Most 529 plans take a conservative approach to risk. What if being too cautious early on means leaving thousands of dollars on the table?

At Gatewood Wealth Solutions, we believe the key to smarter college savings is compounding earlier—when you have the time—and only dialing back risk when it truly matters. In this post, we walk through our custom 529 glide path and compare it to the most common industry average.

Why Glide Paths Matter in 529 Plans

Glide paths are automated investment changes. In 529s, most glide paths reduce equity (stocks) and increase fixed income (bonds/cash) as the beneficiary enters elementary school. It sounds sensible, but the problem is: these providers reduce risk far too early.

Most Gatewood clients don’t touch 529 money until the first year of college. Even then, withdrawals happen over four years. Many families don’t fully spend the accounts at all—preserving them for legacy planning. If the money is invested too conservatively for too long, it underperforms significantly.

That’s where the Gatewood Glide stands apart.

Our Glide Path

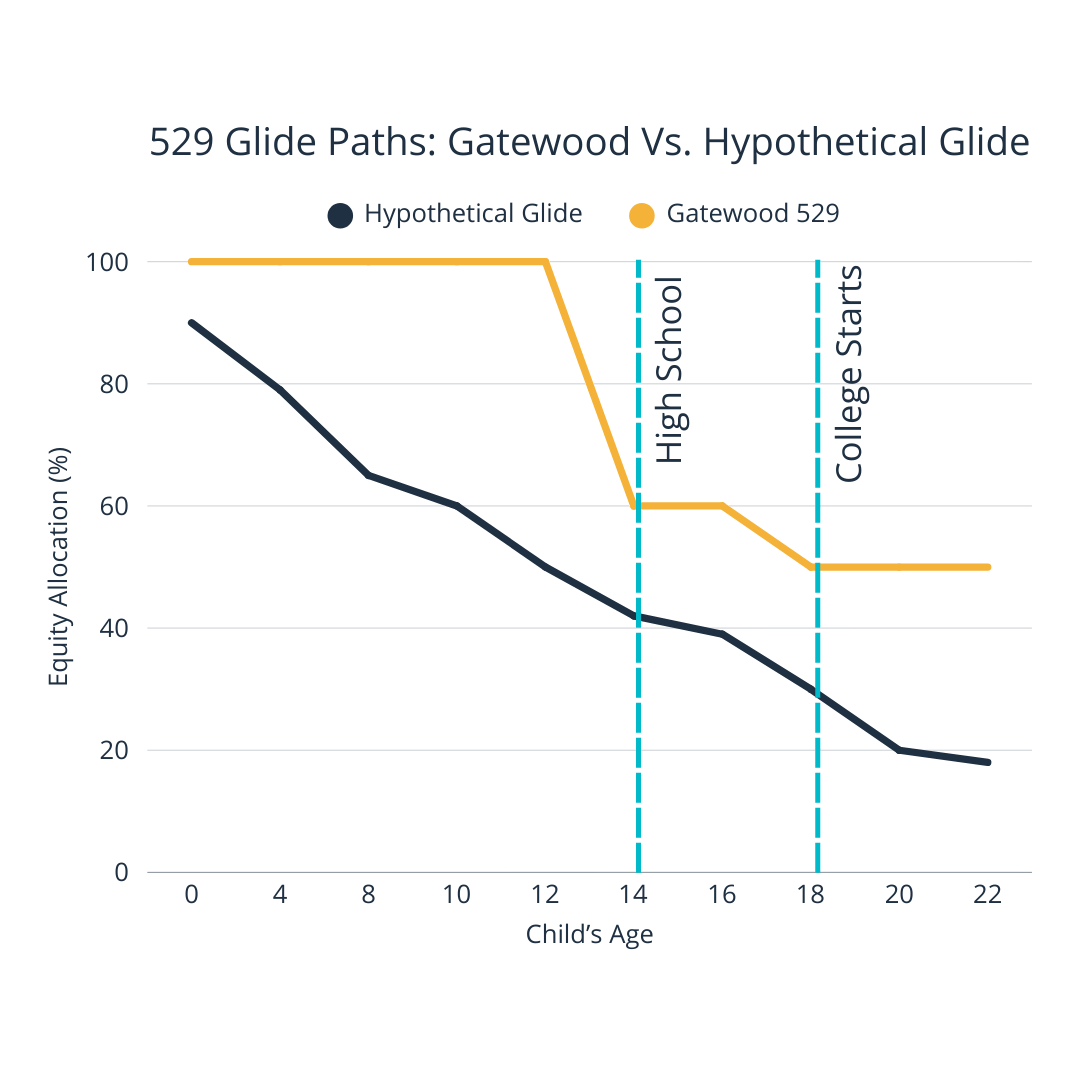

Gatewood’s 529 Glide:

- Starts at 100% equity

- Moves to 60% equity/40% bonds at high school entry (~age 14)

- Drops to 30% equity / 40% bonds / 30% cash at college entry (~age 18)

This gives investors the opportunity to benefit from long-term market growth while still adjusting tactically later if needed.

Glide Path Comparison: Equity Allocation by Milestone

| Plan | Starting Equity | Equity at HS Entry | Equity at College Entry | Avg Equity Allocation |

| Gatewood 529 | 100% | 60% | 30% | 85% |

| Hypothetical Glide 529 | 95% | 30% | 15% | 56% |

Equity Glide Paths

Why It Matters

We are a regulated industry, so publishing expected equity returns can be difficult. However, investors are aware of a consistent equity premium earned in the long run from taking equity risk over fixed income and cash.

Eighteen years is a long-term horizon. We believe that maintaining an average allocation above 80% equity during the growth years aims to lead to better results compared to the typical glide, which tends to average below 60% equity.

Finally, 529 plans are more than just tax shelters. They’re strategic long-term tools. By defaulting too conservative, traditional glide paths underserve many families. At Gatewood, we believe in giving your savings room to grow, with thoughtful transitions when the time is right.

Our 529 strategy reflects how clients really use their plans:

- Continued contributions during high school

- Maintain flexibility around college withdrawals

- Preserve asset for legacy planning

If you’re interested in building a 529 plan that aligns with your goals, we’re here to help.

Building a Better 529 Plan Strategy

Also read: Rethinking the 529: A Legacy Vehicle Hiding in Plain Sight

Explore how 529 plans can extend beyond college savings and support multi-generational wealth planning.

Important Disclosures

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing.

Prior to investing in a 529 Plan investors should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.