with a simple formula: as you get older, shift more of your portfolio into bonds and cash. The thinking is simple. Less volatility equals less risk. And for many firms, the standard recommendation is something like a 60/40 or even 50/50 stock-to-bond allocation by the time you reach retirement.

But we believe this conventional approach misidentifies the risk. It focuses on reducing volatility when the real enemy is inflation. The result? Portfolios that feel comfortable but do not grow fast enough to keep up with the rising cost of life.

At Gatewood, we take a different approach. We call it being “Bear Market Ready, but Bull Market Positioned.” The foundation of this strategy is our Cash Target.

Here is how it works. Rather than shifting large portions of a retiree’s portfolio into bonds simply because they have reached a certain age, we calculate a precise amount of cash that each client should hold in a dedicated cash reserve. This Cash Target is based on the client’s actual monthly expenses, their income sources like Social Security and pensions, and our Investment Committee’s current assessment of market conditions.

The purpose of this cash reserve is simple but powerful: it provides the income a client needs to live on for a defined period of time, regardless of what the stock market is doing. If the market enters a downturn, we draw from the cash reserve rather than selling investments at depressed prices. This gives the invested portion of the portfolio time to recover without being raided during a decline.

Cash buys you time. Time allows your investments to recover. Recovery preserves your purchasing power.

Think of it like a water tower for a community. On a normal day, water flows from the main supply and the tower stays full. But when the main supply is interrupted, whether by a storm or a maintenance issue, the water tower provides steady, reliable service until the supply comes back online. No one panics. No one goes without water. The reserve does its job, and life continues normally.

That is exactly what the cash reserve does for our clients. It is their water tower. When the market is strong, we replenish it. When the market declines, we draw from it. And because our clients know they have this buffer, they have the confidence to remain invested in equities at higher levels than they might otherwise tolerate.

This is the key insight: the cash strategy is not about the cash itself. It is about what the cash allows you to keep invested. By separating the money that you need in the short term from the money that needs to grow over the long term, we give clients the confidence they need emotionally and the growth they need financially.

How This Strategy Preserves Purchasing Power Over Decades

Let us return to Carol, the retiree who wanted to “play it safe.” What would her retirement look like under two different approaches?

Scenario A: The conventional approach. Carol moves to a conservative 40% stock, 60% bond allocation. Her portfolio grows at roughly 4% to 5% per year before taxes. After taxes and inflation, her real return is near zero, or possibly negative in years when healthcare costs spike. Over 25 years, her purchasing power slowly deteriorates. By 85, she is making difficult choices about healthcare, travel, and the lifestyle she planned for. By 90, she is drawing down principal faster than she expected. Her statement looked less vulnerable. Her life did not feel less vulnerable.

Scenario B: The Gatewood approach. Carol maintains a higher equity allocation, perhaps 65% to 75% in stocks, because she has a cash reserve covering 12 to 24 months of living expenses. Her portfolio grows at 7% to 8% over time. With tax-efficient strategies like Roth conversions, strategic withdrawal sequencing, and thoughtful asset location, more of that return actually reaches her wallet. After taxes and inflation, her real return is meaningfully positive. When the market dips, she draws from her cash reserve instead of selling stocks at a loss. When the market recovers, she replenishes the reserve. Over 25 years, her portfolio has not just survived inflation and taxes. It has outpaced them. She is living the same lifestyle at 90 that she planned at 65.

Same starting balance. Same retirement. Vastly different outcomes.

The difference is not luck. It is structure. Carol’s portfolio in Scenario B was designed to grow because the cash strategy removed the pressure to sell during downturns. She did not need to become less invested as she aged. She needed to become more intentional about how her money was organized.

Think of it like a home with a well-stocked pantry. If you know you have three months of food in the house, a winter storm does not send you into a panic. You do not rush to the store in dangerous conditions. You wait. You are prepared. And when the storm passes, you resupply calmly, on your terms. That is the emotional and financial freedom our cash strategy creates.

Inflation Is Not Just Your Problem. It Is a Family Problem.

When we talk about inflation eroding purchasing power, we are not just talking about one person’s retirement. We are talking about the ripple effects that reach across an entire family.

When a retiree’s savings cannot keep up with the cost of living, the burden often shifts.

Adult children step in to help with medical bills, home repairs, or daily expenses. Family vacations get scaled back or canceled. Inheritances that were intended to provide a head start for the next generation shrink or disappear entirely. The financial strain does not stay contained. It radiates outward.

Inflation does not just affect your retirement. It affects your family’s future.

This is why at Gatewood, we think about inflation through the lens of our Firm-to-Family™ approach. When we build a plan, we are not just asking whether your money will last until age 90. We are asking whether your plan preserves the financial independence that allows you to live on your terms, support the people you love, and leave the legacy you intended. Inflation threatens all of it. Your investment strategy must account for all of it.

What You Can Do About It

Inflation may be beyond your control, but your response to it is not. Here are the questions every retiree and pre-retiree should be asking:

Is my portfolio built to grow, or just to survive? If your investments are primarily in bonds, CDs, and money market funds, your portfolio may be falling behind inflation every year. Ask your advisor what your real return has been after accounting for inflation.

Do I have a cash strategy that allows me to stay invested? If a market downturn would force you to sell stocks to pay your bills, your portfolio is not structured properly. A dedicated cash reserve gives you the freedom to weather short-term volatility without sacrificing long-term growth potential.

Have I stress-tested my plan for a 30-year retirement? Many financial plans are modeled for 20 years. But if you are 65 and healthy, planning to age 85 may not be enough. Ask to see what your plan looks like at 90 and 95 with varying inflation assumptions.

Am I thinking about inflation as a fixed number, or as a category-by-category reality? Healthcare inflation runs significantly higher than general inflation. If medical costs are a growing part of your budget, your effective inflation rate may be 4% or 5%, not the 2.5% to 3% headline number.

Is my advisor managing for preservation of principal, or preservation of purchasing power? There is a significant difference. One preserves the number on your statement. The other preserves the life that number is supposed to fund.

Ask the right question, and the right strategy follows.

Wealth Is Personal. So Is Inflation.

At Gatewood Wealth Solutions, we believe that wealth is personal. Your retirement is not a spreadsheet exercise. It is your life, your family’s security, and your ability to do the things that matter most to you for as long as you live. Inflation is the force that quietly threatens all of it.

That is why we do not build portfolios designed to avoid discomfort. We build portfolios designed to sustain purchasing power. Our cash strategy gives clients the confidence to remain invested in equities at levels that can outpace inflation, while the cash reserve provides the confidence to ride through the inevitable downturns along the way.

The true value of planning is the confidence it creates. When you understand how inflation affects your plan, when you have a strategy that accounts for it, and when you know that your cash reserve is there to keep you from selling and manage your lifestyle during the difficult stretches, you do not need to fear the market. You do not need to hide from it. You can participate in the growth potential that keeps your purchasing power intact for decades.

If you want to see what inflation is doing to your specific plan, or if you want to understand how our cash strategy could change the trajectory of your retirement, we would welcome that conversation. Reach out to us at Gatewood Wealth Solutions. We keep your priorities the priority, and purchasing power is always one of them.

Protect what your money can do, not just what it says on the statement.

Important Disclosures

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. Gatewood Wealth Solutions and LPL Financial do not provide legal or tax advice or services.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

Stock investing includes risks, including fluctuating prices and loss of principal.

Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA

CTAs are created and managed in Hubspot, the Embed Code will be used here in the HTML version of the blog.

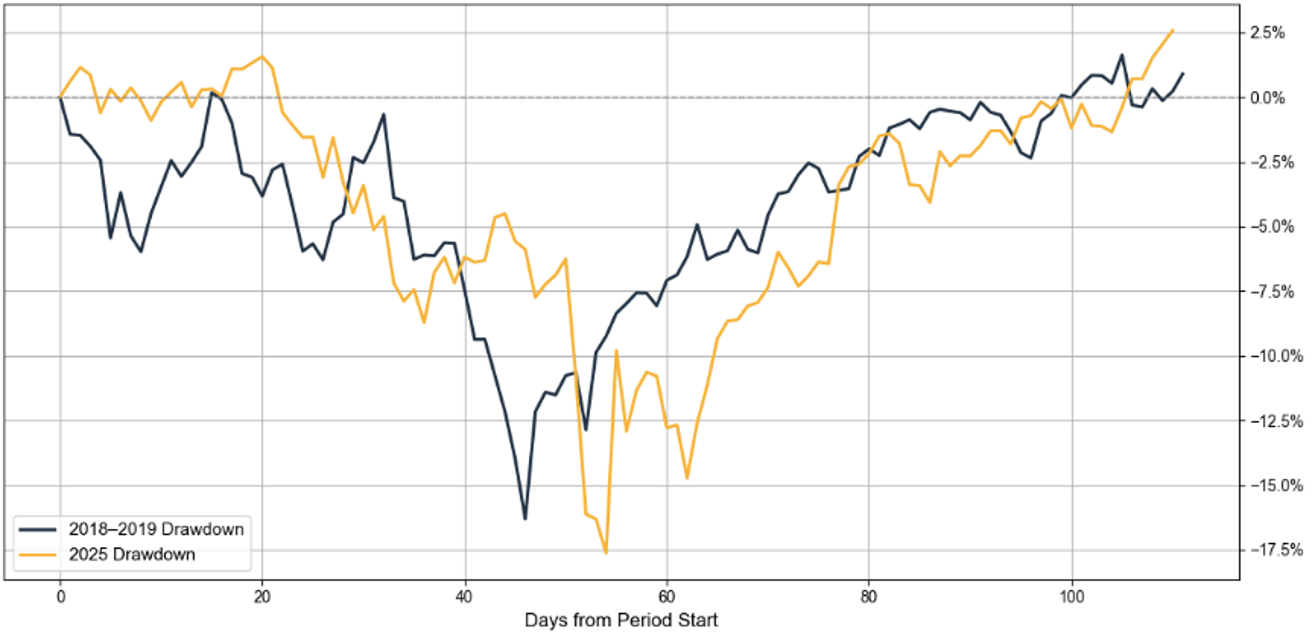

Ten months ago, the sky was falling.

Sweeping tariff announcements sent the S&P 500 plunging nearly 20% from its February 2025 peak, wiping out over $6 trillion in market value in two trading sessions. Headlines screamed recession. Pundits predicted the worst. The temptation to sell everything and hide in cash was overwhelming.

Here’s what our clients did: absolutely nothing.

Their strategy, Fortress Gatewood, held. Their fortress held. Their portfolios recovered, and then some.

Zero families served by Gatewood Wealth Solutions panic sold during the 2025 market correction. Not one.

Today, the S&P 500 is trading near all-time highs. But we’re not writing this to celebrate. We’re writing it because the next correction is coming, and the real question is whether you’ll be ready.

What Happened: The 2025 Tariff Correction

On February 19, 2025, the S&P 500 closed at an all-time high of 6,144.

Then things got ugly. Fast.

February 19 to March 13: The S&P 500 dropped over 10% on tariff fears alone, entering correction territory before “Liberation Day” even arrived.

April 2 to April 8: Sweeping tariffs on nearly all U.S. trading partners triggered the worst two-day loss in S&P 500 history. The VIX spiked to levels not seen since the COVID-19 pandemic.

April 8: The bottom. The S&P 500 sat nearly 19% below its February peak, flirting with official bear market territory.

Then, just as quickly, the reversal. A 90-day tariff pause on April 9 sent the S&P 500 surging 9.5% in a single session, one of its best days ever. By May 13, the index was positive for the year. By June 27, it hit a new all-time high.

From the April 8 bottom to today, the S&P 500 has gained roughly 40%.

The entire round trip took about four months. Investors who sold at the bottom missed all of it.

What Is Fortress Gatewood?

Fortress Gatewood is the planning framework we use to help families navigate market volatility without being forced into reactive decisions. It’s built around intentional layers (or “moats) of liquidity, income, and long-term growth, each aligned to different time horizons and real-world spending needs.

By clearly separating short-term cash needs, intermediate income sources, and long-term growth capital, the structure helps clients understand which dollars are meant to be used now, which are designed to support future income, and which are positioned for long-range objectives.

The goal isn’t to predict markets, but to create enough flexibility and clarity that market movement doesn’t dictate decisions when it matters most.

Download Your Free Copy

How the Fortress Worked

This is exactly the scenario Fortress Gatewood was designed for.

Moat Ring 1: Cash. Two years of spending in liquid reserves. No one needed to sell a single share to pay their bills. No forced selling. No panic.

Moat Ring 2: Fixed Income. Five to eight years of high-quality bonds provided less volatility with stable income. A second wall of defense while equities took the hit.

Moat Ring 3: Equities. Long-term growth capital with a 7 to 10+ year horizon. Because no one was relying on these funds for near-term needs, they could ride the storm and capture the rebound.

But here’s what made the difference: we didn’t just defend. We attacked.

On April 7, 2025, one day before the market bottomed, Chris Arends and the Gatewood Investment Committee sent guidance to every advisor on the team:

“Please contact clients with dry powder and suggest investing 1/2 to strategy now. Dry powder means funds not earmarked for short-term or mid-term spending needs. It must be long-term (>7 years).”

— Chris Arends, Gatewood Investment Committee, April 7, 2025 at 8:47 AM

That’s not a memo written in hindsight. That’s real-time guidance, issued the morning before the market hit its lowest point.

Dry powder means long-term capital not earmarked for short-term or mid-term spending. Funds with a 7+ year horizon. Because Moat Rings 1 and 2 were fully funded, we knew exactly which dollars could go to work at depressed prices, and we deployed them with conviction.

As our investment partner, Aaron Tuttle, said that same morning:

“Since 1957, we’ve had 12 corrections in the S&P 500 greater than 20%. Half were between 20-30%, three were between 30-40%, and three were greater than 40%. If you have a lot of cash, don’t overcomplicate it. Invest half now, another quarter at a 30% drop, and go all-in, buying everything you can at a greater than 40% drop. You might only get one or two opportunities at that level in your lifetime.”

Other investors were frozen. Ours were buying.

That’s the power of a fortress.

The Bigger Picture

The 2025 correction joins a pattern every investor should know by heart:

Market Event

Decline

Recovery Time

Dot-Com Crash (2000–2002)

-49.1%

7.2 Years

Global Financial Crisis (2007–2009)

-56.8%

5.5 Years

COVID-19 Crash (2020)

-34%

~6 Months

2022 Bear Market

-27.5%

~2 Years

2025 Tariff Correction

~19%

~4 Months

Every single one felt like the end of the world. Every single one recovered. Every single time, the investors who stayed disciplined won.

But Here’s What Should Keep You Up at Night

“The biggest risks are always the ones nobody sees coming. The events that aren’t on anyone’s radar are what move the world most. People are generally good at predicting the future except for the surprises that actually matter.”

— Morgan Housel, Same as Ever

The 2025 correction was the easy version. No recession. Strong consumer spending. Resilient corporate earnings. Room for the Fed to cut rates. The economy absorbed the shock and bounced back in months. V-shaped recovery!

That won’t always be the case.

When we study the last 50 years of S&P 500 bear markets, the data is clear: the presence or absence of a recession changes everything.

Bear Markets Without a Recession (1987, 2022)

Metric

Average

Decline

-30%

Peak to Trough

~6.5 months

Full Round Trip

~23.5 months (~2 years)

Bear Markets With a Recession (1980–82, Dot-Com, GFC, COVID)

Metric

Average

Decline

-42%

Peak to Trough

~17.5 months

Full Round Trip

~46 months (~3.8 years)

Recessionary bears are 12 percentage points deeper. The decline phase is 3x longer. The total round trip takes twice as long.

And if you exclude the anomalous COVID recovery (compressed by unprecedented government intervention), the three traditional recessionary bears averaged about 5 years from peak to recovery.

Since 1975, four out of six bear markets have coincided with recessions. We are statistically due for another one. The question isn’t if. It’s when.

Are you building your fortress now, while the sun is shining? Or will you try to build it in the middle of the storm?

The Danger of All-Time Highs: Complacency

Here’s the part most people don’t want to hear: all-time highs are when fortresses get built, not when they get tested.

Right now, with markets at record levels and three straight years of strong returns behind us, it’s tempting to relax. To assume the good times will continue indefinitely. To skip the disciplined work of maintaining cash reserves and rebalancing into fixed income.

But the 2025 correction is a reminder that the next downturn doesn’t send a calendar invite. It shows up unannounced, sometimes triggered by a single speech in a Rose Garden.

With the S&P 500 near 7,000 and all-time highs stacking up, most investors are relaxed. We’re not.

We’re using this moment of strength to prepare for the next moment of weakness:

Reviewing cash positions to make sure every client has their full 2-year liquidity buffer

Rebalancing into fixed income to lock in yields and maintain the 5 to 8 year spending bridge

Harvesting equity gains to fund and strengthen the outer moat rings

Stress-testing every plan against recessionary scenarios: 40%+ drawdowns, multi-year recoveries, rising unemployment

We’re not predicting a crash. We never do. We’re preparing for one, because that’s what we always do.

The Firm to Family™ Advantage: Why the Fortress Held

Zero panic selling across our entire client base is not an accident. It’s the result of how Gatewood is built.

At most firms, the investment team doesn’t talk to the financial planner. The financial planner doesn’t talk to the tax advisor. And nobody coordinates the message to the client when markets are in freefall.

At Gatewood, our Firm to Family™ structure means every professional who touches your financial life is working from the same plan, communicating continuously, and aligned on the same strategy.

When markets dropped in April, your wealth planner could tell you with precision how many months of expenses were covered without touching a single equity position. The Investment Committee was providing real-time guidance on deploying dry powder. And the planning team was tracking the tax implications of every move to make sure nothing was done without considering the full picture.

Our clients didn’t panic because they didn’t have to. They had a plan, a team, and a fortress. And they heard from their advisor, personally, before the bottom even arrived.

The 2025 correction proved the Fortress Gatewood system works. Our clients didn’t panic. They didn’t sell. They didn’t miss the recovery. Zero families. Zero panic sales. Many of them used the downturn to buy at depressed prices and came out stronger on the other side.

But the next test might not be a four-month correction. It could be a recessionary bear market that grinds on for years. The families who navigate that with confidence will be the ones who built their fortress today, while markets were strong and emotions were calm.

Don’t wait for the storm to start digging the moat.

Important Disclosures

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. Gatewood Wealth Solutions and LPL Financial do not provide legal or tax advice or services.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Appendix: Sources

S&P 500 Historical Data & 2025 Market Correction

S&P Dow Jones Indices. S&P 500 historical closing prices.

“2025 Stock Market Crash.”

NBC News. “S&P 500 Hits an All-Time High—Rebounding to Its Level When Trump’s Second Term Began.” June 27, 2025.

CBS News. “The Stock Market Is Nearing a Record High After Cratering in April. Here’s Why.” June 27, 2025.

“How the Stock Market Made Back All Its Losses After Trump Escalated the Trade War.” May 4, 2025.

CNN Business. “What to Expect From Stocks in 2026.” January 1, 2026.

S. Bank. “Stock Market Under the Trump Administration.” Updated February 4, 2026.

Trading Economics. “United States Stock Market Index.” February 10, 2026.

Bank for International Settlements. “Understanding the Swift Market Recovery After the April 2025 Tariff Shock.”BIS Quarterly Review, September 2025.

April 2025 Tariff Crash Details

CNN Business. “Dow Plunges 2,200 Points as Tariff Tumult Rocks Markets.” April 4, 2025.

“Tariff Shock: Top S&P 500 Winners and Losers (April 2–16, 2025).”

Bear Market Historical Data & Recession Analysis

S&P 500 bear market peak-to-trough and recovery data, 1975–2025.

S&P 500 historical performance and earnings data.

National Bureau of Economic Research (NBER). S. business cycle expansions and contractions.

“A History of Bear Markets.”

“A History of Stock Market Percentage Declines (15% to 50%).”

“Here’s How Often Stocks Dip 5% or More.”

Austin Wealth Management. “Dealing With the Dips.”

2026 Market Outlook & Valuation

The Motley Fool. “With the S&P 500 at an All-Time High to Start 2026, Is It Smart to Buy Stocks?” January 9, 2026.

The Motley Fool. “History Says a Turning Point Is Likely Coming for the S&P 500 in 2026.” January 1, 2026.

Visual Capitalist. “152 Years of S&P 500 Returns (and Predictions for 2026).” January 2026.

Advisor Perspectives. “S&P 500 Snapshot: Index Closes at Record High.” January 2, 2026.

Books Cited

Housel, Morgan. Same as Ever: A Guide to What Never Changes. Portfolio/Penguin, 2023.

Understanding the New Children’s Investment Accounts Launching in 2026

Every parent dreams of giving their children a head start in life. Starting in 2026, a new federal program will do exactly that—and thanks to an extraordinary $6.25 billion pledge from Michael and Susan Dell, the gift just got bigger.

Here’s what makes this program remarkable: If you have children age 10 or under, they may automatically receive up to $1,250 in free investment capital—$1,000 from the government plus $250 from the Dell Foundation. No action required beyond enrollment. For a family with two eligible children, that’s $2,500 invested in their future at no cost to you.

The question isn’t whether to accept this gift—it’s whether these “Trump Accounts” make sense as part of your broader savings strategy for your children.

What These Accounts Are Called

These accounts are commonly known as “Trump Accounts” or “Children’s Investment Accounts.” They’re formally defined in Section 530A of the One Big Beautiful Bill Act and are sometimes referenced as “530A accounts” in tax documentation.

Official Website: All program and enrollment information will be published at trumpaccounts.gov

Program Timeline

Spring 2026: Families can begin enrolling by filing IRS Form 4547 with their tax returns or through other designated methods.

Mid-2026: Online enrollment portal launches at trumpaccounts.gov.

July 4, 2026: The program formally launches with seed deposits funded, contributions enabled, and full account access available.

How Trump Accounts Work – The Basics

Eligibility

Any U.S. citizen under age 18 with a Social Security number can have an account opened on their behalf. Children born between 2025 and 2028 automatically receive a $1,000 government-funded seed deposit.

The Dell Foundation Gift

The Dell family’s $6.25 billion contribution provides an additional $250 to eligible children who meet specific criteria: age 10 and under, born before January 1, 2025, and living in ZIP codes with median household incomes of $150,000 or less. This enhancement reaches approximately 25 million children across roughly 75% of U.S. ZIP codes.

Annual Contributions

Families may contribute up to $5,000 per year per child, including employer contributions. Employers may contribute up to $2,500, which counts toward the $5,000 annual cap. Philanthropic enhancements like the Dell gift are separate and don’t count against contribution limits.

Investment Requirements

All funds must be invested in low-cost, broad U.S. equity index funds designated by the Treasury Department. Annual fees are capped at 0.1%. Accounts are initially established through the Treasury and can later be transferred to approved private financial institutions.

The Critical Detail: What Happens to the Tax Treatment

Understanding the tax treatment matters because it affects whether you should add your own money to these accounts or use other vehicles instead. Think of it in two phases:

PHASE 1: Before Age 18 (The Accumulation Phase)

During childhood, contributions are made with after-tax dollars, and investment growth accumulates tax-deferred. Parents or guardians maintain control of the account during this period. This phase is straightforward.

PHASE 2: After Age 18 (The IRA Conversion Phase)

At age 18, Trump Accounts automatically convert to traditional IRAs. This conversion fundamentally changes how the account functions:

Access and Control: The young adult gains full control as the account becomes a traditional IRA in their name.

Withdrawals and Taxes: This is where it gets important. Distributions are taxed as ordinary income on all earnings and growth (though your original contributions come back tax-free). Additionally, the 10% early withdrawal penalty applies to distributions before age 59½.

The Exception Rules:

The 10% penalty (not the taxes) can be waived for:

First-time home purchases (up to $10,000)

Qualified education expenses

Business startup costs in certain circumstances

Here’s the crucial point many families miss: These “qualified expenses” only waive the 10% penalty—they do NOT eliminate the ordinary income tax on the earnings. Even when funding college or buying a first home, you’ll owe income tax on all the growth.

Investment Flexibility: After conversion, the account can be invested more broadly according to traditional IRA rules, no longer restricted to designated index funds.

Why This Matters: This automatic conversion to a traditional IRA means families should carefully consider whether contributing their own funds makes sense compared to other savings vehicles like 529 plans (where qualified education withdrawals are completely tax-free) or custodial accounts (where flexibility is greater).

Comparing Your Options: Trump Accounts vs. 529 Plans vs. UTMA Accounts

We believe informed decisions come from clear comparisons. Here’s how Trump Accounts stack up against the savings vehicles you may already be using:

Trump Accounts offer a $1,000 government seed deposit (for children born between 2025 and 2028) plus potential philanthropic enhancements like the Dell gift. The $5,000 annual contribution limit includes employer contributions. Investment growth is tax-deferred, and the account converts to a traditional IRA at age 18. Withdrawals after 18 are taxed as ordinary income with standard IRA penalties and exceptions applying. The parent controls the account until age 18, then the child gains full access.

529 Plans have no government seed funding but offer no annual contribution limits (though lifetime caps apply by state). Contributions may be deductible at the state level. Investment growth is completely tax-free when used for qualified education expenses. Withdrawals for education are entirely tax-free, while non-education withdrawals face taxes and penalties. The account owner retains control indefinitely and can change beneficiaries.

UTMA Accounts offer no government funding and no annual limits beyond gift tax considerations. There are no tax deductions for contributions. Investment growth is taxable annually, and the kiddie tax may apply. Withdrawals can be used for any purpose benefiting the child with no special tax treatment or penalties. The child gains full, unrestricted control at age 18 to 21 (depending on state), and investment options are highly flexible.

The Bottom Line: The right choice depends entirely on your family’s priorities and timeline—which is exactly the kind of conversation we help clients navigate.

Our Perspective: When Trump Accounts Make Sense

At Gatewood, we believe in giving you straight talk about financial products—even new, politically branded ones. Here’s our professional perspective:

The free money is a no-brainer. If your child qualifies for the government seed and Dell enhancement, opening an account is essentially accepting a gift. We’d help every eligible family capture this benefit.

Your own contributions require more thought. For most families focused on education funding, 529 plans deliver better tax outcomes. The Trump Account’s conversion to an IRA at 18 means you’ll pay ordinary income tax on withdrawals—even for education. That’s objectively less attractive than a 529’s completely tax-free treatment for qualified education expenses.

But there are scenarios where these accounts shine:

You’re already maxing out 529 contributions and want additional tax-advantaged savings

Your priority is very long-term wealth building (retirement savings starting at birth)

You’re specifically targeting a first home down payment for your child

You want to diversify across multiple savings vehicles with different tax treatments

Remember that implementation details are still evolving. The IRS continues to issue guidance on program specifics, and some questions remain unanswered as of December 2025.

The key question isn’t “Are Trump Accounts good or bad?” It’s “Are they right for YOUR family’s specific goals and timeline?”

The Bigger Picture: Why This Program Was Created

This program reflects a simple idea: giving young Americans an ownership stake in the economy early can transform how they think about money, investing, and wealth-building. The policy goals include expanding equity ownership across economic classes, supplementing Social Security with private savings, and creating what policymakers call a “shareholder economy.”

Whether this achieves its lofty policy goals remains to be seen—but for individual families, the opportunity to capture free seed capital and teach children about investing is very real and tangible.

Treasury officials emphasize these accounts are designed to supplement, not replace, Social Security and other safety net programs. The long-term vision is to empower a generation with real assets, investment experience, and an ownership mindset from day one.

How Gatewood Can Help

This program launches in mid-2026, which gives us time to think strategically together. Our process focuses on three essential questions:

Does your family qualify for the maximum benefits, including the Dell enhancement?

Should you contribute your own funds, or does a 529 or custodial account better serve your goals?

How does this fit into your broader wealth-building strategy for your children’s future?

We excel at these nuanced conversations—the kind where “it depends” actually becomes “here’s exactly what makes sense for you.” This isn’t about selling you on Trump Accounts. It’s about ensuring you make the most informed choice for your family’s unique situation.

Ready to discuss your family’s strategy?

Important Considerations

This program is new, and IRS regulations continue to evolve. The information provided here reflects program details as understood in December 2025, but specific rules and procedures may change as implementation progresses. Investment returns are not guaranteed, and tax laws may change. This material is educational and not a recommendation for any specific action.

For personalized guidance on whether Trump Accounts make sense for your family, we encourage you to consult with a financial advisor and tax professional who can evaluate your complete financial picture.

Important Disclosures

Securities and advisory services are offered through LPL Financial, a registered investment advisor and broker-dealer (member FINRA/SIPC).

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Gatewood and LPL Financial are separate entities. Gatewood Wealth Solutions does not provide legal or tax advice directly. However, Gatewood Tax & Accounting, a separate entity under the Gatewood family of companies, provides comprehensive tax planning and preparation services. For legal matters, you should consult your legal advisor regarding your personal situation. Our team coordinates closely with clients’ tax and legal professionals to help ensure comprehensive planning.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax.

This information is not intended to be a substitute for individualized tax advice. We suggest that you discuss your specific tax situation with a qualified tax advisor.

Prior to investing in a 529 Plan investors should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

Why solving our fiscal problems requires more than populist revenue

Dan’s recent blog on tariffs sparked great debate—and it’s exactly the kind of back-and-forth that makes Gatewood special. We don’t always agree, but we’re united by a deeper goal: helping clients—and the country—move forward with clarity.

In fact, Dan and I agree on much more than we disagree. We both want fiscal sanity. We both want a more secure, more sovereign America. But where I start to diverge is in how we get there—and more importantly, what costs we may be ignoring along the way.

The Patriotic Appeal

Tariffs have an undeniable surface-level appeal. They feel like we’re standing up for ourselves. They’re visible, easily framed as constitutional, and unlike the income tax, they don’t require the IRS knowing the color of your wallpaper.

For those of us who believe in limited government, sound money, and national sovereignty, tariffs can feel like a clean swap: ditch the bloated tax code, bring back duties on imports, and reignite American industry.

But that’s the illusion. We’re not replacing anything—we’re adding.

If Tariffs Fix It… Why More Debt?

Let’s be honest about the timing. If tariffs were the fix, why did the same legislative push include a $5 trillion hike to the debt ceiling?

Yes, our tax system is bloated and full of misaligned incentives. But changing the source of tax revenue without reducing the need for tax revenue just feeds the same appetite with a different spoon.

Dan—and even the Trump administration, at times—have argued that no one is offering serious spending cuts. But that’s not quite accurate. DOGE is actually an example of a proposed constraint with substantial support, at least among the public.[1]

Likewise, leaders like David Stockman, Rand Paul, and Thomas Massie have consistently proposed concrete spending reductions.[2] Think tanks like the Heritage Foundation have published full spending-cut blueprints—for example, their “Blueprint for Balance” report offers detailed proposals across discretionary and mandatory spending categories.[3] The problem isn’t a lack of ideas—it’s a lack of political will. And when the addiction runs this deep, adding more revenue doesn’t promote sobriety—it just buys more drinks.

As an aside, entitlement reform is where the real fiscal reckoning lies. These off-balance sheet liabilities are rapidly becoming on-balance. Means testing, extending age eligibility, and protecting those already relying on Social Security is likely the responsible, principled path forward. But that requires honesty—and the courage to call these programs what they legally are: welfare benefits.[4]

Tariffs Are Taxes—Let’s Not Pretend Otherwise

We can debate whether tariffs are inflationary (and I tend to agree with Dan: they’re not in the strict monetary sense). But they are a tax. Like all taxes, they distort prices, create inefficiencies, and protect the politically connected.

Tariffs rarely stop at revenue. They become vehicles for cronyism. Industries seek shelter, not strength. Consumers pay more, often unknowingly. The economy shifts—not through innovation, but through manipulation.

We may “win” a few trade skirmishes, and no, this isn’t Smoot-Hawley 2.0. But if our goal is genuine economic progress, tariffs risk lowering our standard of living—especially if they mask the real disease: runaway spending.

What Actually Works

Here’s what history supports:

Lower and flatter tax codes

Capital formation and voluntary exchange

A federal government limited to its essential roles

We’ve seen it repeatedly: prosperity isn’t determined by how you collect revenue, but by how much is taken and how little the market is distorted in the process.

History shows that income taxes, even with rate changes, tend to remain a steady share of GDP—an observation often attributed to Hauser’s Law, which suggests that federal tax revenues rarely exceed 19–20% of GDP regardless of marginal tax rates. This pattern is also supported by Congressional Budget Office (CBO) data over the past several decades.[5] What shifts is who shoulders the burden. And corporate taxes—despite political rhetoric—have declined significantly as a share of overall federal revenue, falling from over 10% in the late 1980s to under 7% in recent years.[6] It’s no wonder Washington is eager to find new tools.

The Real Discipline Test

In theory, tariffs could be a more visible and arguably more constitutional source of revenue—if they were replacing something.

But they’re not. And they won’t. Not without structural reform. Not without Congress giving up its favorite excuse: “We just need more revenue.”

Dan and I agree: America needs to get its fiscal house in order.

But the discipline we need won’t come from patriotic branding or populist packaging.

It will come from restraint. From honesty. And from the courage to say no—not just to foreign imports, but to our own worst habits.

Want to talk about how policy changes might affect your financial plan? Reach out—we’d love to help you navigate it.

Want to hear the other side?

Gatewood’s COO, Dan Goeddel makes the case for tariffs as a practical, if imperfect, fiscal tool. [Explore Dan’s View →]

Family Footnote

Fun fact: I had a family member involved in the Boston Tea Party. Contrary to popular belief, it wasn’t about high taxes. It was about removing a tax that gave British tea a price advantage over American-smuggled tea. The rebellion wasn’t over taxation alone—it was over losing an advantage because of taxation. And some things never change.

[2] Rand Paul’s “Festivus” Reports, David Stockman’s works like “The Triumph of Politics,” and Thomas Massie’s repeated bills and votes targeting discretionary spending.

[4] I sympathize with those who say, “I paid into the system.” Many were led to believe Social Security was a personal savings or insurance program. But as the Supreme Court confirmed in Flemming v. Nestor (1960), Social Security is a general welfare benefit—not a contractual right. That doesn’t mean we shouldn’t protect those counting on it, but it does mean we need to be honest about the structure going forward.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

This information is not intended to be a substitute for individualized tax advice. We suggest that you discuss your specific tax situation with a qualified tax advisor.

There’s a glaring contradiction in today’s economic discourse, and it clouds the investment outlook. The loudest voices warning about America’s unsustainable federal deficit are often the most reflexive critics of tariffs, an essential tool that could help address the crisis. They demand “fiscal responsibility” but fall silent when asked what they’d cut from the budget. Suggest entitlement reform, and they’ll tell you it’s political suicide. Propose higher income taxes, and they bristle at the economic drag. Ask how they’d raise $2.0 to $2.8 trillion annually to close the federal budget gap, and the conversation ends.

That’s why tariffs—unfashionable, imperfect, and deeply misunderstood—may be one of the only practical tools left that can meaningfully address the deficit until the country is ready for major changes to how the government collects revenue and spends.

D.O.G.E. Promised a Trillion-Dollar Fix. It Delivered a Rounding Error.

The Department of Government Efficiency (D.O.G.E.) was supposed to be the bold solution to government waste. Originally pitched as a vehicle for cutting $1 trillion in inefficiencies, the agency—backed by Elon Musk and restructured under President Trump—quickly revised expectations downward to $150 billion. D.O.G.E. operates as a consultant would, examining costs and structure and recommending changes to achieve efficiencies across various departments.

D.O.G.E. impact is a subject of some debate. As of mid-2025, D.O.G.E. has claimed between $150 billion and $ 90 billion in savings, although independent audits dispute much of that figure. More troubling, aggressive cuts to revenue-generating agencies like the IRS reduced government income. By some estimates, DOGE’s efforts may have cost taxpayers $135 billion through re-hires, overtime, legal settlements, and lost tax collections.

While well-intentioned and fundamentally a good idea, the shortfall was a strategic failure that exposed the limits of the “cut spending” approach. D.O.G.E. aimed to trim fat but ended up delivering a rounding error instead of transformational change.

Growth Alone Won’t Save Us

With a less-than-spectacular D.O.G.E. impact, and large Government spending cuts off the table — at least for now — the bipartisan default in Washington has long been to grow the economy and let increased tax receipts shrink the deficit as a percentage of GDP over time. It’s an appealing theory that consistently fails in practice. Despite periods of strong GDP growth, federal spending continues to outpace revenue by unprecedented margins.

While the growth strategy is politically palatable and will help over time, the U.S.’s current fiscal situation, with annual deficits of over $2 trillion, is dire. We don’t have the luxury of waiting for growth to solve a crisis that compounds daily. Growth matters, but it’s not enough. We need substantial revenue, and we need it soon.

Understanding Tariffs: A Tax, Not Inflation

Let’s address the elephant in the room: tariffs are, in fact, a tax. But they are emphatically not inflation.

Inflation is a monetary phenomenon—the expansion of the money supply that dilutes currency value and drives broad-based price increases. Tariffs don’t expand the money supply or devalue the dollar. They are a targeted consumption tax applied to imported goods, with three key differences from domestic taxes:

Revenue generation: Unlike inflation, tariffs generate federal government revenue, potentially $300 billion annually

Targeted impact: They affect specific imported goods rather than the entire economy. Imports are roughly 15% of the U.S.’s GDP today.

Importer and Corporate absorption possibility: Who absorbs the cost increase from U.S. tariffs is an interesting and complex question, with the absorbing party differing by item and by importer. With energy costs roughly 10% lower than two years ago, many corporations have absorbed most of the tariff costs rather than passing them through

Despite persistent warnings from economists, tariffs have not triggered the runaway inflation they predicted.

The Hidden Costs of Corporate Absorption

However, when corporations absorb tariff costs, the economic impact doesn’t simply disappear—it gets redistributed. Companies facing compressed profit margins from tariff absorption experience a cascade of effects that ultimately flow back to the broader economy:

Reduced profit margins lead to lower corporate earnings, which translate to decreased stock valuations. This creates a diminished wealth effect as portfolio values decline, prompting consumers to reduce spending. Meanwhile, lower capital gains tax revenue partially offsets the government’s gains in tariff income.

This redistribution means that while tariffs may not be directly reflected in consumer prices, their costs still flow through the economy via financial markets and reduced economic activity.

The Regressive Reality of “Targeted” Impact

While tariffs don’t affect every sector equally, describing their impact as merely “targeted” obscures an important truth: if passed through, they disproportionately burden lower-income households. These families spend a higher percentage of their income on goods (versus services), have less flexibility to substitute away from imported products, and are more price-sensitive to increases in everyday items.